Sea: Another step on the profitability pathway

Sea Limited Q1 2023 Earnings Analysis

Welcome to the hundreds of new subscribers who have joined since the popular Cloudflare, Inc. Research Report.

Executive Summary

Digital Entertainment quarterly active users decreased by 20% YoY, and the quarterly paying user ratio declined from 10.0% to 7.7% YoY. As a result, quarterly paying users fell by 39% to 37.9 million. Both the total user base and paid user base continue to shrink resulting in segment revenue declining 53% YoY.

E-commerce revenue increased 51% YoY driven by higher transaction-based fees and advertising revenue. The resulting increase in take rates has flowed directly to the bottom line resulting in segment gross margin expansion from 22% to 45%.

Digital Financial Services revenue reached $413 million, growing 75% YoY benefiting from expanded use cases, becoming a payment method for Apple services in Southeast Asia. This segment has grown to 14% of group revenue, up from 4% less than two years ago. The credit business continues to thrive with $2 billion in total loans receivable and stable nonperforming loans past due by over 90 days at approximately 2%.

Contents

Financial Highlights

Wall Street Expectations

Digital Entertainment

E-commerce

Digital Financial Services

Financial Analysis

Guidance

Conclusion

1. Key Highlights

Revenue: $3.04 billion +5% year-over-year (YoY)

Digital Entertainment: $540 million -53% YoY

E-commerce: $2.26 billion +51% YoY

Sale of goods: $242 million -9% YoY

Gross Profit: $1.42 billion +21% YoY

Digital Entertainment: $366 million -56% YoY

E-commerce: $1.02 billion +215% YoY

Sale of goods: $32 million +54% YoY

Net Income: $87 million compared to a loss of $580 million YoY

Adjusted EBITDA: $507 million compared to a loss of $510 million YoY

2. Wall Street Expectations

Revenue: $3.06 billion (miss by 1%)

Earnings per Share: 0.53 (miss by 72%)

3. Digital Entertainment

At the end of Q1 2023, quarterly active users (QAUs) reached 491.6 million, a decrease of 20% YoY. The quarterly paying user ratio also decreased from 10.0% to 7.7% YoY. What this ultimately means is that quarterly paying users (QPUs) fell by 39% from 61.6 million a year ago to 37.9 million for the first quarter of 2023. The total user base and paid user base both continue to shrink YoY.

On the face of it, quarterly active users appear to have steadied and increased 1% from Q4 2022. Management revealed that they have been working to optimise various aspects of gameplay and game mechanics based on user feedback, ensuring that players continue to enjoy the highly engaging and highly social experiences they associate with their games. In April 2023, Free Fire experienced a notable increase in monthly active users. This surge resulted in achieving the highest number of active users in the last eight months. April will fall into Q2 so we will have to until then to see if this can boost the number of quarterly paying users.

Another game, Arena of Valor, achieved a new peak in quarterly active users and bookings. Management alluded to a healthy pipeline of upcoming titles, including the open-world survival game Undawn and the mobile title Black Clover Mobile.

QPUs is the single most important metric when looking at Digital Entertainment. Free users don’t pay the bills. QPUs are back to where there were in Q1 2020, three years ago. Can optimisation of gameplay and the launch of new titles convert to paying users?

