Executive Summary

Q2 2023 deliveries totalled 23,520 vehicles, with a decrease of 6% YoY and a more significant decrease of 24% QoQ. July 2023 deliveries showed positive growth, with 20,462 vehicles delivered, marking a substantial 104% YoY increase and nearly equaling Q2's total deliveries.

NIO faced challenges in terms of declining total revenues, primarily driven by decreases in vehicle sales. These declines were attributed to a lower average selling price caused by increased deliveries of lower-priced models and reduced delivery volume. However, the growth in other sales, particularly from used cars, accessories, and power solutions, helped partially offset some of these declines.

NIO experienced a decline in gross margin, vehicle margin, and gross profit in the second quarter of 2023 compared to the same period in 2022 and the first quarter of 2023. These declines were influenced by factors such as changes in product mix, battery cost fluctuations, increased sales of lower-margin used cars, and variations in delivery volumes.

NIO's liquid assets have decreased by 22% from Q1 2023 to $4.3 billion in Q2 2023. Despite management's expectation of improved operating cash flow due to increased delivery volume in Q3 and beyond, concerns remain about the sustainability of cash flow. The current cash burn rate suggests that NIO might need to secure additional financing, potentially leading to further shareholder dilution, considering its existing debt load.

While the Q3 vehicle delivery guidance surpassed Wall Street analysts' estimates, it should not be considered a success based on management's previous target of 20,000 deliveries per month. Management's reaffirmation of the 20,000 delivery target as recent as June for the rest of 2023 contrasts with the current guidance, which is 5%-8% below that target.

In this report, I will cover the following:

Key Highlights

Wall Street Expectations

Business Activity

Financial Analysis

Guidance

Conclusion

1. Key Highlights

Revenue: $1.21 billion -15% year-over-year (YoY)

Vehicles: $991 million -25% YoY

Other: $219 million +120% YoY

Gross Profit: $12 million -94% YoY

Net Loss: $835 million compared to a loss of $412 million YoY

2. Wall Street Expectations

Revenue: $1.27 billion (miss by 4%)

ADS Earnings per Share: -0.36 (miss by 42%)

Source: Koyfin

3. Business Activity

Deliveries of vehicles were 23,520 in Q2 2023, including 10,492 premium smart electric SUVs and 13,028 premium smart electric sedans. These figures represent a decrease of 6% compared to the second quarter of 2022 and a more significant decrease of 24% compared to the first quarter of 2023. While this was a very poor return, this information was already well known as NIO disclose delivery numbers at the end of each month.

NIO experienced a positive trend in vehicle deliveries in July 2023, with 20,462 vehicles delivered. This number signifies a substantial YoY increase of 104% and almost equivalent to the total deliveries in Q2.

In July, NIO became the best-selling brand in the premium electric vehicle segment for vehicles with a transaction price over RMB 300,000 ($41,200). NIO claimed an impressive 59% market share in this premium segment, as per CATARC retail statistics.

NIO continued its product lineup expansion with the delivery of multiple new models, including the smart electric tourer ET5T and the flagship SUV ES8. These new models contributed to NIO achieving high-quality deliveries for a total of five new models in the second quarter.

NIO's product safety received significant recognition. The smart electric mid-size sedan ET5 and the mid-large SUV EL7 received a five-star safety rating from Euro NCAP, validating NIO's commitment to safety.

NIO showcased its advancements in assisted and intelligent driving technologies, with over 100,000 users activating the Navigate on Pilot Plus (NLP Plus) feature and a high penetration rate of 53%.

NIO's sales and service network continued to expand, with 420 NIO houses, NIO spaces, and pop-up stores in 143 cities, along with extensive service and delivery centers. Efforts were being made to further expand user touch points, sales channels, and the sales team in China to enhance sales capabilities.

NIO had a significant presence in the charging and swapping network, boasting 1,747 power swap stations and over 27 million battery swaps. The company has a robust charging infrastructure, including power chargers, destination chargers, and a connected map to over 1.36 million third-party chargers globally.

4. Financial Analysis

During the quarter, NIO's total revenues were $1.21 billion representing a decrease of 15% compared to the second quarter of 2022 and a further decrease of 18% compared to the first quarter of 2023.

Vehicle sales in Q2 2023 accounted for $991 million of total revenues. This reflected a substantial decline of 25% from the second quarter of 2022 and a decrease of 22% from the first quarter of 2023. The decline in vehicle sales was primarily attributed to a lower average selling price, due to a higher proportion of deliveries for the ET5 and 75 kWh standard-range battery pack models, as well as a decrease in delivery volume. A back of the napkin calculation suggests that the average selling price in Q2 2023 was $51k compared to $61k in Q2 2022.

