NIO: Record revenue and deliveries for six quarters

Nio Inc. Q3 2021 Earnings Analysis

Today, I analyse the Q3 2021 earnings report of NIO Inc (Ticker: NIO), which was released on 9 November 2021. NIO reports earnings in RMB and US$; all of the figures and comparatives referenced in this report are in US$.

In this report, I will cover the following:

Key Highlights

Wall Street Expectations

Vehicles

Income Statement

Balance Sheet

Cash Flow

Guidance

Conclusion

1. Key Highlights

Revenue: $1.52 billion +128% year-over-year (YoY)

Vehicles: $1.34 billion +113% YoY

Other: $0.18 billion +375% YoY

Gross Profit: $309 million +259% YoY

Net Loss: $130 million compared to a loss of $154 million YoY

2. Wall Street Expectations

Revenue: $1.46 billion (beat by 4%)

ADS Earnings per Share: -0.09 (miss by 55%)

Source: Nasdaq

3. Vehicles

Deliveries of vehicles were 24,439 in Q3 2021, including 5,418 ES8s, 11,271 ES6s and 7,750 EC6s, representing an increase of 100% YoY and an increase of 12% from Q2 2021.

NIO delivered 3,667 vehicles in October 2021, representing a decrease of 28% YoY due to restructuring upgrades of the manufacturing lines, preparation for the introduction of new products and supply chain volatilities. At the end of October, cumulative vehicle deliveries were 145,703.

On the conference call, CEO William Li stated that ‘demand continues to be strong and our new orders reached a new record high in October’.

4. Income Statement

During the quarter, NIO grew its top line by 122% YoY. Nio has reported triple-digit revenue growth for six consecutive quarters. Gross profit is following a similar growth trajectory and increased by 259%, with gross margin also improving from 13% to 20% YoY.

Other revenue continued to outpace Vehicle revenue in Q3 growing over three times as fast. Vehicle revenue still accounts for over 88% of Nio’s revenue, down from 94% one year ago.

The increase in gross margin from 13% to 20% is a result of an increase in gross margins in both areas of the business.

Why are margins improving?

Vehicle margins improved due to higher average selling prices and lower material costs. On the conference call, Nio stated that a 20% vehicle gross margin was the target for 2022, with a long-term target of 25% based on an annual production of 300,000 vehicles.

Other margins improved due to the sale of automotive regulatory credits. On the conference call, it was explained that the majority of the automotive credit sales were realised in Q3 and that significant revenue was not expected in Q4. Of the $181 million in Other revenue, half related to automotive credit sales

The sale of automotive credits is not sustainable over the long-term. Instead, investors should focus on the improvement in vehicle gross margin of 4% until battery services become a major component of revenue. The overall gross margin has been on an upward trend since Q2 2020.

Operating expenses increased by 105% YoY to $463 million during the quarter. The main drivers here included the following: sales; general and operative expenses, which increased by $145 million to $283 million due to the increase in headcount costs in sales and service functions; and costs related to sales and service network expansion. This is not surprising given that NIO has been increasing the number of job opportunities posted on LinkedIn over recent months, particularly in Europe as it gears up for expansion in this market.

Overall, NIO’s revenue has caught up with its spending on operating expenses over recent quarters, meaning that the operating expense ratio is trending downwards over time.

