In this report, I will cover the following:

Overview

Customers

Capitalisation

Revenue & Margins

Balance Sheet and Cash Flow

Stock Price History

Competitors

Management and Ownership

Risks

Opportunities

Valuation Multiples

Investment Strategy

PayPal Holdings, Inc.

Ticker: PYPL

Sector: Financial Services

Market Cap: $215.3 billion

1. Overview

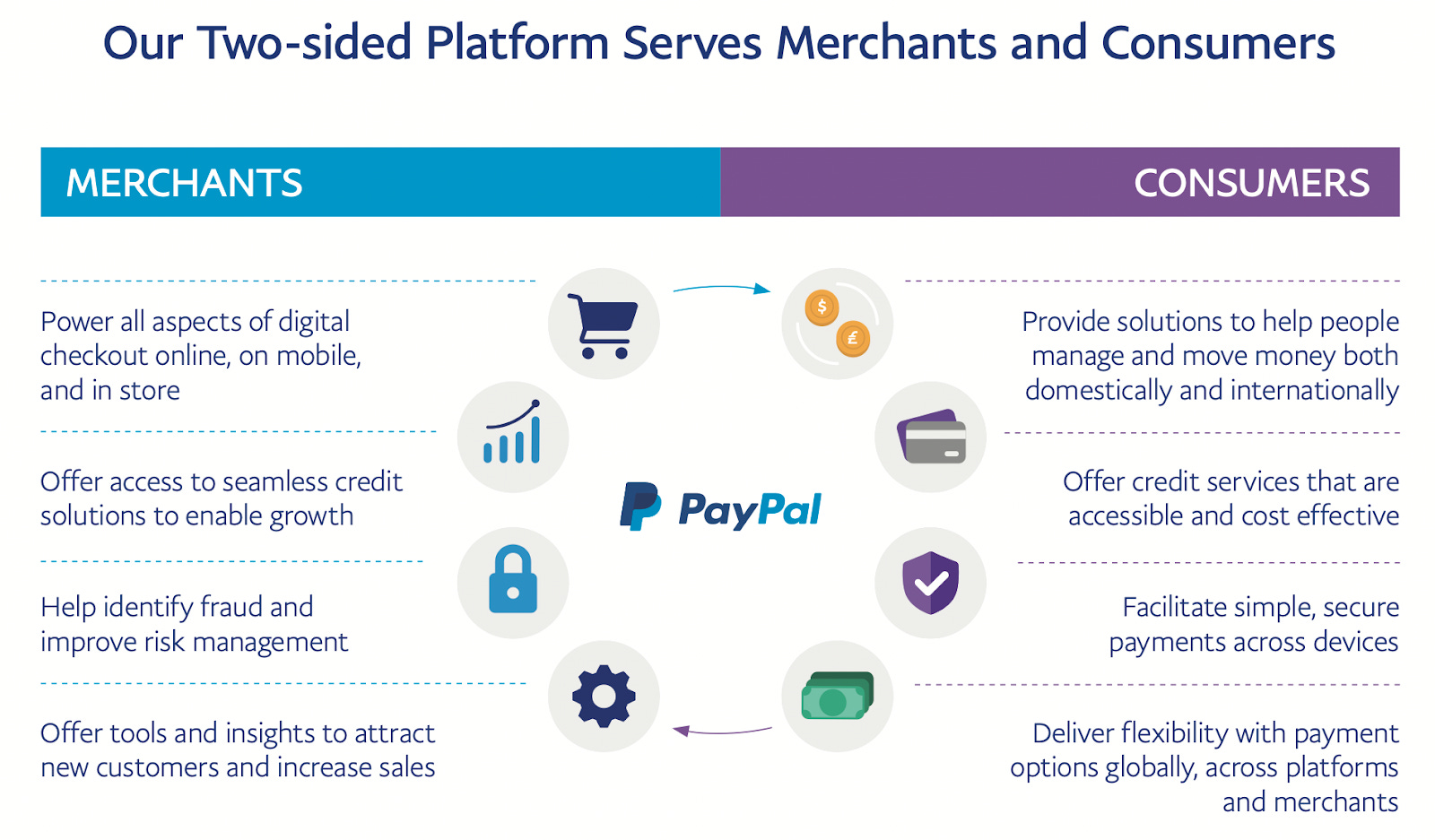

PayPal Holdings, Inc. was incorporated in Delaware in January 2015 and is a leading technology platform and digital payments company that enables digital and mobile payments on behalf of merchants and consumers worldwide. PayPal’s mission is to ‘democratize financial services to improve the financial health of individuals and to increase economic opportunity for entrepreneurs and businesses of all sizes around the world’. Their goal is to enable merchants and consumers to manage and move their money anywhere in the world, anytime, on any platform, and using any device when sending payments or getting paid. PayPal also facilitates person-to-person (‘P2P’) payments through the PayPal, Venmo, and Xoom products and services and simplifies and personalized shopping experiences for consumers through the Honey Platform.

PayPal earns revenues primarily by charging fees for completing payment transactions for customers and other payment-related services that are typically based on the volume of activity processed on their payments platform. PayPal generally does not charge consumers to fund or draw from their accounts; however, they generate revenue from consumers on fees charged for foreign currency conversion and instant transfers from their PayPal or Venmo account to their debit card or bank account, as well as from interest and fees from their credit products. PayPal also earns revenue by providing other value added services, which comprise revenue earned through partnerships, merchant and consumer credit products, referral fees, subscription fees, gateway services, and other services that are provided to merchants and consumers.