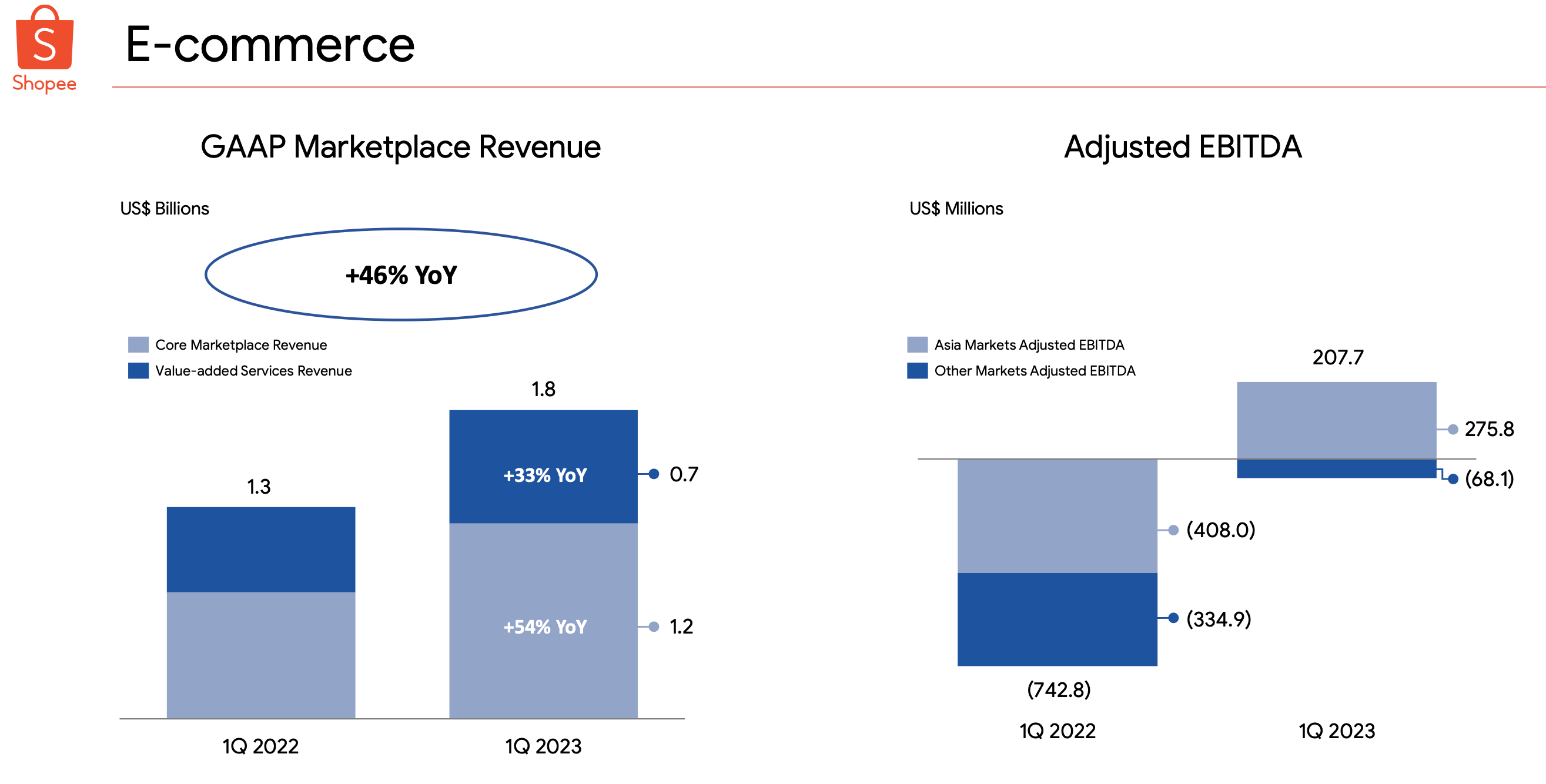

4. E-commerce

Unfortunately, last quarter management revealed that from Q1 2023 onwards they will transaction from quarterly to annual disclosure of Gross Orders and Gross Gross merchandise value (GMV) meaning the analysis here is limited. This is a personal frustration as it limits the depth of my analysis. The focus on revenue is not optimal for investors as this is a lagging indicator.

During Q1 2023, revenue increased by 36% YoY, reaching $2.1 billion, mainly due to deeper monetisation. Core marketplace revenue grew by 54% to $1.2 billion, driven by higher transaction-based fees and advertising revenue. Adjusted EBITDA improved significantly, with a positive value of $208 million, compared to a loss of $743 million in the previous year.

