Q4 2023 Earnings Preview

Stocks covered: AMZN, MSFT, META, PYPL, MELI, SE, ABNB, ADYEN, DDOG, EVO

Welcome to the Q4 2023 earnings preview where I delve into the market expectations and highlight Key Performance Indicators (KPIs) that I believe are most important to the companies that I follow closely.

Revenue Snapshot

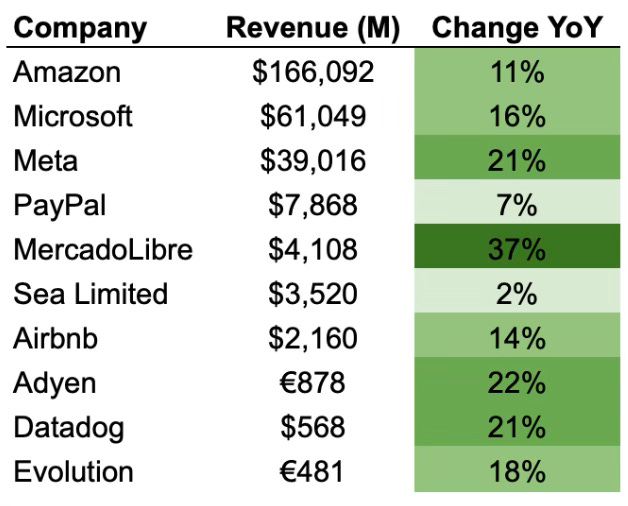

In the table below, I have compiled a snapshot of the revenue consensus estimates for 10 stocks that I am most interested in this earnings season. The stock market is a forward-looking mechanism, and these estimates represent what the market has priced in today. Generally speaking, any deviations from these expectations will cause fluctuations in the stock prices.

The consensus estimates have been obtained from Koyfin, the tool I use to screen and analyze stocks. In my opinion, it is the most comprehensive financial data and visualization tool that makes the research process much easier for investors. If you would like to try it for yourself, you can click here to sign up and receive a 10% discount.

What stands out to me initially is the strong double digit revenue growth that the Big Tech names, namely Amazon, Microsoft, and Meta, are expected to achieve. MercadoLibre is also anticipated to have another stellar quarter, with quarterly revenue expected to exceed $4 billion for the first time. The revenue number quoted for Adyen relates to H2 rather than Q4, as Adyen reports half-yearly results. Sea Limited has very low expectations among analysts, with revenue growth of just 2% expected.

Amazon

KPI: AWS Revenue Growth.

The growth in Amazon Web Services (AWS) revenue is a vital KPI for assessing Amazon, as it contributes over 70% to the company's total profits. The consistent 12% growth over the past two quarters underscores AWS's stability and its pivotal role in Amazon's financial performance. This sustained growth is indicative of AWS's market strength and its influence on Amazon's broader success, making it a key metric for investors assessing the company's long-term prospects.

