Sea: The Triple Engine Firing on All Cylinders

Sea Limited (SE) Q1 2026 Earnings Analysis

Executive Summary

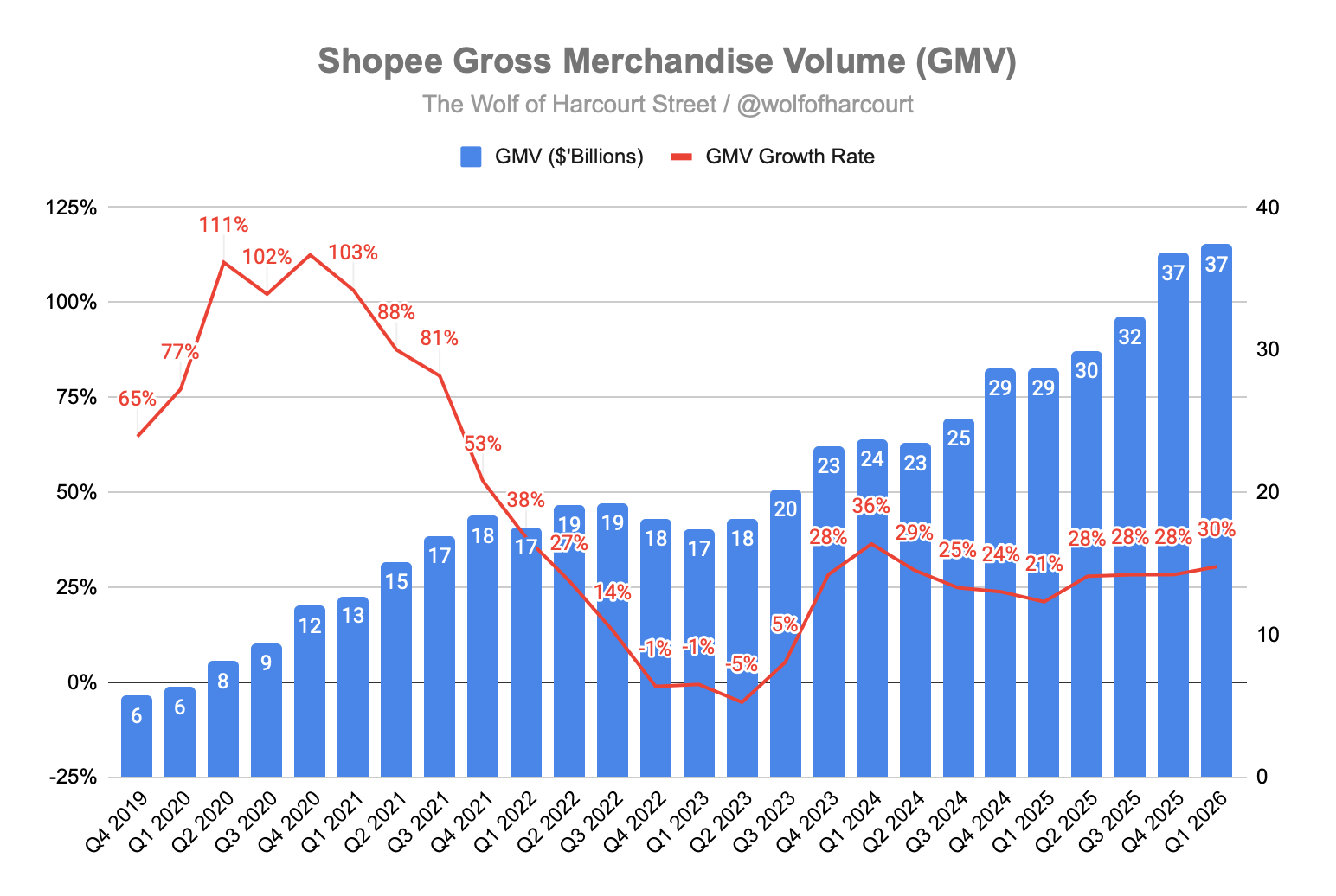

E-commerce delivered another record quarter, with GMV reaching $37.3 billion, up 30% YoY, marking the strongest growth since Q1 2025. Gross orders rose 29% YoY to 4.0 billion, while the implied take rate increased to 12.1%, supported by exceptional advertising momentum. Ad revenue surged 80% YoY in Q4 2025, with the ad take rate expanding by more than 90 basis points. Shopee’s investments in instant delivery, fulfilment capabilities, and the ShopeeVIP membership programme are already improving unit economics. In Indonesia, instant delivery costs fell 20% YoY despite volume growth exceeding 35%. Brazil remained a standout market, delivering the fastest growth across the business while continuing to operate profitably.

