Auto Partner: Steering Around a Challenging Environment

Auto Partner (APR.WA) Full Year 2023 Earnings Analysis

Executive Summary

There is a growing need for maintenance and repair services in both Poland and the European Union due to the increasing average age of passenger cars. Despite modest GDP growth and fluctuations in new car registrations, steady demand for used cars, particularly older models, indicates a consistent need for vehicle maintenance and repair services.

Auto Partner's strong revenue growth in 2023 was fuelled by a combination of strategic initiatives, market diversification, and effective pricing strategies, positioning the company for continued success in the automotive aftermarket industry. Auto Partner faced margin pressure in 2023, with both gross and operating margins declining compared to 2022. The gross margin decrease was primarily due to currency exchange headwinds affecting product pricing dynamics. Additionally, the operating margin decrease was attributed to factors such as inflated transport costs, inflationary pressures, and higher finance costs due to interest rate hikes.

Auto Partner’s business model has led to a Return on Capital of 13% in 2023. This notable performance is primarily attributed to the effective utilization of its branch network. Despite only a modest 2% increase in the number of branches, the company managed to achieve a significant 27% growth in average revenue per branch. Management's strategic approach of focusing on optimising existing branches rather than rapid expansion reflects a less capital-intensive strategy akin to the Home Depot model, aiming for sustained growth and operational efficiency.

Auto Partner’s margins are likely to face continued pressure in 2024 due to several factors: falling inflation, which will not translate into higher sales prices; impending wage increases due to new minimum wage laws in Poland; and the likelihood of existing conditions persisting, rather than a reversal of currency exchange rates to historical levels.

