Let's Talk About Tax - Part 1

Income Tax - Claiming back overpaid tax

In this week’s edition, I am going to take a look at all things taxation. This has been one of the most requested topics that I have received. The information contained within this edition will relate to Irish residents only. I’m going to break this into a two-part series:

Income Tax

How you can claim back overpaid tax at year end. This is regardless of whether you are an investor or not

Declaring Dividend Income

Asset Appreciation Tax

Capital Gains Tax

Strategies to reduce tax arising from investing

Disclaimer - The information discussed is my own interpretation of the tax guidance in Ireland at this moment in time. If you are in any doubt about your own personal circumstances I suggest you speak with a qualified professional.

Income Tax

For Pay As You Earn (PAYE) workers like myself, our tax is automatically calculated by our employer and deducted from our gross pay. What we receive into our bank account every month (or whatever frequency you are paid) is therefore net of tax. When calculating the tax to subtract from your gross salary, the employer generally tries to spread your tax credits evenly throughout the year so that your net pay is even.

However, there are two important areas that are not included in this allocation. Firstly, the employer does not include all of the allowable tax expenses or credits that can be claimed. Secondly, the employer assumes you are working evenly throughout the entire year. This year in particular many people may have been out of work for varying lengths due to Covid-19. In other years, individuals might have left their job during the year to go travelling.

The above situations can result in an overpayment of tax which means you have paid more tax than you were liable to pay. From about the second week of January onwards the previous years tax return can be accessed. Here is how we go about claiming back the overpayment:

Log onto Revenue.ie

This is the Irish tax and customs website. From here, click on the “sign into myaccount”

Sign into your account

If you have never been onto this site before you will need to register by clicking the “Register Now” button. To register you will need Your PPS Number, Date of Birth, Mobile Number, Email Address and Home Address.

If you are already registered, simply log in using your PPS Number, Date of Birth and Password.

Request Statement of Liability

When you sign in you will see a number of sections. What we are concerned with is PAYE Services. In this section click on “Review Your Tax 2017-2020”.

Next, beside the “Statement of Liability for 2020” click “request”. As you can see below, I have already requested mine so the screen looks a bit different to what you will see when doing it for the first time.

Review you Tax

You will now be brought to your Income Tax Return.

Personal Details

Check that the information in the system that you are seeing is correct for example residency, contact details and bank details (where any overpayments will be paid).

PAYE Income

This gives a summary of how much you were paid by your employer last year and the taxes that were paid. This will automatically be populated so just give it a sense check.

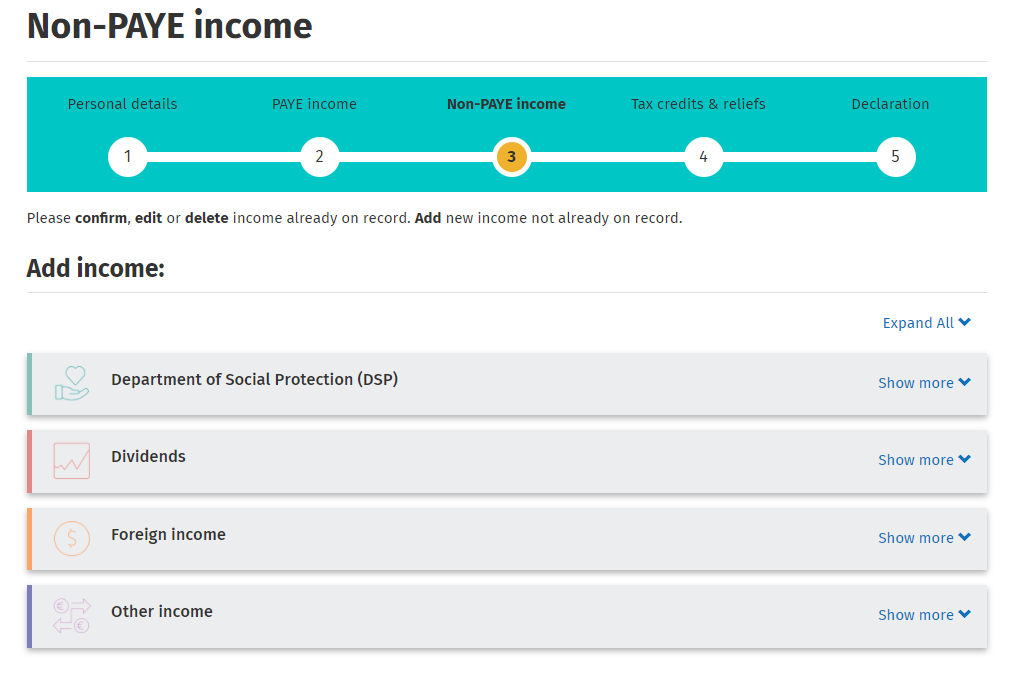

Non PAYE Income

If you received any other income throughout the year other than your salary from your employer you should include it here. One example here might be Dividend Income (See section below).