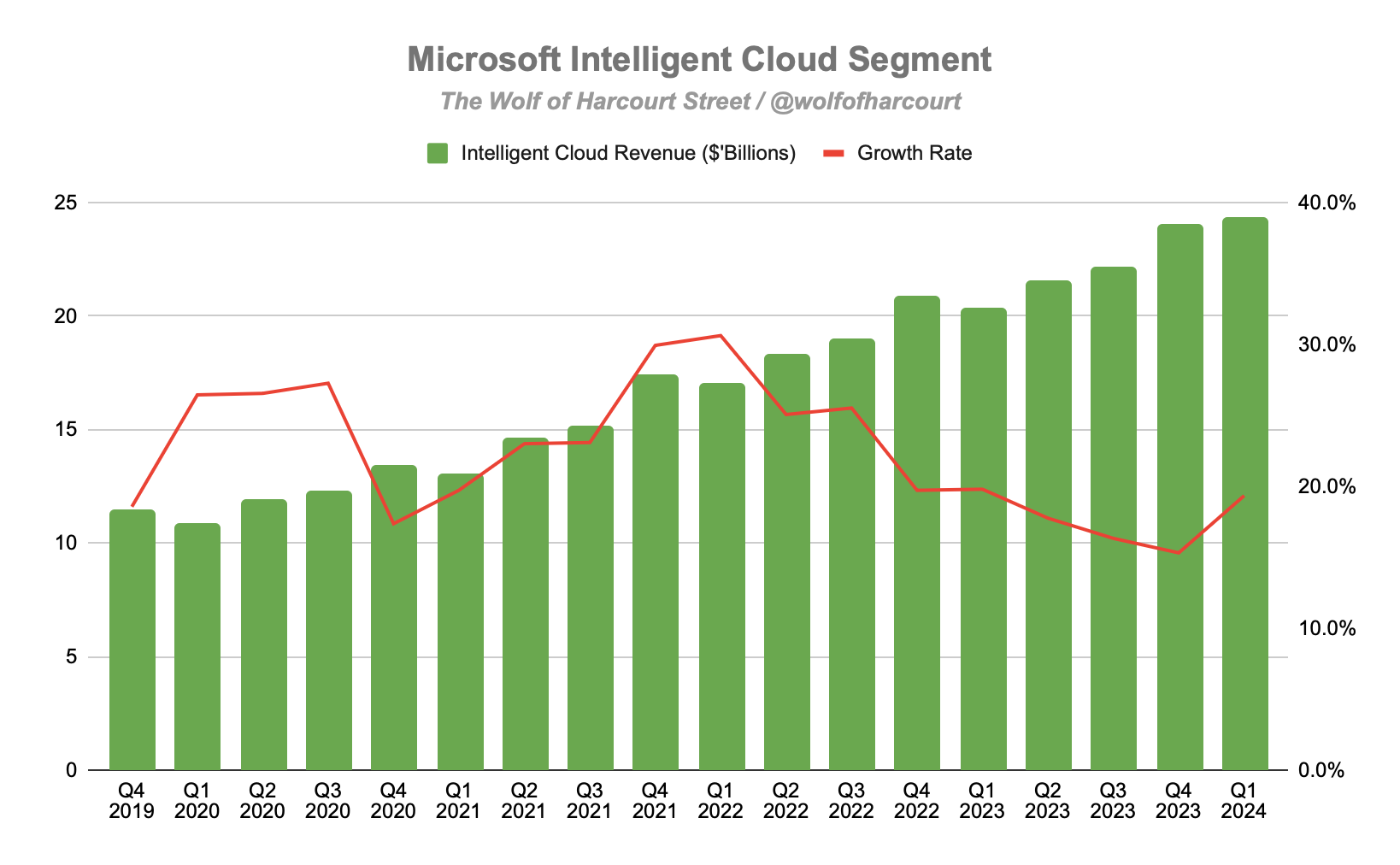

Microsoft

KPI: Intelligent Cloud Revenue Growth.

Microsoft's performance in the rapidly growing cloud computing market is best assessed through its Intelligent Cloud segment revenue, making it an important KPI. In Q1 2024, the Intelligent Cloud segment experienced accelerated growth at 19%, the fastest since Q1 2023. This metric demonstrates Microsoft's strength in cloud services, particularly with Azure, showcasing the company's ability to meet increasing demand for cloud solutions. As organizations increasingly rely on cloud-based technologies, the growth in Intelligent Cloud revenue signifies Microsoft's competitive position and its ongoing success in capturing market share in this critical sector.