Contents

Financial Highlights

Business Activity

Financial Analysis

Guidance

Conclusion

1. Key Highlights

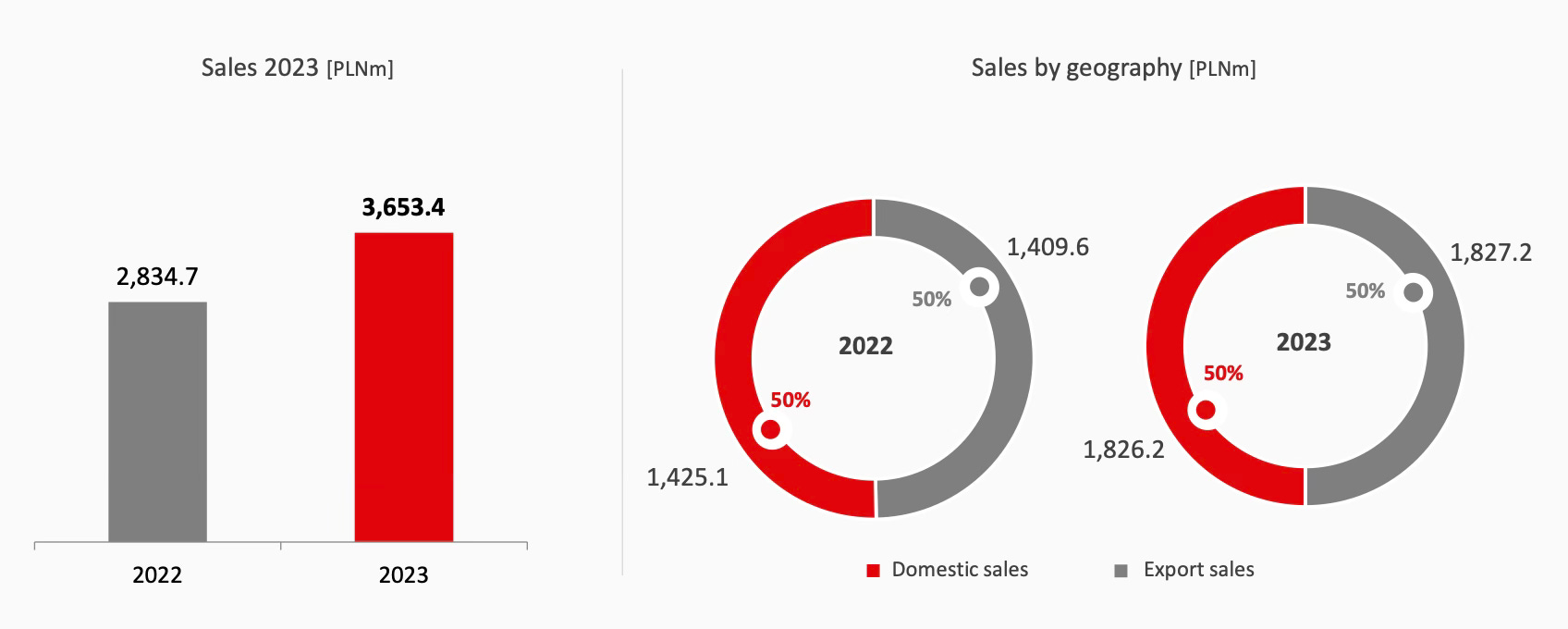

Revenue: PLN 3,653.4 million +29% year-over-year (YoY)

Gross Profit: PLN 989.9 million +17% YoY

Operating Profit: PLN 302.7 million +8% YoY

Net Profit: PLN 223.6 million +8% YoY

2. Business Activity

Customer Base

Auto Partner’s (APR) market share of the auto parts market in Poland remains unchanged at 10%. International markets remain increasingly important for the company and account for 50% of sales. About 70% of APR’s orders are placed online, but when it comes to international markets, 99% of orders are placed online.

When it comes to the domestic market in Poland, repair workshops account for almost two-thirds of all revenue. Specialized stores now account for 30% of revenue, up from 27% in Q3.

APR’s own brand, MaXgear, offers over 35,000 individual parts and contributes 20% to total sales.