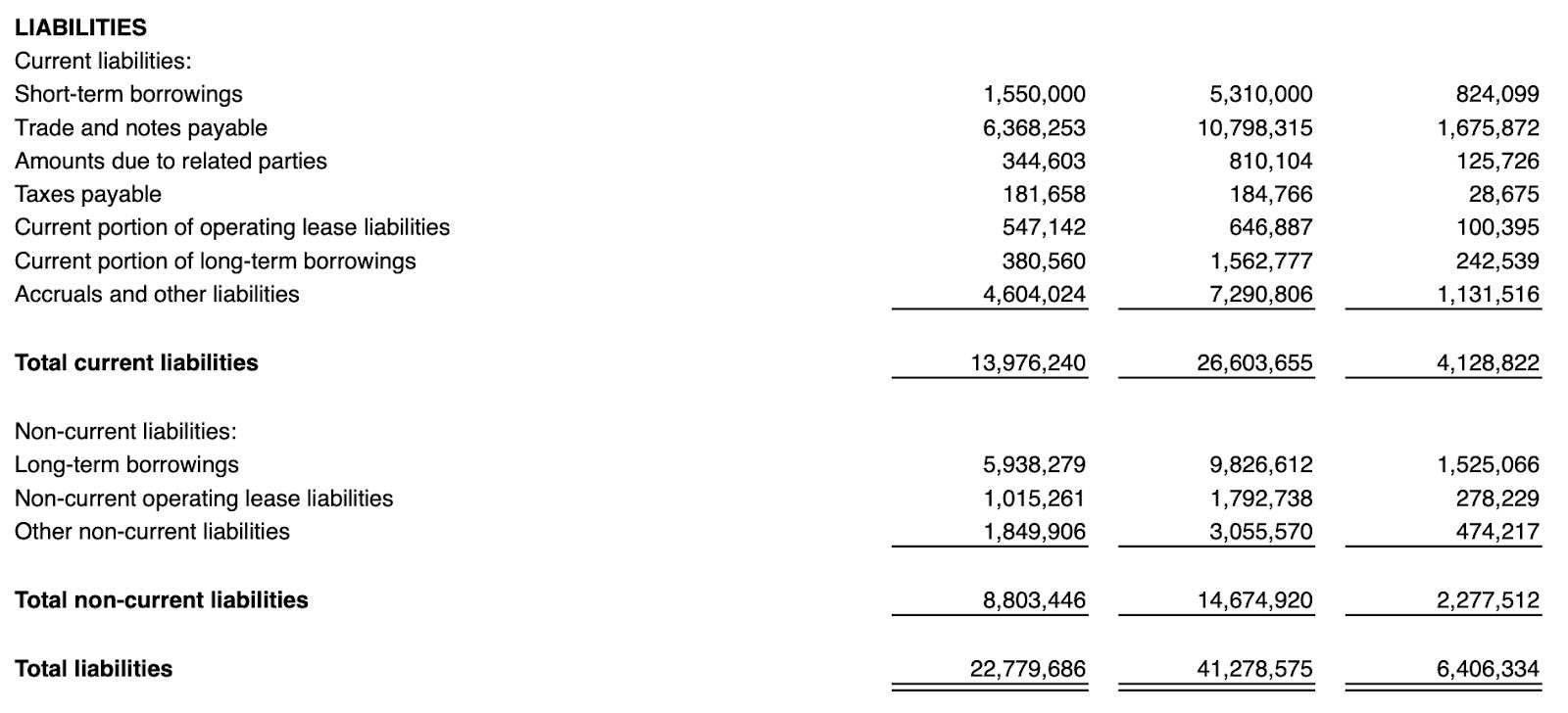

5. Balance Sheet

Observations

Over $3.9 billion in cash and cash equivalents

Total Liabilities as percent of Total Assets is 60%

Current Assets to Current Liabilities ratio of 2.04

Inventory balance making up less than 3% of total assets meaning the impact of the risk of impairment is low

Quite a bit of debt on the balance sheet with a combined $2.3 billion in short-term and long-term debt which has almost doubled since the end of 2020

6. Cash Flow

Unfortunately, NIO does not provide any cash flow statement in its quarterly earnings. This is a personal frustration of mine, and it means that we will have to wait for the annual report for any details about this.

7. Guidance

In Q4 2021, NIO expects deliveries of the vehicles to be between 23,500 and 25,500, representing an increase of approximately 35.4% to 46.9% YoY. The lower end of this delivery range would represent a decrease of approximately 3.8% from Q3 2021, while the higher end of this range would represent an increase of approximately 4.3%.

Total revenues in Q4 2021 are expected to be between $1.46 billion and $1.57 billion, representing an increase of approximately 41.2% to 52.2% YoY. The lower end of this revenue range would represent a decrease of approximately 4.4% from Q3 2021, while the higher end of this range would represent an increase of approximately 3.1%.

8. Conclusion

This was a solid quarter from NIO against the backdrop of manufacturing line upgrades and supply chain constraints. Q4 delivery guidance might appear light, but the reason for this is that the manufacturing lines in October were out of action for 15 days due to upgrades. Vehicle margins are improving, and the long-term path laid out by management shows a clear path to profitability.

As touched on earlier, the demand for Nio vehicles remains strong. Management confirmed that when the NIO House opened on 30 September in Norway, ‘after the test drive, one-fourth of the users [had] placed orders for our products’. NIO has further plans to enter five additional countries in Europe in 2022.

In September, NIO launched the 75-kWh standard-range battery pack, which has higher energy density, longer drive range and lower cost compared with the 70-kWh battery pack. This will start being delivered in late November.

There are many reasons to remain optimistic.

On Wednesday, 11 November, the day after earnings were released, NIO closed the session down 2%.

Rating: 3 out of 5. Meets expectations.

Disclosure: The author holds a long position in NIO.

Contact me

Twitter: @wolfofharcourt

Email: wolfofharcourtstreet@gmail.com

Hit the subscribe button below if you have not already done so in order to receive the latest content straight to your inbox each week. By hitting the archive button you can view all of my previous newsletters on the website.

Happy investing

Wolf of Harcourt Street

Disclaimer: I am not a financial adviser and I am not here to give specific financial advice. The opinions expressed are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product. The information is based on personal opinion and experience, it should not be considered professional financial investment advice. There is no substitute for doing your own due diligence and building your own conviction when it comes to investing.

Wolf, do you know what the other 50% of the “other” revenue relates to? Also, in terms of the regulatory credits, I assume, like Tesla, Nio is not factoring that as a long term revenue driver and is just going to ride the wave for as long as it lasts? Looking forward to their European expansion in the hopes of getting a test drive in the near future! That’ll have to do me until I can afford a Lucid Air. 😃