Let's Talk About Tax - Part 2

Capital Gains Tax and Tax Mitigation Strategies

This week’s edition is part 2 of the “Let’s Talk About Tax” series. Part 1 covered Income Tax. I would recommend reading this edition first.

In this edition, I am going to take a look at asset appreciation tax including capital gains tax and tax mitigation strategies. The information contained within this edition will relate to Irish residents only.

Disclaimer - The information discussed is my own interpretation of the tax guidance in Ireland at this moment in time. If you are in any doubt about your own personal circumstances I suggest you speak with a qualified professional.

Capital Gains Tax (CGT)

CGT is a tax you pay on any capital gain (profit) made when you dispose of an asset. It is the chargeable gain that is taxed, not the whole amount you receive. The chargeable gain is usually the difference between the price you paid for the asset and the price you disposed of it for. CGT is payable by the person making the disposal. For the purposes of this analysis I am only going to look at CGT related to shares in companies.

On the Revenue website there is a very comprehensive section on CGT on the sale, gift or exchange of an asset which should be your starting point. The CGT rate related to shares is currently 33%. Each tax year, the first €1,270 of your gain or gains (after deducting losses) are exempt from CGT.

When to Pay

For disposals made between:

1 January and 30 November (the initial period), you must pay CGT by 15 December of the same year.

1 December and 31 December (the later period), you must pay CGT by 31 January of the next year.

How to Calculate CGT

The first thing to note is that we only are liable for CGT when we sell a share. We are not liable for CGT on shares that have increased in value in our portfolio but we have not sold. The second thing to note is that we are only liable for CGT on the profit. If we don’t make a profit when we sell then we are not liable for CGT.

As mentioned earlier, the first €1,270 of your gain or gains (after deducting losses) are exempt from CGT. For example, if I bought shares for €1,000 and sold them for €2,000 in 2020 I would have made a profit of €1,000. As I have an exemption of €1,270 I am not liable to pay any CGT on this sale in 2020. Alternatively, if I sold the shares that cost me €1,000 for €3,000 I would have made a profit of €2,000. In this scenario the first €1,270 is exempt so I have a chargeable gain of €730 @ 33% equals €241 of a tax liability.

On the Revenue website there is a fantastic CGT Calculator in excel format that can assist you when calculating any CGT due.

How to Pay CGT

Calculating and paying your CGT liability is all self-declarative. Many people hire a tax advisor to do this but it is possible to do it yourself as long as you are registered on the Revenue website.