Tax Reliefs & Credits

Time for the good stuff! In this section we get to add our tax credits and allowable expenses. For a definition of each refer to Personal tax credits, relief and exemptions page on the revenue website. The important thing to remember here is that you will need to retain proof of receipts to support and credits or expenses you are claiming.

The value of a relief or credit will depend on whether it is allowed at the highest rate of income tax that you pay or is restricted to the standard 20% rate. Take the example of a claim of €100. If you pay tax at 40% and you can claim it at this rate, then it will reduce your tax by €40 (€100 x 40%). If the highest rate of tax that you pay is 20%, or the relief is restricted to the standard rate, then the claim of €100 will reduce your tax by €20 (€100 x 20%). You should input the gross amount of the expense or relief (unless instructed otherwise onscreen) and then the revenue system will calculate the actual tax relief amount.

Here are some examples:

Health expenses - Did you have to get any non-routine dental procedures (root canal, crowns) performed that were not covered as part of health insurance? You can request a Med 2 form from your dentist which will support this expense. Health expenses are restricted to 20% so if I had a non-routine dental procedure that cost €750 this would result in €150 of a tax reduction.

Tuition fees - Did you pay third level education fees for you or a dependent?

Stay and Spend (introduced in 2020) - Did you holiday in Ireland after 1 October 2020. If so you can claim relief for holiday accommodation and “eat in” food and drink

Remote Working Relief (new in 2020) - Did you work from home for a lot of this year? If your employer has not paid you an additional €3.20 per day for working from home you can claim a relief on it. You are permitted to claim 10% of the cost of light and heath and 30% of the cost of broadband, apportioned based on the number of days you worked at home. Eg if my broadband cost €600 for the year and I worked 200 days from home this year - €600*30%*(200/365)= €99

Flat Rate Expenses - Is your job included on this list of flat rate expense professions? All employees of the class or group in question can then claim the agreed deduction in their own tax credits.

Declaration

Review the summary and confirm that all of the information that you have input is accurate. Remember that you will need to have copies of all original receipts and retain them for a period of 6 years.

Revenue will be in touch with you via email to let you know once your Statement of Liability is ready to view and here you will be able to see if you have over or under paid tax.

If you have retained receipts or believe you have allowable reliefs for earlier years 2017 to 2019 and you have not done so already, you could request your statement of liability for these years. The “four year rule” means that you can only request reviews or claim refunds from the last four years.

If you’ve found this information useful or you’ve managed to get a tax refund it would be great if you could share it with family or friends so that they can do likewise. This will also help the newsletter to grow.

Dividend Income

Dividends are taxable as part of total income. You will recall from above that when reviewing your tax as part of the “Statement of Liability” there is a section called Non-PAYE income.

In this section, you can add any other income including dividends. When adding the dividends here, the dividends are grouped by region eg Irish dividends, US dividends etc.

The easiest way to figure out how much dividends you have received during the year is to refer to your broker statement. My main broker is DEGIRO and at the end of each year they issue you with an Annual Report. This report will list all of your transactions during the year including purchases, sales, fees, withdrawals, deposits and dividends.

For the dividends received, the amounts are displayed by country and also by gross dividend, withholding tax and net dividend. In my situation, all of the dividends that I receive are from US companies bar one so I do not have a huge amount of input required here.

In the specific case of US dividends, the gross amount is the amount that was declared by the company. The withholding tax relates to the double taxation agreement between Ireland and the US. With this agreement, 15% of the gross dividend is automatically withheld so I receive 85% of the gross dividend as my net dividend. When I am inputting the amount of dividends received for the US I input the gross amount. As an irish shareholder, I am taxable on the gross dividend at marginal rates, but will be entitled to a tax credit for the tax withheld by the company.

Inputting Irish dividends, UK dividends etc follows a similar process so just follow the onscreen instructions. All of the information you need will be contained in your broker statement.

As dividends are taxed as income, the amount you pay in tax will vary depending on your own personal circumstances. For example, if you a single individual who earns more than €35,300 per annum, the dividends will be taxed at the marginal rate of up to 52% once you add in USC and PRSI. On the flip side, if you earn less than €35,300 or you are a retired individual who’s sole income is now dividends you could end up paying significantly less.

Link to Part 2

Hit subscribe below if you have not already done so in order to receive the latest content straight to your inbox each week.

If you enjoy today’s edition, then feel free to share as it, it really helps.

Happy investing

Wolf of Harcourt Street

Contact me

Twitter: @wolfofharcourt

Email: wolfofharcourtstreet@gmail.com

Very helpful article. How are European dividends submitted through the Revenue website? It only lists, Irish, US, UK, Canadian.