2. Customers

At the end of Q3 2021, PayPay had 416 million active accounts up 15% year-over-year (YoY) consisting of 383 million consumer active accounts and 33 million merchant active accounts. PayPal defines an active account as ‘an account registered directly with PayPal or a platform access partner that has completed a transaction on our Payments Platform or through our Honey Platform, not including gateway-exclusive transactions, within the past 12 months’.

During Q3 2021, Total Payment Volume (TPV) grew 26% to $310 billion. PayPal defines total payment volume as ‘the value of payments, net of payment reversals, successfully completed on our Payments Platform or enabled by PayPal via a partner payment solution, not including gateway-exclusive transactions’. This increase comes even as eBay's TPV declined by 45% in the quarter and is now approximately 3% of the overall TPV. Excluding eBay, our volumes grew by 31%.

For some background context here, eBay purchased PayPal in 2002 and later spun it out in 2015. As part of this arrangement it was with the agreement that PayPal would keep managing payments for a five-year transition period. From 1 June 2021, eBay now pays its sellers directly rather than through PayPal.

3. Capitalisation

On 15 February 2002, PayPal went public for the first time, its stock exploding by 55% the first day and raising over $70 million. In July 2002, eBay announced that it would be acquiring PayPal for $1.5 billion, and it was made official in October.

In 2015, eBay decided to spin-off PayPal into its own public company. Under the terms of the spin-off, each eBay investor as of 8 July 2015, received one share of PayPal stock per eBay share owned. PayPal opened its first day at $41.46.

Today, the PayPal share price trades at $191.28 meaning that if you had invested at the second IPO date you would have almost 5x your investment in 6 years.