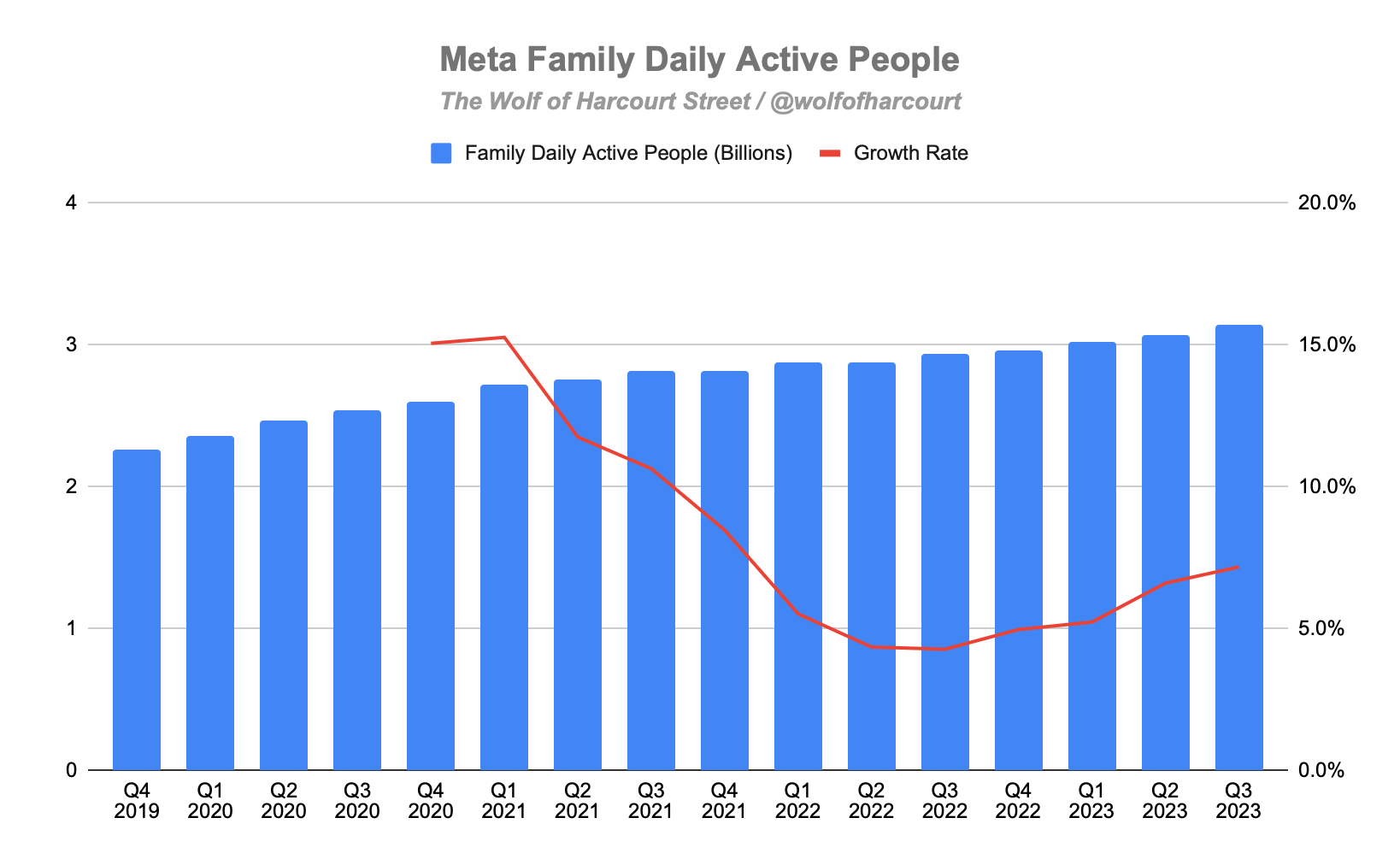

Meta

KPI: Family daily active people (FDAP).

FDAP stands out as the most important KPI for analyzing Meta as it tracks the engagement of users within the broader family of apps including Facebook, Instagram, Messenger and WhatsApp. In Q3 2023, FDAP grew by 7%, marking its fastest increase since Q4 2021. This metric is significant because a higher number of Daily Active Users directly correlates with increased Ad impressions, subsequently driving revenue and profit for Meta.