Other sales, which include sales of used cars, accessories, provision of power solutions, and auto financing services, reached $219 million for the quarter. This represented a significant increase of 120% from the second quarter of 2022 and a more modest increase of 9.3% from the first quarter of 2023. The increase in other sales was mainly attributed to higher sales of used cars, accessories, and power solutions, driven by the continued growth of NIO's user base.

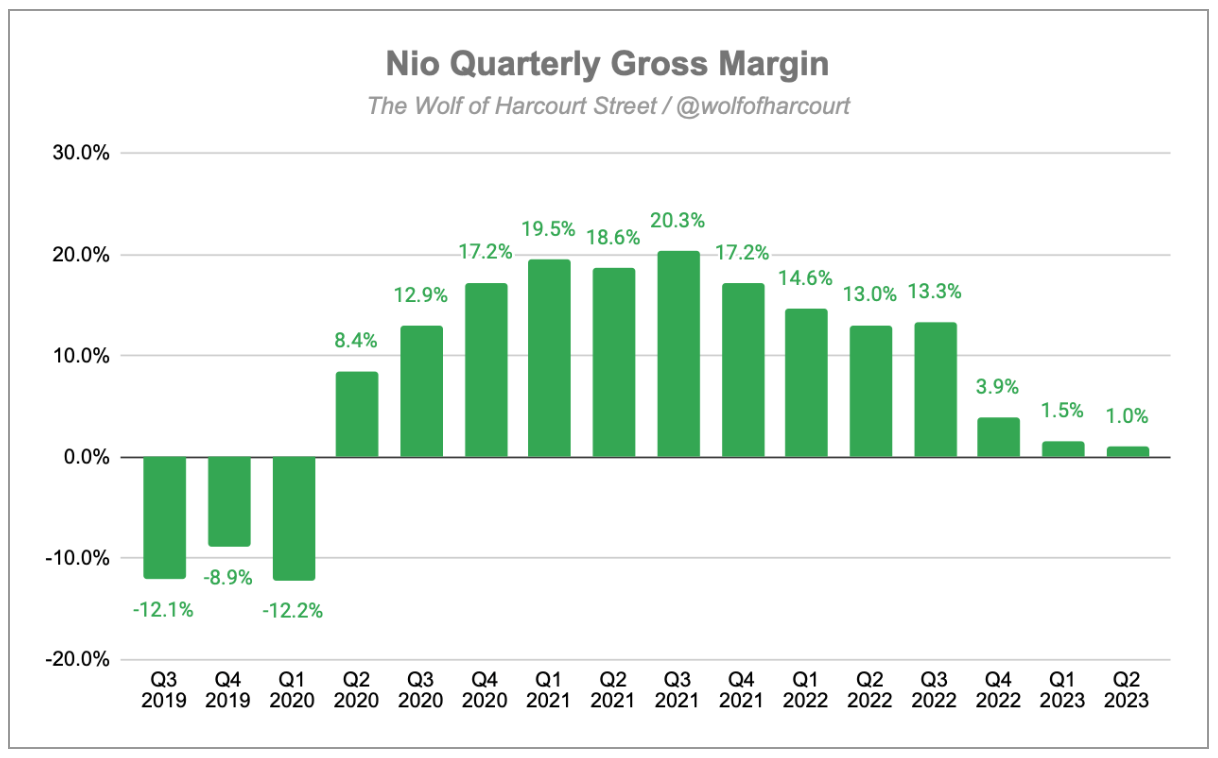

The gross margin for the second quarter of 2023 was 1.0%, a significant drop from 13.0% in the same period of 2022 and a slight decrease from 1.5% in the first quarter of 2023. This is the lowest gross margin since Q1 2020. The decrease in gross margin is primarily attributed to a reduced vehicle margin.

The vehicle margin for the second quarter of 2023 was 6.2%, which is considerably lower than the 16.7% reported in the same quarter of 2022 and slightly higher than the 5.1% in the first quarter of 2023. The decrease in vehicle margin is mainly due to changes in the product mix, even though it was partially offset by a decrease in battery cost per unit.

Operating expenses (OpEx) increased by 36% YoY to $850 million during the quarter. The fall in revenue coupled with the increase in OpEx has caused the OpEx ratio to balloon to 70%, the highest since Q1 2020.