4. Revenue and Margins

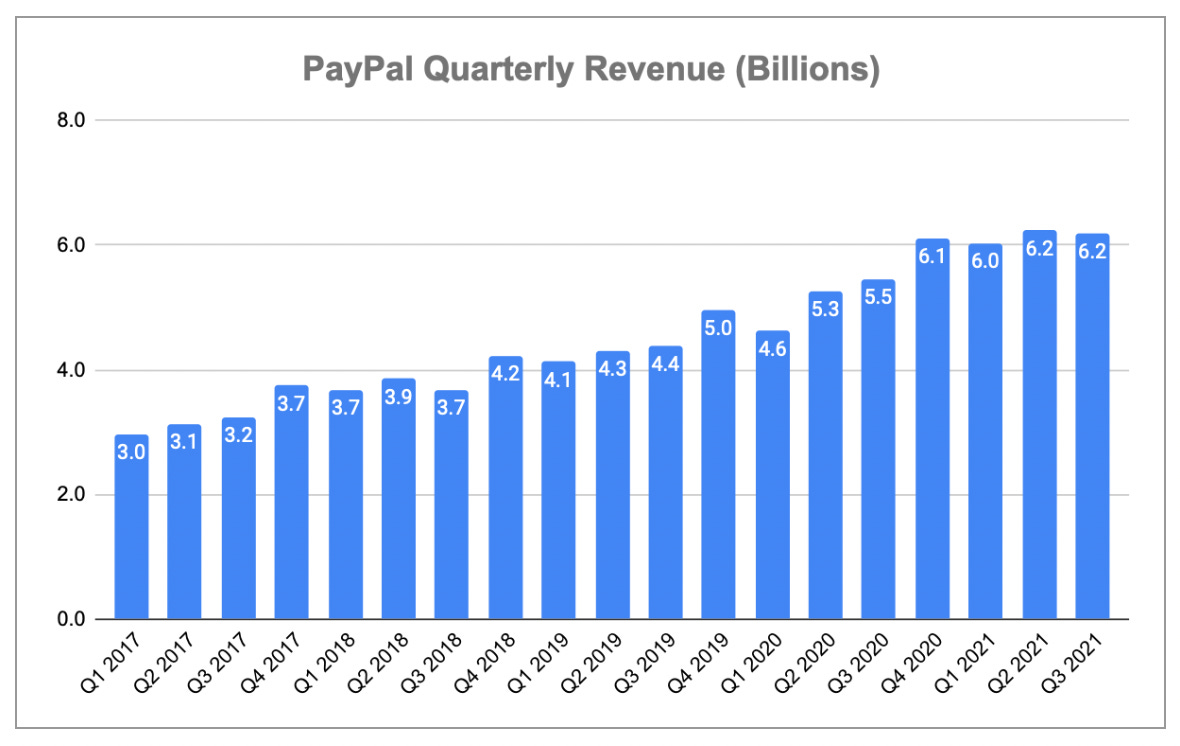

PayPal has been growing revenue at a steady rate over the past number of years. During its most recent financial results for Q3 2021 PayPal recorded revenue of $6.2 billion, an increase of 13% YoY. PayPal’s revenue growth has all the hallmarks of a long term compounder. In less than four and a half years PayPay has managed to double revenue from $3.1 billion in early 2017.

Whilst doubling revenue during this period, PayPal has also been able to maintain it’s impressive operating margin of 17% at Q3 2021.

PayPal is an extremely profitable business. From revenue of $6.2 billion, PayPal produced over $1 billion in operating income in Q3 2021.

PayPal is expected to grow revenue and earnings by 18% and 12% respectively in 2022 (Source: Zachs).

5. Balance Sheet and Cash Flow

Commentary

Over $7.7 billion in cash and cash equivalents

Total Liabilities as percent of Total Assets is 70%

Current Assets to Current Liabilities ratio of 1.30

Goodwill balance making up almost 13% of total assets. This balance is a result of a number of acquisitions including Honey for $4 billion and iZettle for $2.2 billion

Low level of debt amounting to $7.9 billion making up 11% of total assets

During Q3 2021, cash flow from operating activities amounted to $1.51 billion, an increase of 15% YoY. For the same period PayPal recorded free cash flow of $1.29 billion which grew 20% YoY. PayPal is a cash generating machine.

6. Stock Price History

After the second IPO in 2015 PayPal compounded at a steady rate before exploding in 2020 during the Covid-19 pandemic. The stock hit an all time high in July 2021 before experiencing a 40% drawdown over the last couple of months. During this time negative sentiment included the rumoured interest in acquiring Pinterest (Source: Reuters).

7. Competitors

The global payments industry is highly competitive, continuously changing and increasingly subject to regulatory scrutiny and oversight. PayPal competes against a wide range of businesses.

Merchant Competitors

Adyen growing payments company with global operations headquartered in the Netherlands

Stripe provides a payment gateway to application developers and competes with developer tools offered by Square

Shopify, Big Commerce, Wix are direct competitors when it comes to e-commerce building

Consumer Competitors

Square’s Cash App stands as a direct and the most serious competitor to Venmo particularly in the U.S. At the end of 2020, Venmo has 52 million users while Cash App has 36 million but is growing faster.