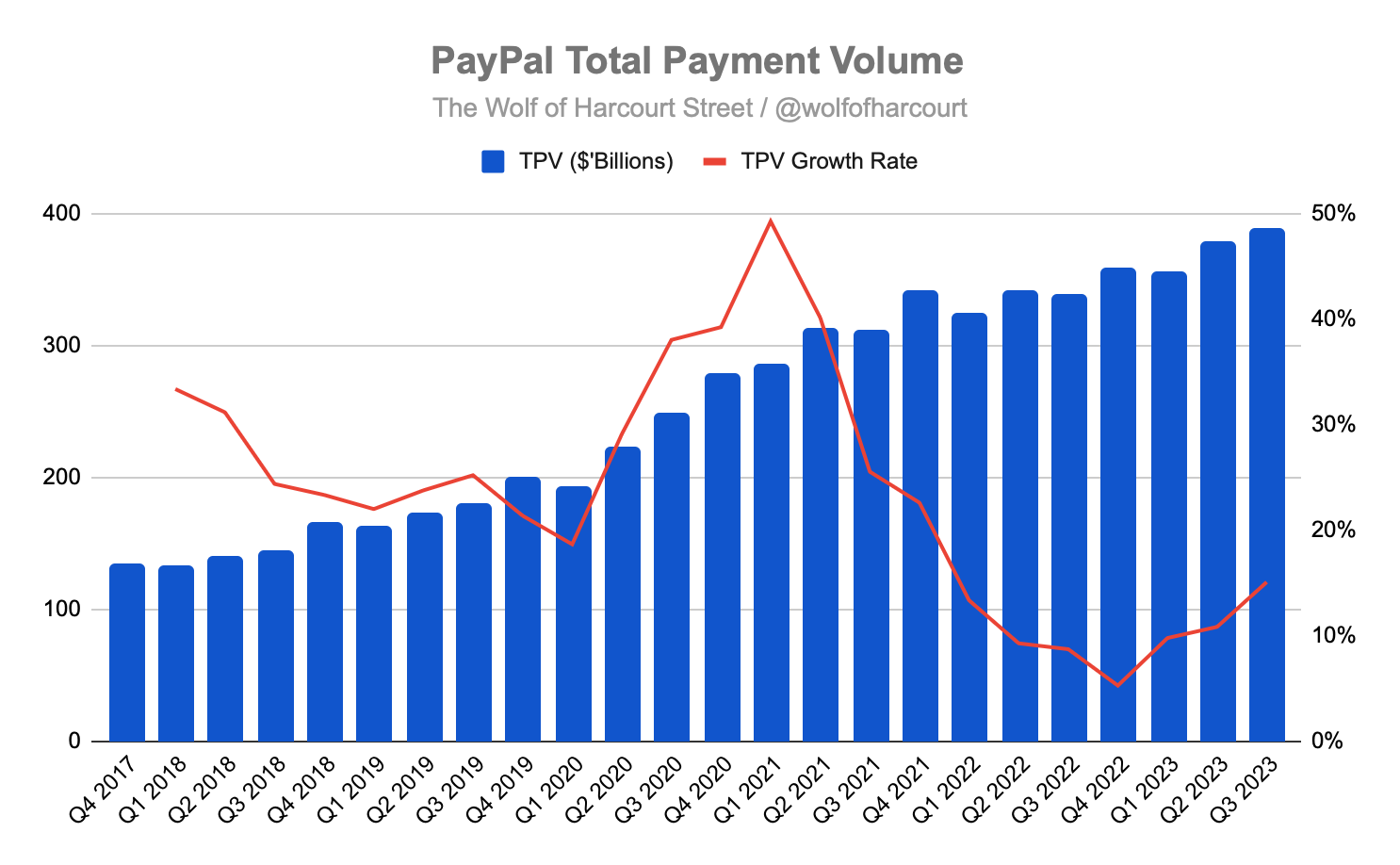

PayPal

KPI: Total Payment Volume (TPV).

TPV serves as a key metric for assessing PayPal, offering insights into the company's transactional activity and overall financial well-being. The accelerated growth from 5% in Q4 2022 to an impressive 15% in Q3 2023 indicates an uptick in user engagement and payment processing. This surge in TPV suggests a positive outlook for PayPal's revenue streams, making it a pivotal metric for investors evaluating the company's performance.