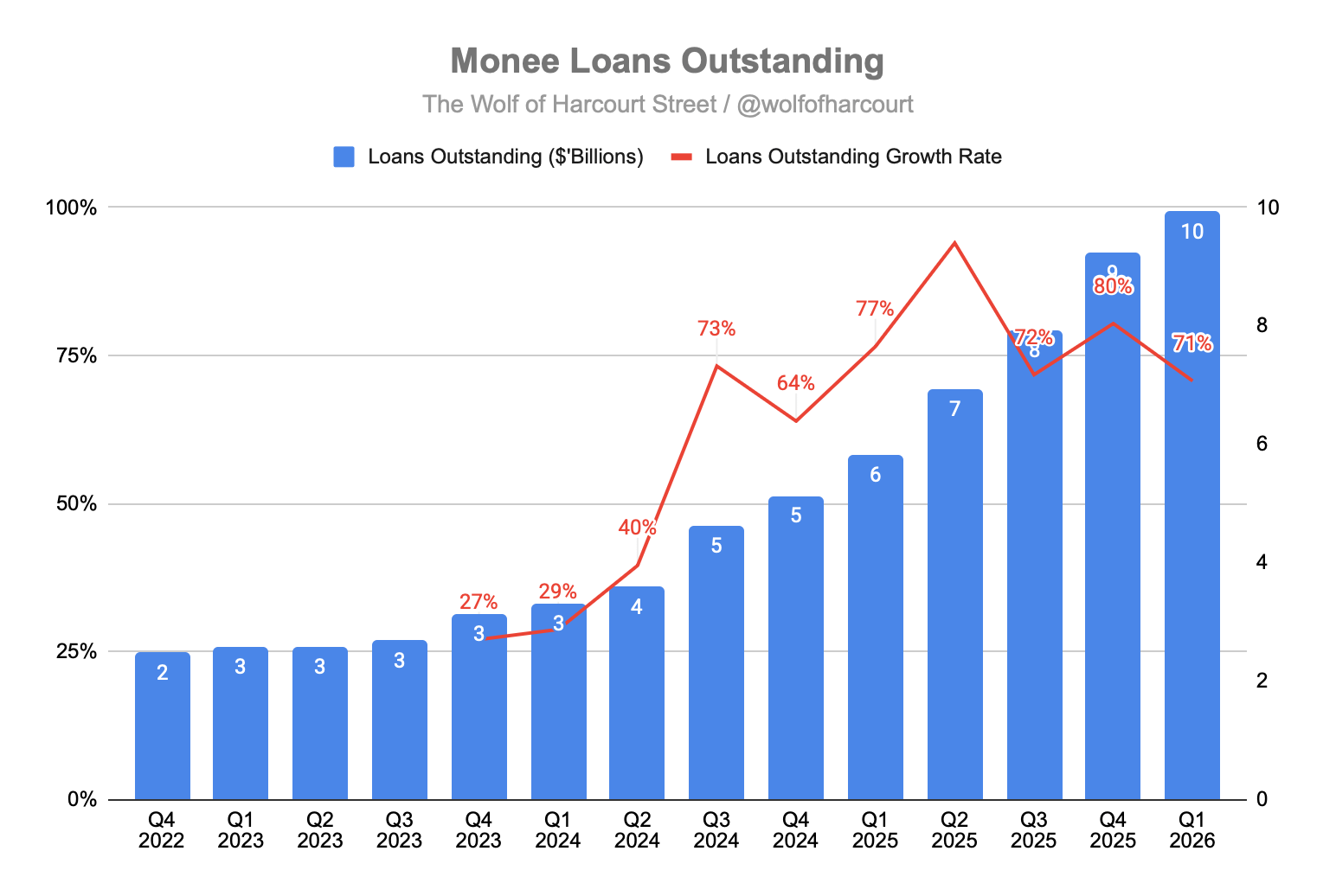

Digital Financial Services maintained its rapid expansion, with the loan book surging 71% YoY to $9.9 billion, including $8.8 billion on-book and $1.1 billion off-book. Growth was driven by the addition of 4.9 million first-time borrowers during the quarter. Active credit users surpassed 38 million, growing more than 35% YoY, while average loan outstanding per user increased 25% to $250. Brazil became the fourth market to exceed $1 billion in loans, growing more than 250% YoY, supported by the recently obtained SCFI licence, which expands Monee’s service capabilities. Importantly, the 90-day NPL ratio remained stable at 1.1%, highlighting strong credit discipline despite aggressive expansion into new user segments and off-Shopee use cases.