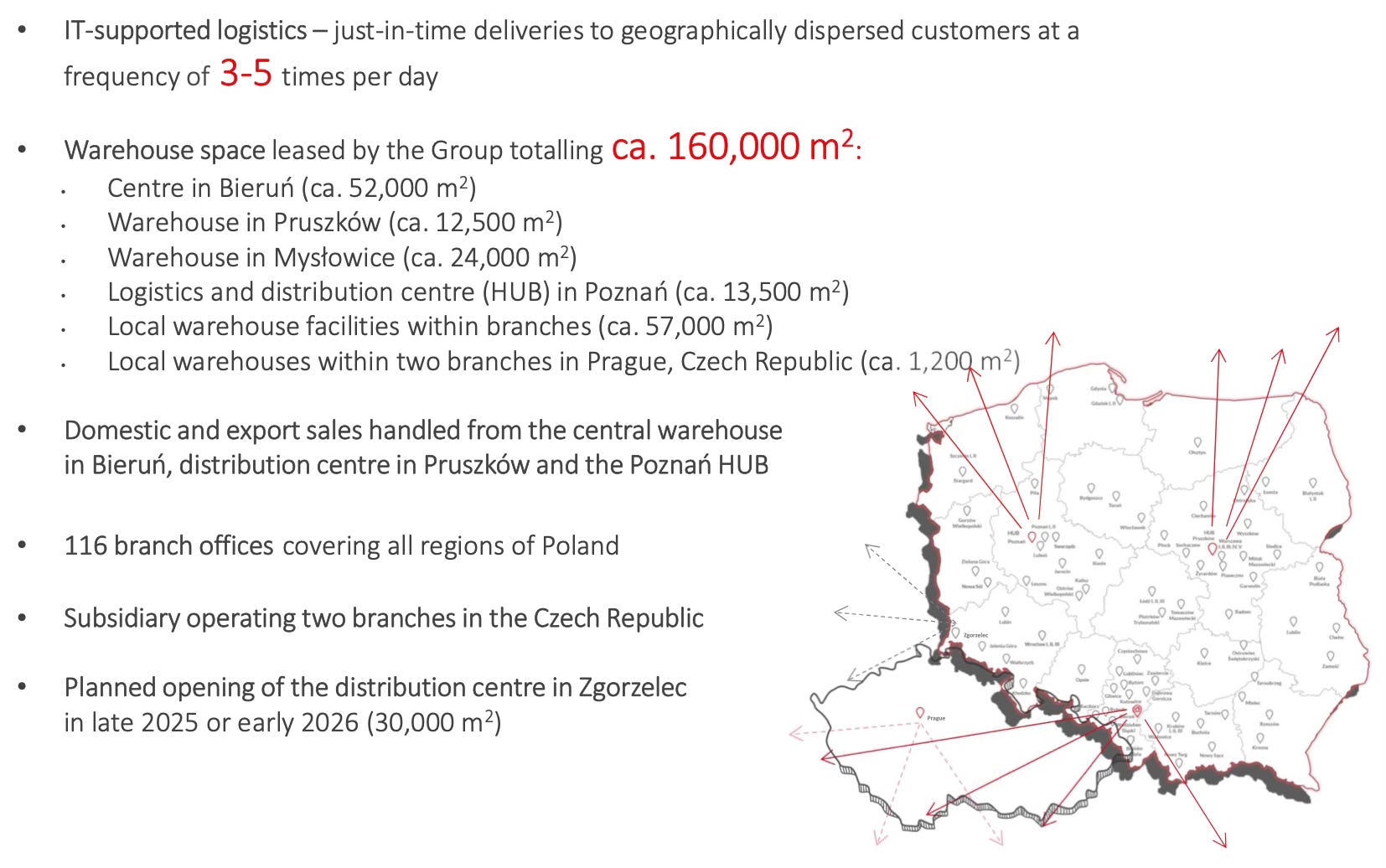

Logistics Network

APR's main distribution center is in Bierun, along with two hubs in Pruszkow and Poznan. Another hub is being built in Zgorzelec and will open in 2025. This is a strategic move as it is located near the western border of Poland. This is significant because it will bring APR a few hours closer to international markets. APR will be able to reach further distances, and customers will be able to place orders for longer periods, allowing APR to be even more competitive in international markets.