Shopee's positive financial performance was attributed to increased monetization and improved operating cost efficiency. In the Asian market, they achieved an adjusted EBITDA of $276 million, a substantial improvement from a loss of $408 million in the same period last year. Adjusted EBITDA losses in other markets also narrowed considerably, reaching $68 million compared to $335 million previously. Brazil showed a significant improvement in contribution margin loss per order, decreasing by 77% YoY to $0.34, thanks to enhanced monetisation and higher efficiency in sales and marketing expenses.

On the conference call management noted consistent seasonality trends QoQ compared to the previous year in relation to GMV. Indonesia showed strong performance, and Thailand and Malaysia also experienced QoQ growth. Brazil remains a growth market, and despite achieving significant scale and operational efficiency, the company continues to invest in the market to capture long-term opportunities.

Shopee plans to invest further in Brazil to seize the significant opportunities in the market. During the quarter, they focused on enhancing logistics cost leadership and delivery experience, increasing automation in delivery services, and expanding the coverage of their logistics services across markets. They reduced average delivery time by over half a day and achieved 95% buyer coverage for delivery services in Indonesia. In Brazil, they expanded their distribution and sorting centers, opened 50 new hubs, and worked on improving the customer journey, including piloting on spot returns and handling returns directly for better buyer experience.

Shopee continues to diversify its local seller base, strengthen relationships with ecosystem participants, and empower influencers through programs like the Shopee affiliate program. They have reached over 3 million registered local Brazilian sellers, representing 85% of orders in Brazil. The Shopee affiliate program has over 4 million registered influencers across markets, driving significant growth in orders. Shopee also focuses on value creation for brand partners, offering tools to track trends, understand buyer behavior, enhance consumer loyalty, and protect intellectual property rights.

5. Digital Financial Services

SeaMoney's performance in the first quarter of 2023 showed significant growth. Revenue reached $413 million, a 75% increase compared to the previous year. The adjusted EBITDA improved to $99 million, a substantial improvement from a loss of $125 million in the same period of 2022. This growth was attributed to strong top-line growth and efforts to optimize costs, particularly in sales and marketing expenses.

In terms of digital wallet services, Shopee Pay expanded its use cases, such as becoming a payment method for Apple services in Southeast Asia. The credit business also performed well, with a total loans receivable of $2 billion and stable nonperforming loans past due by more than 90 days at around 2%.

The company has diversified its funding sources for the credit business, including channeling arrangements and asset-backed facilities with local and regional banks. They aim to further diversify their funding sources to include broader financial investors.

To strengthen risk management, the company utilizes AI to assess fraud risk, credit risk, and enhance the KYC (Know Your Customer) process. This allows them to offer financial products to more users while maintaining risk control. They have also expanded their product offerings, including insurtech products and services in their banking apps, providing greater convenience and accessibility to users.

Integration of these financial products into their broader ecosystem, connecting Shopee and SeaMoney, ensures a seamless user experience.