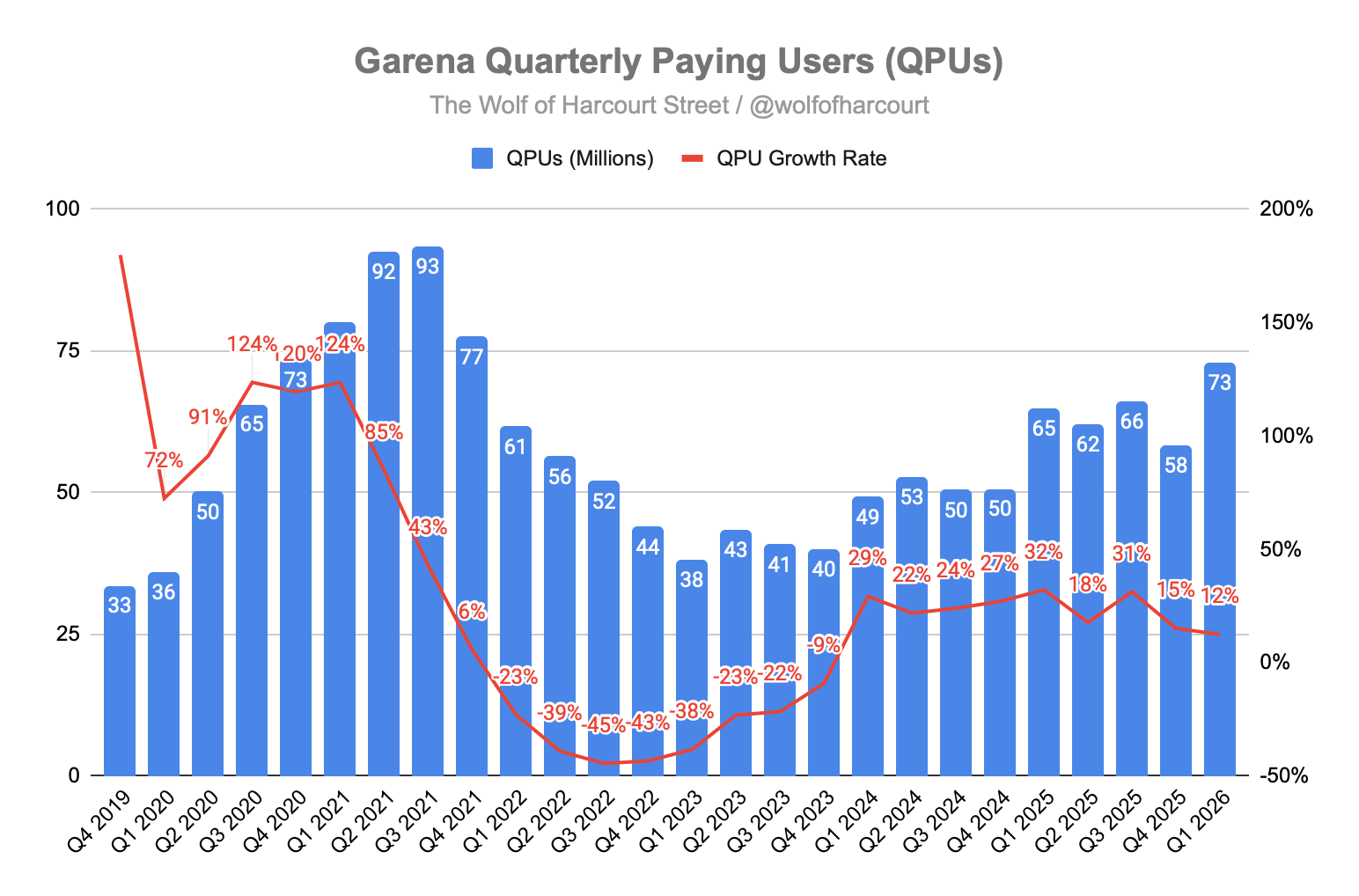

Digital Entertainment delivered its strongest quarter since 2021. Bookings increased 20% YoY to $931 million, while quarterly paying users reached 73 million, up 12% YoY. Free Fire’s collaboration with Jujutsu Kaisen generated more than 700 million content views, becoming one of the most successful IP partnerships in the game’s history. Arena of Valor also achieved record quarterly bookings in its tenth year, reinforcing Garena’s ability to operate games profitably across genres and geographies over long periods. The paying user ratio improved to 10.9% from 9.8% a year ago, while ARPPU increased to $1.40 from $1.17.