Market Environment

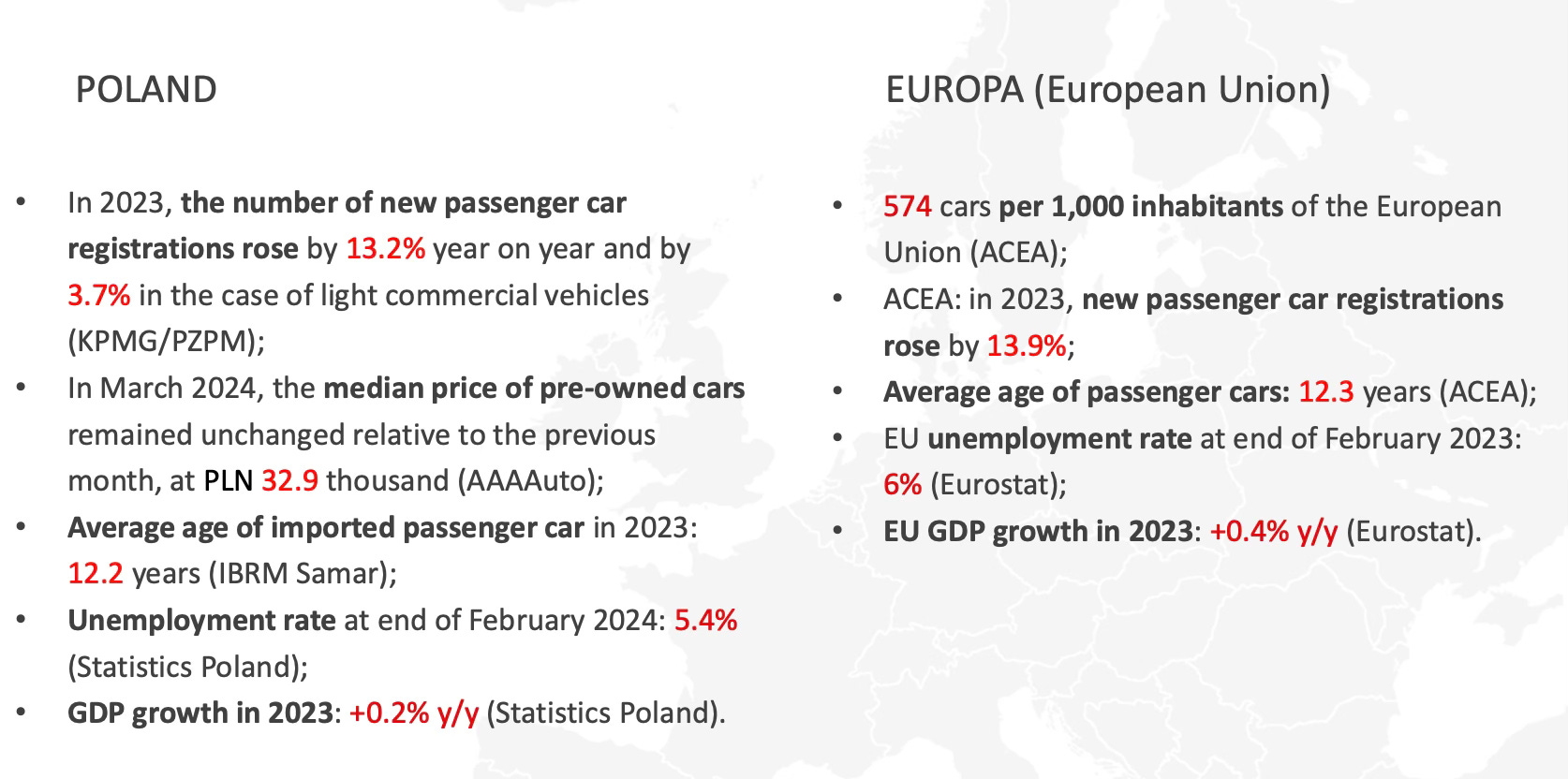

With the average age of imported passenger cars in Poland reaching 12.2 years and the average age of passenger cars in the European Union at 12.3 years, there is a growing need for maintenance and repair services. Older vehicles typically require more frequent servicing and repairs to remain roadworthy.

Despite the increase in the number of new passenger car registrations, the median price of pre-owned cars in Poland remained unchanged. This suggests that there is a steady demand for used cars, particularly older models, which will continue to contribute to the need for maintenance and repair services

With relatively low unemployment rates in both Poland (5.4%) and the European Union (6%), consumers are more likely to have disposable income to spend on vehicle maintenance. APR can target these employed individuals who rely on their vehicles for daily transportation and are willing to invest in keeping their cars in good condition for longer periods.

Despite modest GDP growth in both Poland (+0.2% y/y) and the European Union (+0.4% y/y), the automotive industry remains resilient, indicating sustained consumer spending on vehicles and related services.

3. Financial Analysis

Revenue

APR grew revenue by 29% in 2023 to PLN 3.65 billion. Management attributes this growth to a couple of key drivers:

Expansion into new export destinations and routes.

Opening of new branches in Poland.

Further expansion of the product mix and better alignment with customer needs across different price segments.

Price increases due to rising costs of automotive parts, as well as fluctuations in the EUR/PLN and USD/PLN exchange rates.

During the conference call, management disclosed that at least 20% of the revenue growth was driven by volume, with the remainder attributed to inflation.

Export sales to international markets contribute half of the total revenue, with a 30% growth in 2023. Domestic sales also grew by 28% during the same period.