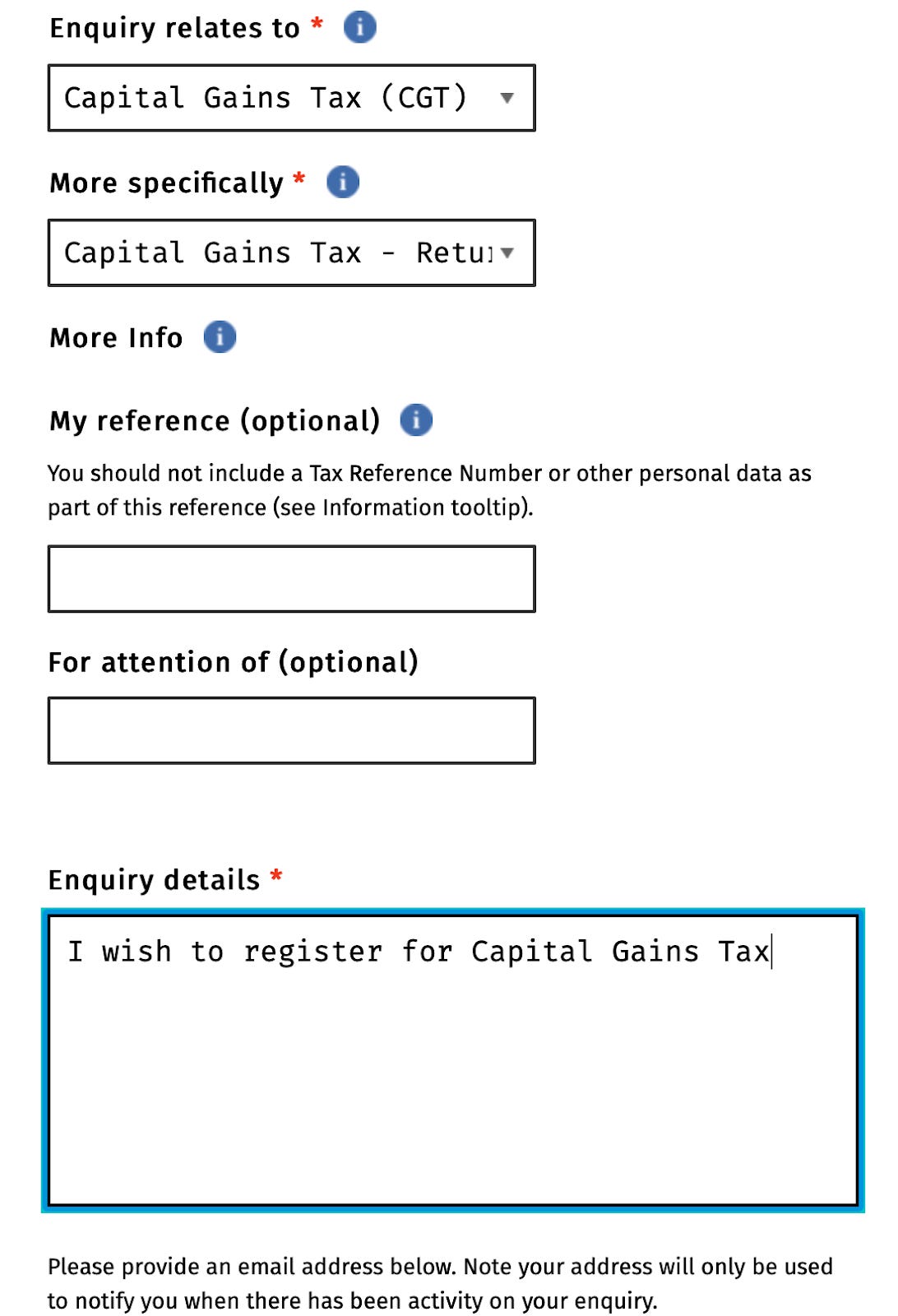

Register for CGT

Even though you are registered on the Revenue website you might not be registered for CGT. To register, click on “My Enquiries” after you have signed in. Then click on “Add New Enquiry” and see below as a sample

After a couple of days you should receive an email confirming that you are now registered for CGT.