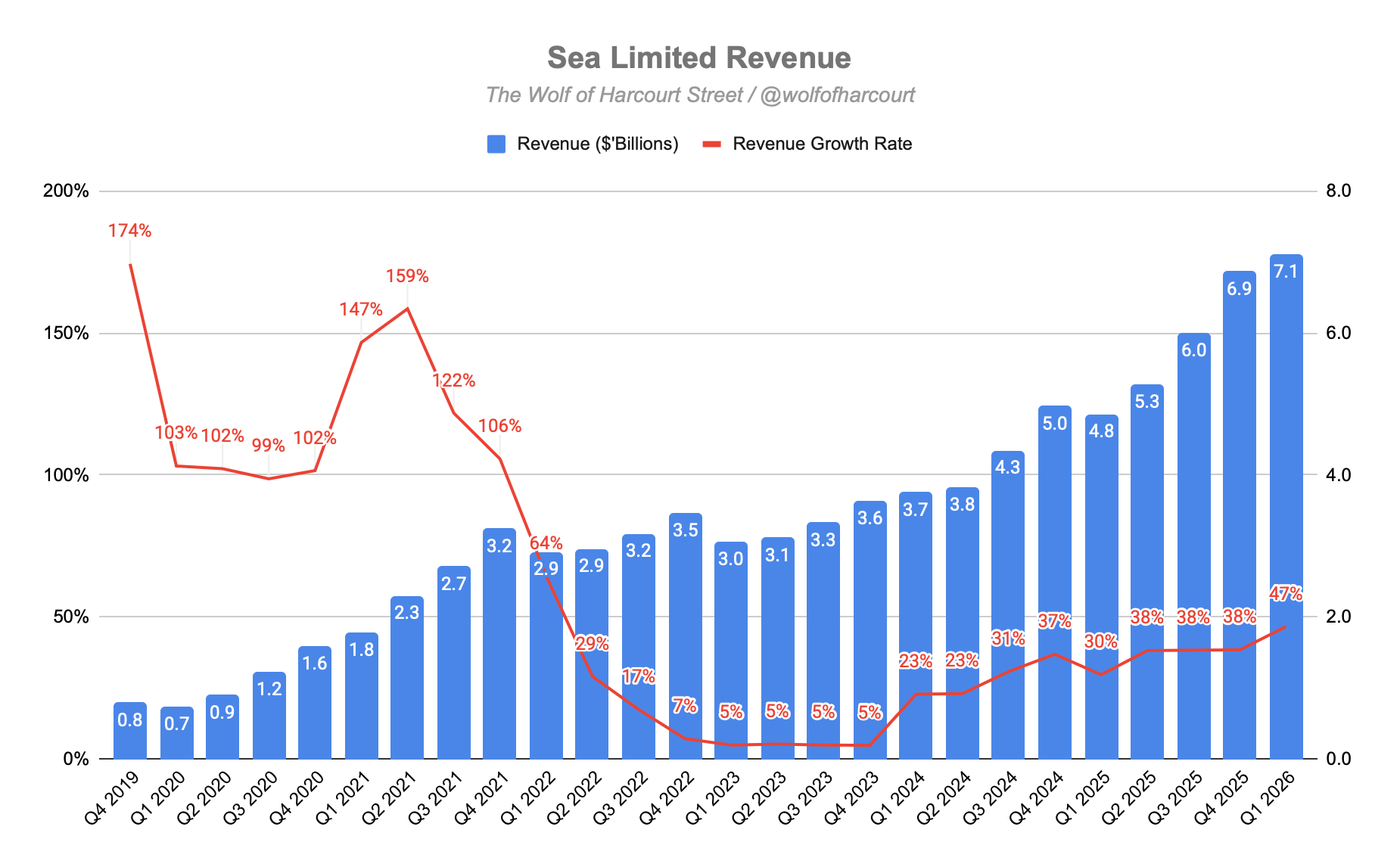