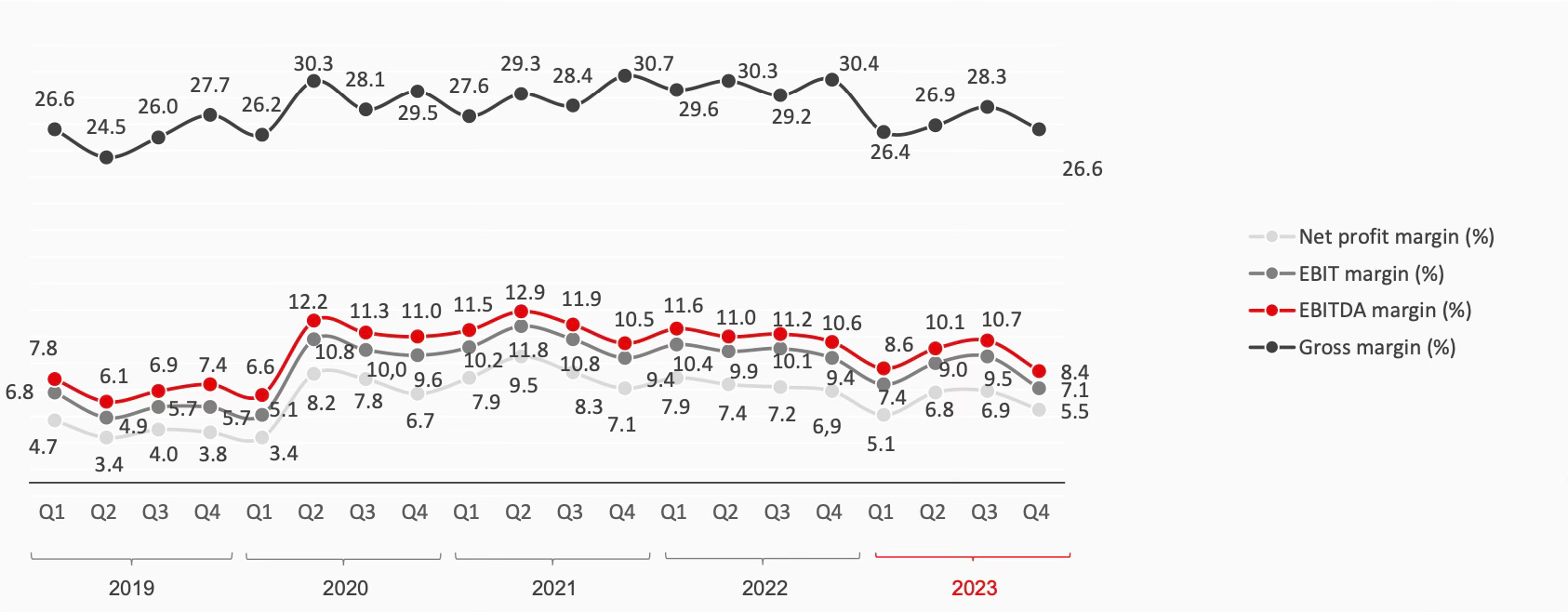

Gross Margin

APR achieved a gross margin of 27.1% in 2023, which deteriorated from 29.9% in 2022. On the conference call, management noted that the drop in 2023 was a result of currency exchange headwinds, which led to more expensive products being bought in 2022 during a period of PLN depreciation and then having to be sold at a lower price in 2023. This was followed by a strengthening trend continuing until the end of 2023.