6. Financial Analysis

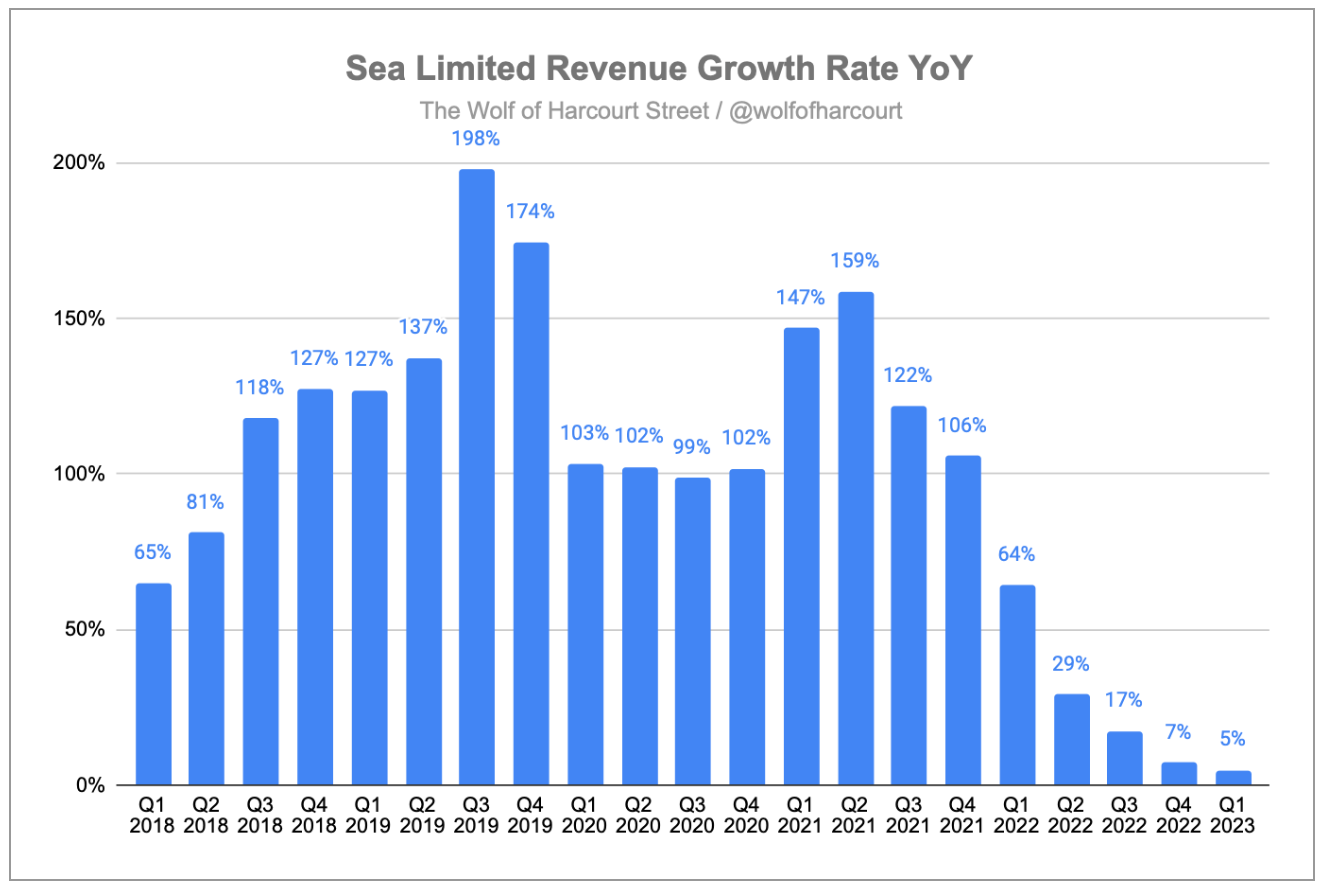

Sea grew its top line by 5% YoY as growth continues to trend downwards. Despite revenue only increasing by 5%, gross profit increased by 21% with gross margin improving from 40% to 47% YoY.

E-commerce continues to contribute the majority of revenue of the business. Digital Entertainment and Sale of Goods both experienced revenue declining during the quarter.

The increase in gross margin from 40% to 47% is a result of the E-commerce gross margin doubling from 22% to 45%. Sale of Goods gross margin increased modestly but Digital Entertainment gross margin declined during the quarter adding further cause for concern in this division.

E-commerce margins improved due to increased marketplace take rate. While we cannot work out the exact take rate in Q1 due to the reduced GMV disclosures this quarter, we know that the implied take rate during Q4 2022 was 10.0% compared to 7.1% at Q4 2021. E-commerce revenue grew 50% in Q4 2022 and grew 51% in Q1 2023 despite the take rate increasing which demonstrates the pricing power Shopee can exert. E-commerce can continue to grow despite the focus on profitability.