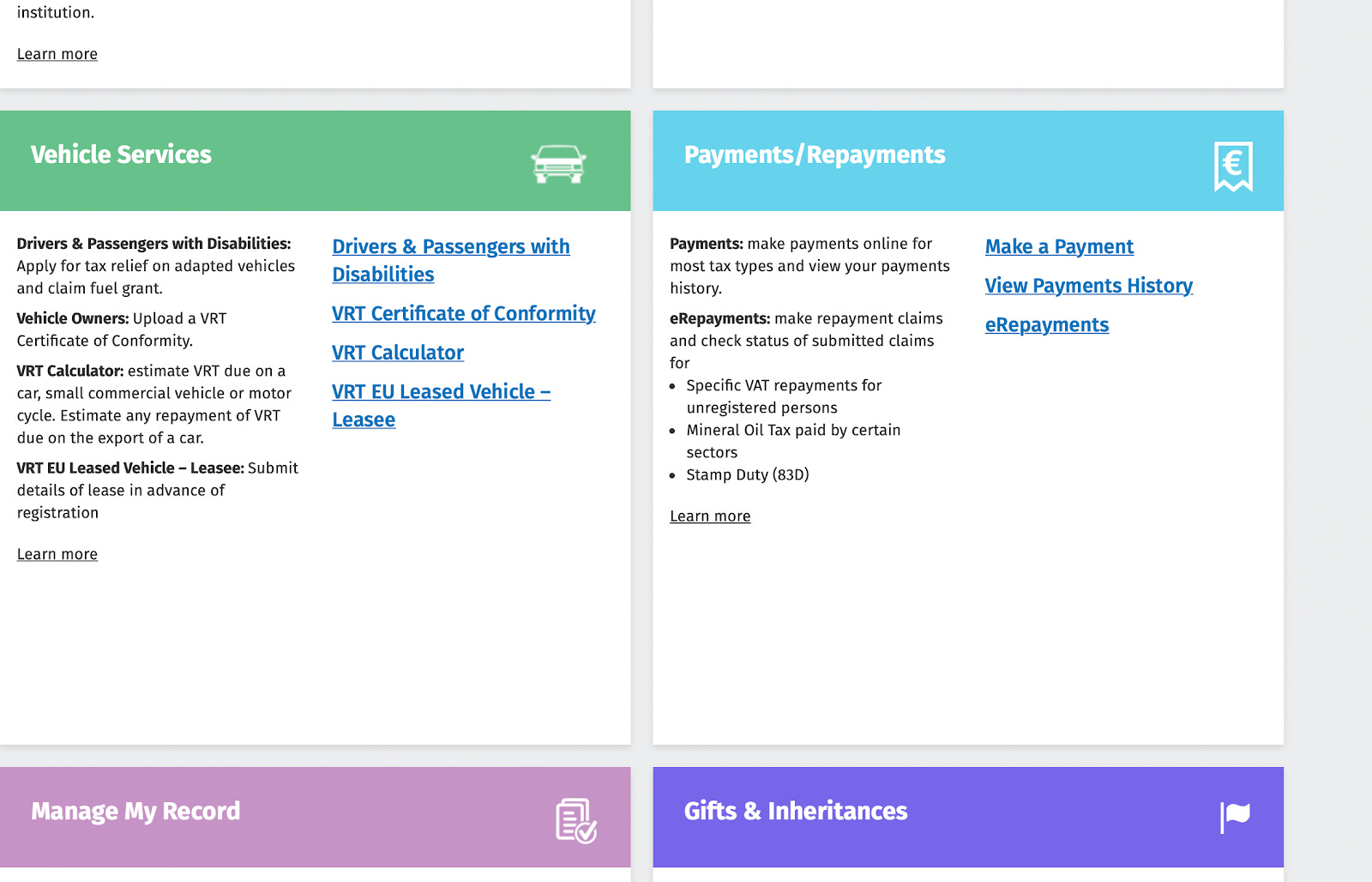

Pay the CGT

On your account homepage, navigate to the “Payments/Repayments” section and click on “Make a Payment”.

Select the payment you are making as “Tax”. Then select “Capital Gains Tax”. When entering the amount to pay you are entering the actual amount you need to pay. Do not confuse this with your gains that are liable for tax.

How to File CGT

You must file by 31 October in the year after the date of disposal. You must do this even if no tax is due because of reliefs or allowable losses.

To file the CGT return you need to fill in a form (I hate forms). For most people the relevant form will be the CG1. I suggest referring to the website if you are in doubt as the form differs slightly if you are self-employed or you are jointly assessed.

Where filling the the form you will need to include:

a description of the asset of assets disposed

the amount you received for the asset or assets

any reliefs you claimed

the chargeable gain or loss

your taxable gain

The amount of CGT paid (already paid in advance)

Once you have completed the form you can upload it onto your Revenue account or post it to your local Revenue office.

Tax Mitigation Strategies

Unfortunately it is practically impossible to get away without ever having to pay tax on your investments. However, there are a number of strategies that could be executed to try to minimise your tax liability. Bear in mind that you only pay tax when you are making money so do not let the idea of tax scare you off from investing.

Annual Allowance

Each tax year, the first €1,270 of your gains are exempt from CGT. If you are a long term investor, you could sell shares with gains of €1,270 each year and pay no tax. This method of trimming your portfolio means that you are not leaving all of the tax liability until the later years. You could then reinvest the proceeds back into your portfolio and start the cycle again.

Tax-Loss Harvesting

Tax-loss harvesting is the selling of shares at a loss to offset a capital gains tax liability. Let’s assume that you have sold shares with a gain of €2,000 for the year. However, you have some shares sitting in your portfolio in a company performing badly and are down 50% compared to the price when you bought them. In this scenario, you could sell €800 worth of shares that previously cost you €1,600 thereby resulting in a €800 loss. This €800 loss can be offset against the €2,000 gain leaving a €1,200 net gain. This amount is less than the €1,270 annual allowance therefore no CGT tax will be payable.

An important concept to be aware of here is the four week rule. If you dispose of shares for a loss you must wait four weeks before you can buy them back to be able to utilise the losses against other assets. If you sell and buy back within four weeks, the losses can only be used against the subsequent disposal of the acquired shares.