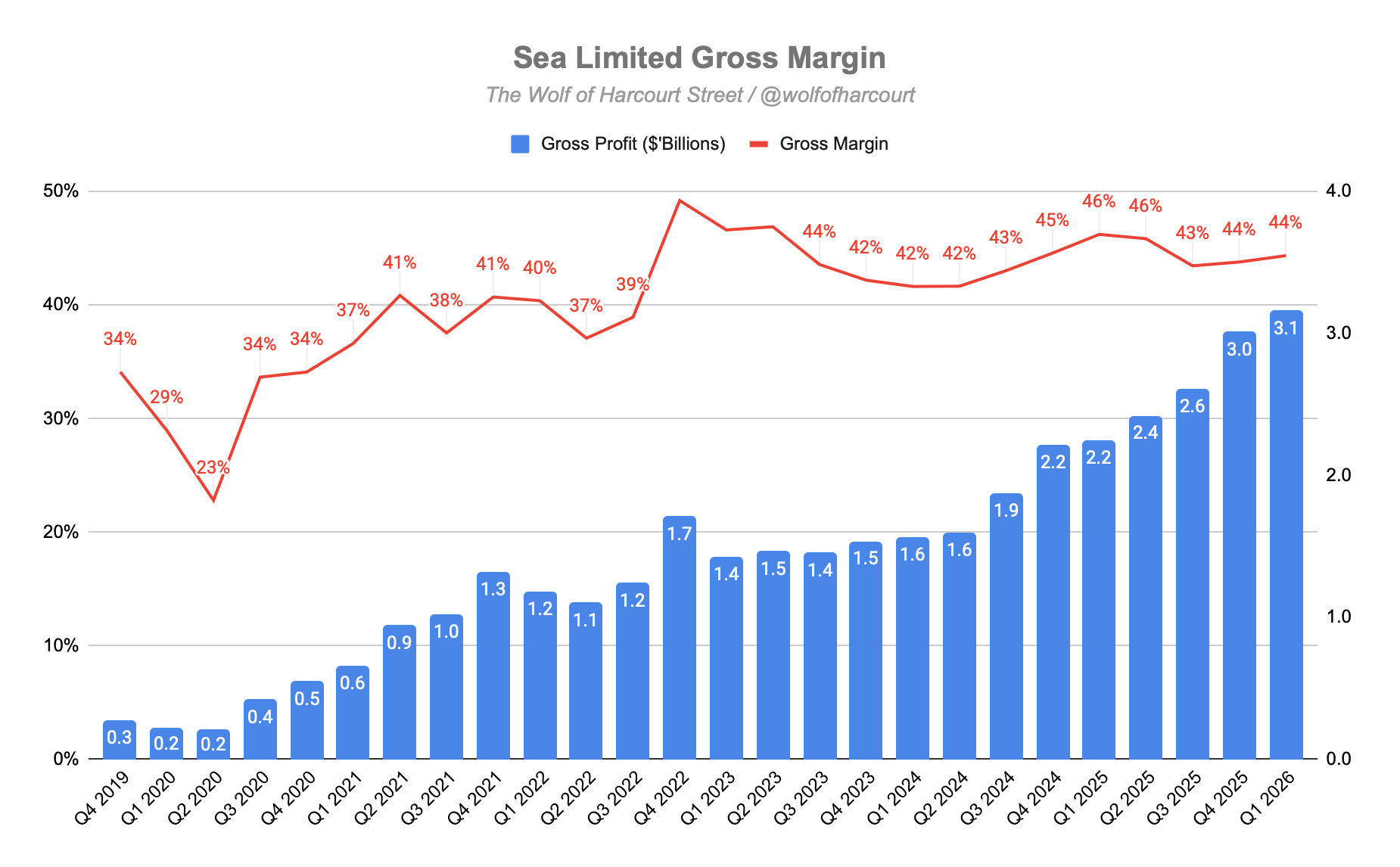