Operating expenses decreased by 23% to $1.67 billion during the quarter. The main driver here was sales and marketing expenses, which decreased by 60% to 400 million due to the continued efforts to optimise operating costs and achieving higher cost efficiencies.

Provision for credit losses increased 121% to $177 million driven by expansion to a broader user base and the growth of the loan book.

The primary reason Sea missed the EPS estimate was due to $118 million goodwill impairment associated with a previous acquisition.

The walk from an operating loss of $498 million during Q1 2022 to an operating income of $125 million during Q1 2023 can be summarised as follows:

~$189m gross margin benefit primarily due to higher transaction-based fees and advertising

~$434m operating margin benefit primarily due to continued cost optimisation and efficiencies

Cash Flow Analysis

Sea’s operating cash flow is continuing to improve. At Q1, quarter-to-date (QTD) cash flow from operations improved from -$724 million to +$606 million. This represents an operating cash flow margin of 20% which is really impressive considering the focus on profitability is only two quarters old.

One item of interest in the operating cash flow statement is share based compensation (SBC) which increased 47% YoY to $199 million. This represents considerable growth especially considering revenue only grew 5% but is explained by the shift from cash bonuses to SBC over the past year due to the focus on profitability.

This shift has resulted in share dilution of almost 8% over the past year. This will not be sustainable as it will massively erode shareholder returns.

Sea’s QTD investing cash flow resulted in a deficit of $674 million compared to a deficit of $1.13 billion YoY.

Sea’s QTD financing cash flow resulted in a surplus of almost $59 million compared to a surplus of $142 million YoY.

Without a granular cash flow statement we are unable to determine the free cash flow that Sea generated but it is safe to assume that Sea is now self sufficient based on the operating cash flow with no requirement for external sources of funding.

7. Guidance

Management did not give any future guidance. Wall Street analysts are predicting revenue growth of 8.2% for 2023 and EPS of 3.31 compared to -1.69 in 2022.

8. Conclusion

E-commerce and Digital Financial Services continue to remain extremely resilient. Operating margins for both have improved enormously, swinging negative to positive while revenue continues to grow at above average rates.

Digital Entertainment is a real worry. Management have tried to draw attention to the fact that QAUs have increased 1% QoQ but what really matters is that QPUs continue to fall QoQ which has resulted in revenue and crucially margins declining further. Not so long ago this segment was referred to as a cash cow but while still profitable has turned into the problem child in my eyes. Management have referenced actions to optimise Garena and I expect to see some sort of results next quarter.

A second quarter of profitability in a row is nothing to be sniffed at especially for a company that has been loss making up until last quarter. The company has gone to extraordinary lengths to achieve this including layoffs, banning business class flights, daily meals capped at $30, hotels at $150 per night, snacks disappearing from offices, luxury tea brands replaced with Lipton and two-ply toilet paper gaving way to one-ply (Source: Bloomberg)

Management has demonstrated that it can control costs so far. Now it must prove that it can reaccelerate profitable growth.

Rating: 3 out of 5. Meets expectations.

Disclosure: The author holds a long position in Sea Limited.

Hit subscribe below if you have not already done so in order to receive the latest content straight to your inbox each week.

If you enjoy today’s edition, then feel free to share as it, it really helps.

Happy investing

Wolf of Harcourt Street

Contact me

Twitter: @wolfofharcourt

Email: wolfofharcourtstreet@gmail.com

Momentum Asia did a great webinar (Apples to Apples: Benchmarking Shopee, Grab, GoTo and other major tech platforms webinar) some months ago trying to make sense of tech delivery platform company earnings and metrics which I did a post about… Frankly, would not touch the sector as they are too difficult to evaluate… https://emergingmarketskeptic.substack.com/p/making-sense-of-delivery-platform-stock-metrics