The competition between Venmo and Cash App is a really fascinating one. If you are interested in reading a bit more into it, I recommend the Venmo vs Cash App paper by Maximillian Friedrich from Ark Invest.

Other consumer competitors

Google Pay and Apple Pay allows consumers to make fast and easy purchases in stores and online

Skrill which is a Paysafe company, provides a digital wallet, Payment gateway, and prepaid card among others

Revolut and N26 which are more commonly used here in Europe

8. Management and Ownership

PayPal was originally established by Peter Thiel, Luke Nosek and Max Levchin, in December 1998 as Confinity. In March 2000, Confinity merged with x.com, an online financial services company founded in March 1999 by Elon Musk. The company was renamed PayPal in 2001. After eBay acquired PayPal in 2002, the original PayPal employees had difficulty adjusting to eBay's more traditional corporate culture and within four years all but 12 of the first 50 employees had left. In the years that followed, this group remained close and became so prolific that the term PayPal Mafia was coined. Companies that the original employees have since founded include Tesla, YouTube, LinkedIn, Afirm, Yelp and Palantir.

Dan Schulman is the current CEO and President having joined in 2014. Prior to joining PayPal, Schulman served as Group President at American Express. Prior to joining American Express, Schulman was President of the Prepaid Group at Sprint Nextel Corporation following its acquisition of Virgin Mobile USA, where he led the company as its founding CEO for eight years. Earlier in his career, Schulman was President and CEO of Priceline Group, where he led the company through a period of rapid growth and expansion. He also spent 18 years at AT&T, where he held a series of positions, including President of the Consumer Markets Division.

Dan Schulman appears to be well received at PayPal with an 92% approval rating on Glassdoor with the company overall scoring 4.0 out of 5 by its own employees.

Given the legacy that PayPal has built over the past 20+ years it is not surprising that the company is no longer founder led. Nonetheless, Dan Schulman appears to be doing a good job.

9. Risks

1. Global Competition

As discussed in Section 8, the global payments industry is highly competitive and highly innovative. Many areas in which PayPal operates evolve rapidly with innovative and disruptive technologies, shifting user preferences and needs, price sensitivity of merchants and consumers, and frequent introductions of new products and services. Competition will further intensify as new competitors emerge, businesses consolidate and established companies in other segments expand to become competitive with various aspects of PayPal’s business model.

The emerging blockchain represents one such disruptive technology. We have seen the race to zero when it comes to trading fees with more and more brokerages offering zero fees. Legacy brokers have had to adapt to this model and are now playing catch up. I think the probability is high that something like this happens with payments. In this scenario, the monetisation would have to come from other value added solutions.

PayPal often partners with many businesses and the ability to continue establishing these partnerships is important to the business. Competition for relationships with these partners is intense, and there can be no guarantee that PayPl will be able to continue to establish, grow, or maintain these partner relationships.

2. Cyberattacks

Cybercrime is on the rise globally and by 2020 is expected to cost the world $10.5 trillion annually (Source: Cybersecurity Ventures). As one of the largest payment processors in the world, PayPal has become one of the most heavily targeted brands for phishing attacks. PayPal scams come in many different forms and typically include phishing emails, spoofed websites, suspicious links, and malicious posts on social media. They are designed to look like official correspondence from the company and the aim is to trick as many users as possible into disclosing sensitive information. Examples include:

Phishing emails - a problem with your account

Phishing website

Social media PayPal scams

You’re a prize winner

Under payment card network rules and contracts with payment processors, if there is a breach of payment card information that PayPal stores, or that is stored by their direct payment card processing vendors, PayPal could be liable to the payment card issuing banks for their cost of issuing new cards and related expenses. Cybersecurity breaches and security vulnerabilities could subject PayPal to significant costs and liabilities, lead to loss of customer confidence and damage of reputation and brands.

10. Opportunities

1. War on cash

Growing numbers of consumers explored different payment mechanisms as an alternative to cash, credit and debit cards in 2020-21 due to a fear of touching cash. That added to a surge in mobile commerce activity, which saw consumers buy more goods and services online using their smartphones as physical stores were closed. Mobile commerce will represent 72.9% of total retail e-commerce sales worldwide in 2021, compared to 70.4% in 2020 (Source: Statistica).