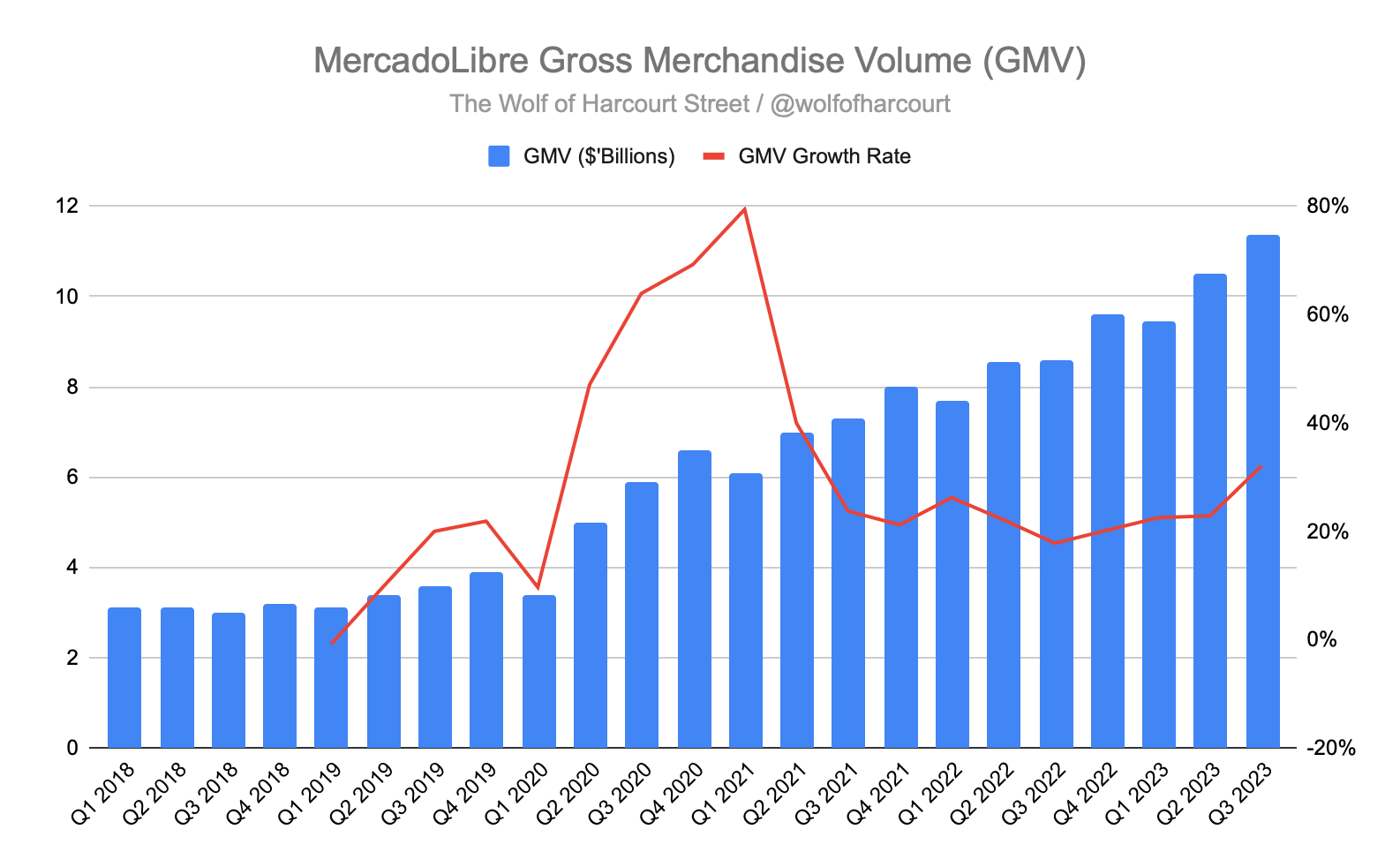

MercadoLibre

KPI: Gross Merchandise Volume (GMV).

GMV plays a crucial role in evaluating MercadoLibre as it measures the total value of goods sold on the platform. The accelerated growth of GMV, from 18% in Q3 2022 to an impressive 32% in Q3 2023, signifies the platform's increasing transaction volume and market influence. This surge not only reflects a growing user base but also underscores MercadoLibre's ability to facilitate more substantial transactions, making it a key metric for investors evaluating the company's overall performance and market expansion.

Sea Limited

KPI: Digital Entertainment Quarterly Paying Users (QPUs).

QPUs directly reflect the Digital Entertainment platform's revenue-generating user base. In Q3 2023, QPUs experienced a decline from 43.1 million to 40.5 million, though it remained above the Q1 2023 low. Despite this setback, there is anticipation that the strong performance of Free Fire, prominently featured in worldwide download charts, will positively impact Q4 performance. Note that metrics associated with Shopee and e-commerce are no longer disclosed quarterly, which is why I have opted for this metric.

Airbnb

KPI: Nights and Experiences Booked.

Nights and Experiences Booked serves as a KPI for Airbnb, acting as a robust predictor of future demand. In Q3 2023, the growth rate increased to 14%, up from 11% in Q2 2023, underscoring the platform's increasing popularity and indicating a positive trajectory for the company's performance in the coming quarters.

Adyen

KPI: Processed Volume.

Processed Volume is the most important KPI for analyzing Adyen, as it reflects the company's transactional activity and overall payment processing health. In H1 2023, Adyen experienced a 23% growth in Processed Volume, marking the slowest expansion since H1 2020. Over 80% of the growth came from the expansion of existing customer relationships on the platform.

Datadog

KPI: $100K+ Annualised Revenue Run-rate (ARR) Customers.

For Datadog, the KPI in question is the number of customers with an Annualized Revenue Run-rate (ARR) exceeding $100,000. This subset, constituting around 10% of the total customer base, holds significant weight as it contributes approximately 85% to the company's ARR. In Q3 2023, Datadog added 140 new customers in this category, marking the highest quarterly increase since Q4 2022.

Evolution

KPI: Employee Utilisation.

Employee Utilisation is the KPI to focus on when analysing Evolution due to its direct impact on unit economics. In Evolution's operational model, leveraging live dealer salaries as a fixed cost across a substantial player base enhances the scalability and attractiveness of unit economics. Based on the Q3 2023 annualised numbers, Evolution's revenue per average FTE of €140k is five times higher than the cost per FTE of €28k.

If you'd like to support the work of an independent analyst, you can buy me a coffee. The proceeds will contribute to covering the annual running costs of the newsletter.

Join the community of informed investors – subscribe now to receive the latest content straight to your inbox each week and never miss out on valuable investment insights.

If you found today's edition helpful, please consider sharing it with your friends and colleagues on social media or via email. Your support helps to continue to provide this newsletter for FREE!

Happy investing

Wolf of Harcourt Street

Contact me

Twitter: @wolfofharcourt

Email: wolfofharcourtstreet@gmail.com

Good framework