The main components here include sales, general and operative expenses (SG&A), which increased by 25% to $394 million due to higher personnel costs related to sales functions, expanded sales and marketing activities (including new product launches), and greater rental and related expenses related to the company's sales and service network expansion.

On the conference call, management noted a deficiency in its sales team and product selling capabilities compared to market competitors like BMW and Mercedes. The company took active measures from June to expand its sales network and enhance personnel strength to improve user satisfaction, test drives, and lead conversion. The goal is to support new orders of 30,000 units per month through increased sales network and personnel, with initial capability expected by the end of September and full effect from October.

Research and development (R&D) expenses increased 57% to $461 million due to increased personnel costs within R&D functions, higher share-based compensation expenses recognized in Q2 2023, and additional design and development costs associated with new products and technologies.

Cash Flow Analysis

Unfortunately, NIO does not provide any cash flow statement in its quarterly earnings.

However, we are provided with the Balance Sheet. At the end of Q2, NIO reported liquid assets (cash and cash equivalents, restricted cash, short-term investment and long-term time deposits) of $4.3 billion. This has fallen by 22% from $5.5 billion at the end of Q1 2023. NIO is clearly burning cash having had $6.6 billion of liquid assets at the end of Q4 2022.

On the conference call, management noted that operating cash flow is expected to improve significantly as delivery volume ramps up in Q3 and beyond. The company also made reference to the $740 million strategic investment from CYVN (an investment vehicle wholly owned by the Abu Dhabi Government). Based on the current cash burn run rate of $1.15 billion per quarter, NIO could have to raise additional finance within the next eighteen months unless the cash burn slows dramatically. This is far from ideal given that NIO already has $2.6 billion of debt on its Balance Sheet meaning further shareholder dilution is almost inevitable.

5. Guidance

In Q3 2023, NIO expects deliveries of vehicles to be between 55,000 and 57,000, representing an increase of approximately 74% to 80% YoY. Total revenues in Q3 2023 are expected to be between $2.61 billion and $2.69 billion, representing an increase of approximately 45% to 50% YoY.

NIO anticipates achieving a double-digit gross profit margin in Q3 and a 15% margin in Q4. Management confirmed that the impact of price reductions has been accounted for in its projections.

Following a question from an analyst on the conference call, management noted that the OpEx budget for the next year is not finalized, but indications suggest continuity in R&D investment, similar to this year's quarterly range of $410 million to $480 million. Growth in SG&A expenses is anticipated for next year due to more aggressive sales targets, market activities, and events, but the percentage of total sales revenue may decrease due to delivery volume and operating efficiency improvements.

6. Conclusion

This was a really disappointing quarter from NIO but it had been well sign-posted and should not have come as a surprise to anyone who follows the company closely.

This quarter, I was primarily focused on the discussions about future guidance. Some analysts argue that exceeding Wall Street's estimate of 48,000 vehicle deliveries for Q3 was a significant achievement. However, I don't agree with this assessment. I base my evaluation on management's actions and statements, not on the opinions of Wall Street analysts. As recently as June 9th, management confirmed the goal of delivering 20,000 vehicles per month for the rest of 2023, equating to 60,000 for Q3. Therefore, the current guidance falls 5%-8% short of this target.

In addition, despite the impressive July delivery figures, it seems that deliveries have been pulled forward from other months. During the conference call, management predicted reduced delivery volumes for August and September due to adjustments in power swap benefits. The cancellation of free power swaps for new orders from August 1st prompted a surge in July orders, impacting the delivery count for that month. The anticipation is that NIO won't achieve 20,000 monthly deliveries until the fourth quarter of this year.

Finally, it appears that cancelling the free battery swap policy admits implies the endeavour was never going to be a profitable one, even at scale. One positive of this is that more users are expected to pay for battery swap services, leading to increased revenue. With the introduction of the third-generation power swap stations, the efficiency and profitability of the power swap business are improving. Charging users separately for electricity costs and implementing a service fee for each swap should contribute to improved margins in the power swap business.

Question marks remain when it comes to future growth and the pathway to profitability.

Rating: 2 out of 5. Not meeting expectations.

Disclosure: The author holds a long position in NIO.

Hit subscribe below if you have not already done so in order to receive the latest content straight to your inbox each week.

If you enjoy today’s edition, then feel free to share as it, it really helps.

Happy investing

Wolf of Harcourt Street

Contact me

Twitter: @wolfofharcourt

Email: wolfofharcourtstreet@gmail.com