Operating Margin

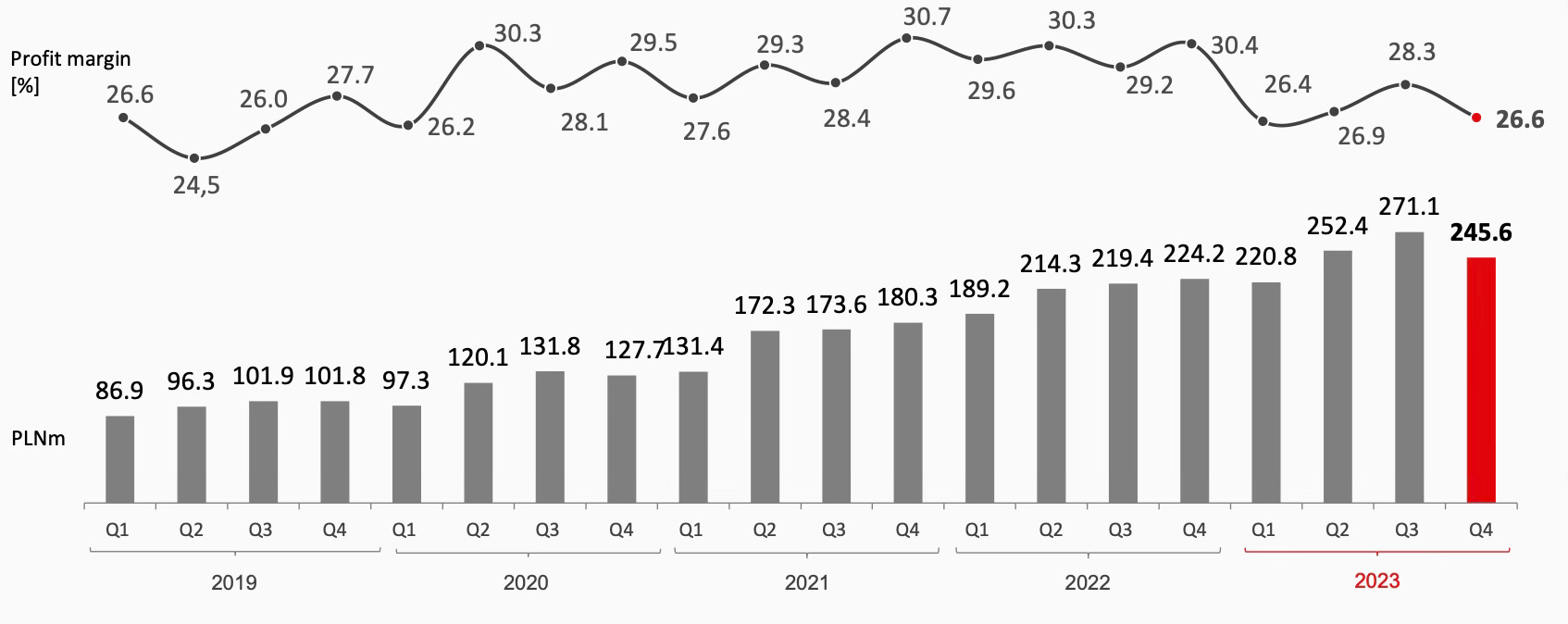

APR maintained solid margins in 2023 despite a challenging market environment. During 2023, the operating margin fell to 8.3% from 9.9% in 2022, but it still remained above the pre-pandemic level of 5.7%. Management attributed the decline to a couple of key factors:

Inflated transport costs.

Inflation (including wage pressure) and business expansion.

Significantly higher finance costs due to interest rate hikes.