Pension

Investing in Ireland is taxed heavily. However, there are significant tax reliefs available for pension contributions. The relief is limited based on your age and increases the closer you get to retirement. For example, consider a 29 year old earning €40,000 that contributes 15% of their salary to their pension per annum amounting to €6,000 or €500 a month. In accordance with the revenue limits below, this pension contribution will qualify for relief from income tax. This effectively means that, where the higher rate of income tax is 40%, €500 contribution to a pension per month will only have a net cost to the individual of €300. Had the individual not made the contribution, the other €200 would have gone to the government as income tax.

I personally have a pension and my own individual investment portfolio. My own approach is to maximise my pension contributions to avail of the significant tax reliefs and then invest the remainder of my disposable income into individual stocks. For PAYE employees, your pension contributions are all handled by your employer. The downside to employee pensions is that you cannot decide what individual stock that your pension is invested in and you cannot draw it down until retirement.

If you are self employed or own a company you have the option to set up a Self-Directed Pension. Typically it is directors of businesses that opt to establish such schemes as a way to fund their retirement income, and to control how, what and when they invest the funds. It is run by the director/employer and not by a traditional pension provider. If you are self-employed or own a company this is definitely an area worth investigating.

Investing through a company

If you already have a company, you could invest through the company or a Director’s pension. By doing this, the money you have earned never has to leave the company and therefore does not get taxed at the higher income tax marginal rate of 52% when including USC and PRSI. Instead, corporation tax is 12.5% on trade income or “active income” and 25% on non-trading income or “passive income”.

However, if you are not self-employed or do not have a company already, I do not recommend setting up a company purely to invest. Firstly, if you set up a company purely to invest you are going to have to pay annual compliance and accounting fees beginning at about €500. The paperwork related to investing through a company is also far more onerous than investing as an individual.

Additionally, if you are a PAYE earner you could be paying tax at the higher marginal rate of 52% when including USC and PRSI. Once you receive your salary into your bank account it has been taxed once. Consider this the tax on the capital. When you invest it and make a gain you will pay tax a second time at disposal. Call this the tax on profit. If you set up a company purely to invest, you will still pay tax once when you receive your salary. When you put the money into the company, the money will be taxed a second time in the company. Then, when you try to get the money out of the company and into your hands it will be taxed a third time.

The benefit of a company is gained by having income earned through the company and then investing this without the money ever leaving the company. This means that the initial tax on capital is 12.5% or 25% vs as much as 52%. If you are setting up a company purely to invest, your money has already been taxed before you put it into the company and the benefit is not realised.

Readers Questions

Q. Which instruments are better from a tax point of view?

A. In order of tax efficiency:

Pension - Tax deductible contributions - cannot access until retirement

Individual stocks - CGT of 33% - €1,270 annual exemption

ETF/Index funds - Exit tax of 41% on gains - no annual exemption (there is also an 8 year deemed disposal rule meaning you have to calculate and pay the theoretical tax that would be liable after 8 years even if you don’t sell)

Dividends - Income tax marginal rate of up to 52% - no annual exemption

Q. Can expenses towards investing be subtracted from CGT? For example, if I pay a yearly subscription to a stock information service, can this be included as a cost to lower cgt.

A. The short answer here is no. The only expenses that you can offset are the brokerage or commission costs involved in selling the stock.

Q. What are the penalties for paying CGT late?

The surcharge for paying CGT late is a percentage of the total tax payable for the year for which the return is late. The percentage amount is set according to the length of the delay in filing. The amount of the surcharge is also subject to an overall cap.

The surcharge is calculated as follows:

5% of the tax liability for the year of assessment to which the tax return relates, subject to a maximum of €12,695, where the tax return is delivered within two months of the filing date;

10% of the tax liability for the year of assessment to which the tax return relates, subject to a maximum of €63,485, where the tax return is not delivered within two months of the filing date.

Hit subscribe below if you have not already done so in order to receive the latest content straight to your inbox each week.

If you enjoy today’s edition, then feel free to share as it, it really helps.

Happy investing

Wolf of Harcourt Street

Contact me

Twitter: @wolfofharcourt

Email: wolfofharcourtstreet@gmail.com

Regarding ETFs--it might be worth adding that the "deemed disposal" rule requires you to pay tax on an ETF every 8 years even if you haven't sold. This rule is peculiar to Ireland and greatly detracts from index fund/ passive strategies because the compounding effect loses much of its power

Hi Wolf. It might be outside the scope of the article but an EIIS is pretty tax efficient, albeit risky, as you are investing in a start up. Nice way to get in early like some of the VCs and, if it all goes wrong, you’ve only lost, at most, 60% of your investment.