Digital wallets are making the idea of carrying around a physical wallet almost novel. A digital wallet refers to a software, electronic device, or online service that allows individuals or businesses to make electronic transactions. Total spend through digital wallets will exceed $10 trillion in 2025, up from $5.5 trillion in 2020 (Source: Juniper Research).

It’s widely expected that higher volumes of lower-cost smartphones in emerging economies that feature integrated mobile payment technologies like near field communications will make a significant contribution to that e-wallet expansion. The study from Juniper predicts that over 34% of handsets will use contactless payments by 2025, compared to 11% in 2020.

2. Super App

In 2020 PayPal laid out its vision for the future of its digital wallet platform and its PayPal and Venmo apps. This plan involved a shift in product direction that would make PayPal a U.S.-based version of something like China’s WeChat or Alipay or India’s Paytm. Like those apps, PayPal aims to offer a host of consumer services under one roof, beyond just mobile payments. The number of consumers using digital wallets is expected to double to 4.4 billion globally by 2025, and nearly half of consumers already cite simplicity as the top reason to use a digital wallet (Source: Juniper Research).

In September 2021, the first version of that app was officially introduced, offering customers a single place to manage their bill payments, get paid up to two days earlier with the new Direct Deposit feature provided through one of our bank partners, earn rewards and manage gift cards, send and receive money to friends, family and businesses, pay with QR codes for purchases and redeem rewards in-store, access and manage credit, Buy Now, Pay Later services, buy, hold and sell crypto, as well as support causes and charities they care about.

The new app includes a personalized dashboard of a customer's PayPal account, a wallet tab to manage payment instruments and Direct Deposit, a nance tab that includes access to high yield savings and crypto capabilities, and a payments hub that includes send and receive money features, international remittances, charitable and non- prot giving, bill pay, and a two-way messaging feature to send notes of acknowledgment after peer-to-peer.

11. Valuation Multiples

Below are some of the key valuation metrics that I have identified for PayPal.

When PayPal hit an all-time high of $310 in July 2021, the P/S ratio hit 16. Today, PayPal trades at a P/S of just 8.

But, how does this valuation compare to competitors?

The first thing to note is that Square’s Price/Sales ratio is artificially low due to the accounting treatment of Bitcoin revenue. Based on the PE ratio PayPal is very attractively valued relative to its competitors. I would argue that PayPal is fairly valued if not a little undervalued. This is underlined by the fact that both the P/S and PE valuation multiples are at the lowest levels since the pandemic in March 2020.

12. Investment Strategy

PayPal is a proven high-quality compounder. It also benefits from strong tailwinds with the switch to a digital economy presenting a long runway for growth. On the flip side, the risk of disruption is a significant risk. New and emerging technologies are going to change the way we transact and I do believe that it will turn into a race to zero fees. This does not mean that companies like PayPal will not be required, it simply means monetisation coming from other areas of the value chain.

PayPal has proven that it is capable of innovating. You don’t last over twenty-three years in a highly competitive industry without being able to innovate. As a recent example, PayPal decided to build their own BNPL solution whereas Square spent $29 billion on the acquisition of AfterPay.

When it comes to investing, the price you pay ultimately determines the return that you will achieve. At the current valuation PayPal is very attractively valued. My opinion is that the risk of disruption has been priced in.

Disclosure: The author holds a long position in PayPal.

Twitter: @wolfofharcourt

Email: wolfofharcourtstreet@gmail.com

Hit the subscribe button below if you have not already done so in order to receive the latest content straight to your inbox each week.

All previous posts are viewable on the website.

If you enjoy what you see, please give it a like, comment below and share.

Happy investing

Wolf of Harcourt Street

Disclaimer: I am not a financial adviser and I am not here to give specific financial advice. The opinions expressed are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product. The information is based on personal opinion and experience, it should not be considered professional financial investment advice. There is no substitute for doing your own due diligence and building your own conviction when it comes to investing.

Thanks for sharing!