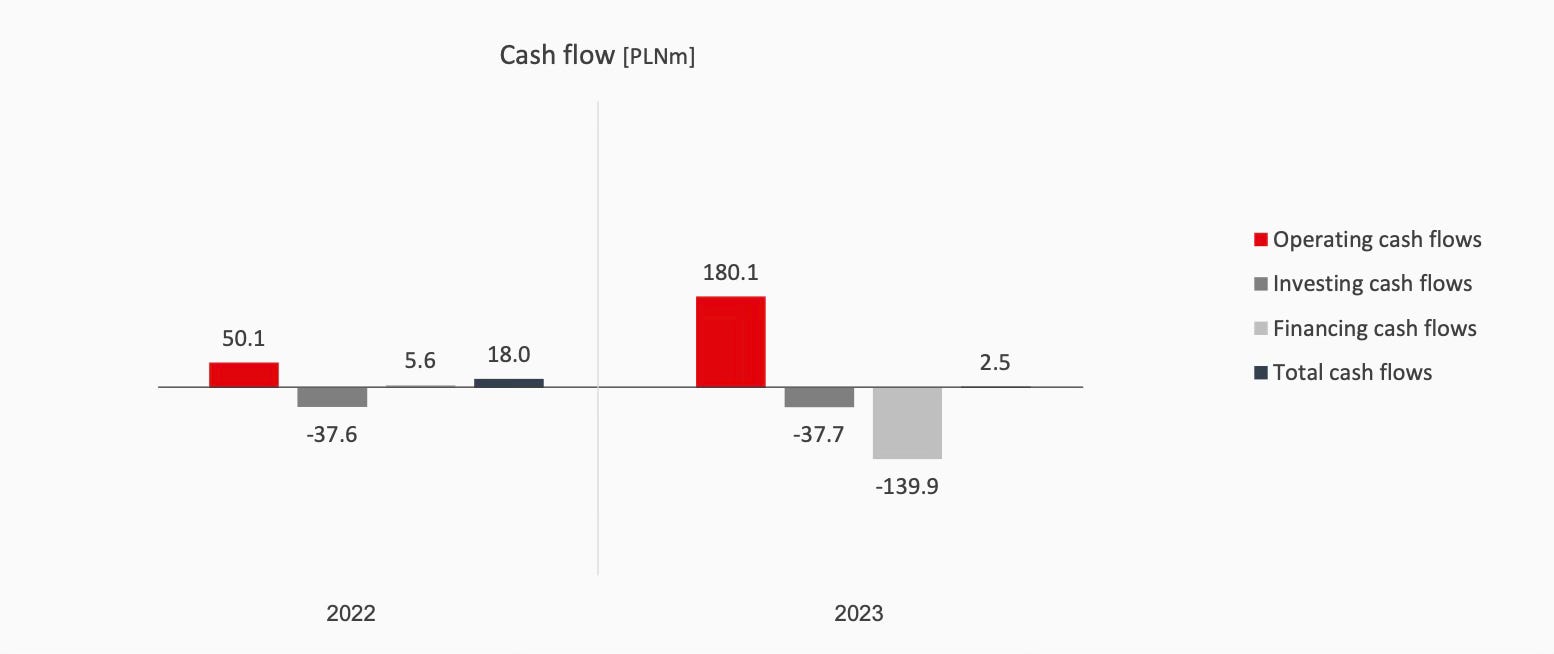

Cash Flow Analysis

APR recorded an operating cash flow of PLN 180.1 million in 2023, representing an increase of over 259% compared to 2022. Part of this increase is attributed to the effective management of working capital requirements, particularly inventory. Despite revenue increasing by 29% in 2023, management managed to limit the growth of closing inventory to just 5%. Management noted that they are satisfied with the current level of inventory and that there will be no need to increase it going forward. The inventory turnover decreased from 158 days at the end of 2022 to 137 days at the end of 2023

Return on Capital

APR's profitability and business model have resulted in a Return on Capital (ROC) of 13% in 2023. The key driver behind the improved double-digit returns over the past couple of years is due to APR’s utilization of its branch network.

APR grew its branches by 2% from 114 at the end of 2022 to 116 at the end of 2023. During the same period, APR has been able to grow the average revenue per branch by 27% from PLN 24.9 million to PLN 31.5 million. Not only has APR been able to increase the number of branches it operates, but it has also significantly increased the average revenue per branch.

During the conference call, management confirmed that the goal was only to open a couple of branches each year going forward. Rather than flooding the market with new branches, APR is looking to optimise the existing branches, which is a less capital-intensive strategy and very much reminds me of the Home Depot strategy, albeit in a different industry.

4. Guidance

The preliminary revenue for Q1 2024 was PLN 994.3 million, an increase of 19% YoY. Management does not provide full-year financial guidance, but management's target is +20% growth, in line with previous years.

Management expects a double-digit increase in employee costs in 2024 based on the new minimum wage laws in Poland, which increased by 18% from January 2024.

Based on the existing foreign exchange rates, management is working towards a net profit margin of 6% in 2024, in line with 2023.

5. Conclusion

APR posted really strong top-line revenue numbers in 2023, with growth accelerating from 2022 primarily due to the positive impact of inflation on sales prices. Looking at the bottom line, APR faced a number of challenges including currency exchange headwinds and rising costs across wages, transport, and financing.

It is apparent that margins will continue to come under pressure in 2024. External data suggests that inflation is falling, meaning that APR will not see this benefit in the form of higher sales prices. To make matters worse, wages are still going to increase due to the new minimum wage laws in Poland.

One possible tailwind could be the reversal of the currency exchange rates to the historical mean. If this were to occur, it would be a welcome boost to earnings, but at this moment, it is more conservative to assume the existing conditions will remain.

For the past number of years, APR has benefited from a combination of favorable currency exchange rates or inflation trends. Now that the tables have turned, I am looking forward to seeing how management reacts to unfavorable conditions in 2024. This will be the perfect environment to appraise management's real competency.

The positive for APR remains its competitive positioning, particularly its success internationally. Based on the current growth rates, export sales should surpass domestic sales for the first time in 2024. Trading at just twelve times forward earnings, APR remains very reasonably valued.

Rating: 3 out of 5. Meets expectations.

If you'd like to support the work of an independent analyst, you can buy me a coffee. The proceeds will contribute to covering the annual running costs of the newsletter.

Join the community of informed investors – subscribe now to receive the latest content straight to your inbox each week and never miss out on valuable investment insights.

If you found today's edition helpful, please consider sharing it with your friends and colleagues on social media or via email. Your support helps to continue to provide this newsletter for FREE!

Happy investing

Wolf of Harcourt Street

Contact me

Twitter: @wolfofharcourt

Email: wolfofharcourtstreet@gmail.com

Great work. I like both APR and CAR, interesting to see how they handle the next year or so.

Nice update, thanks.