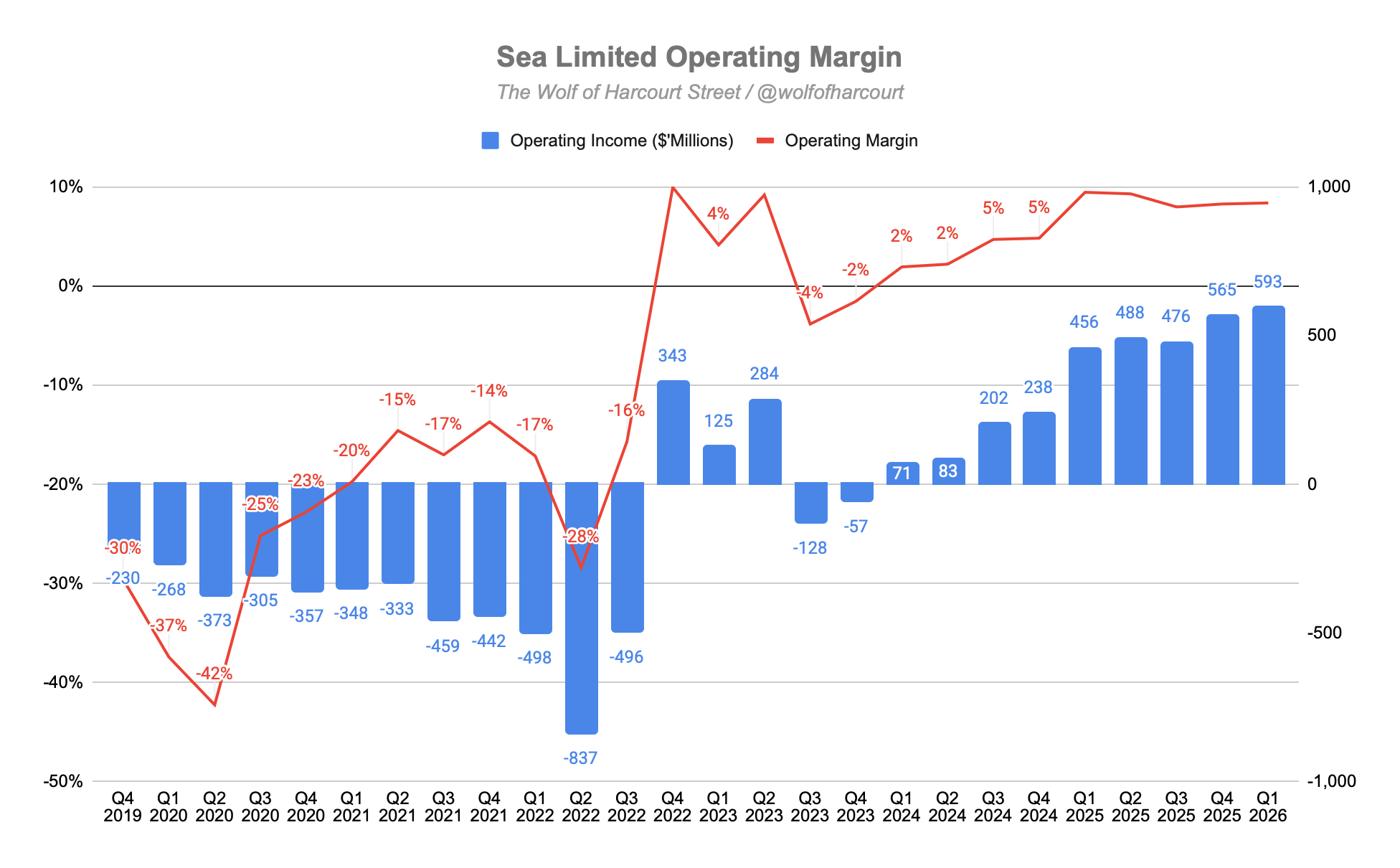

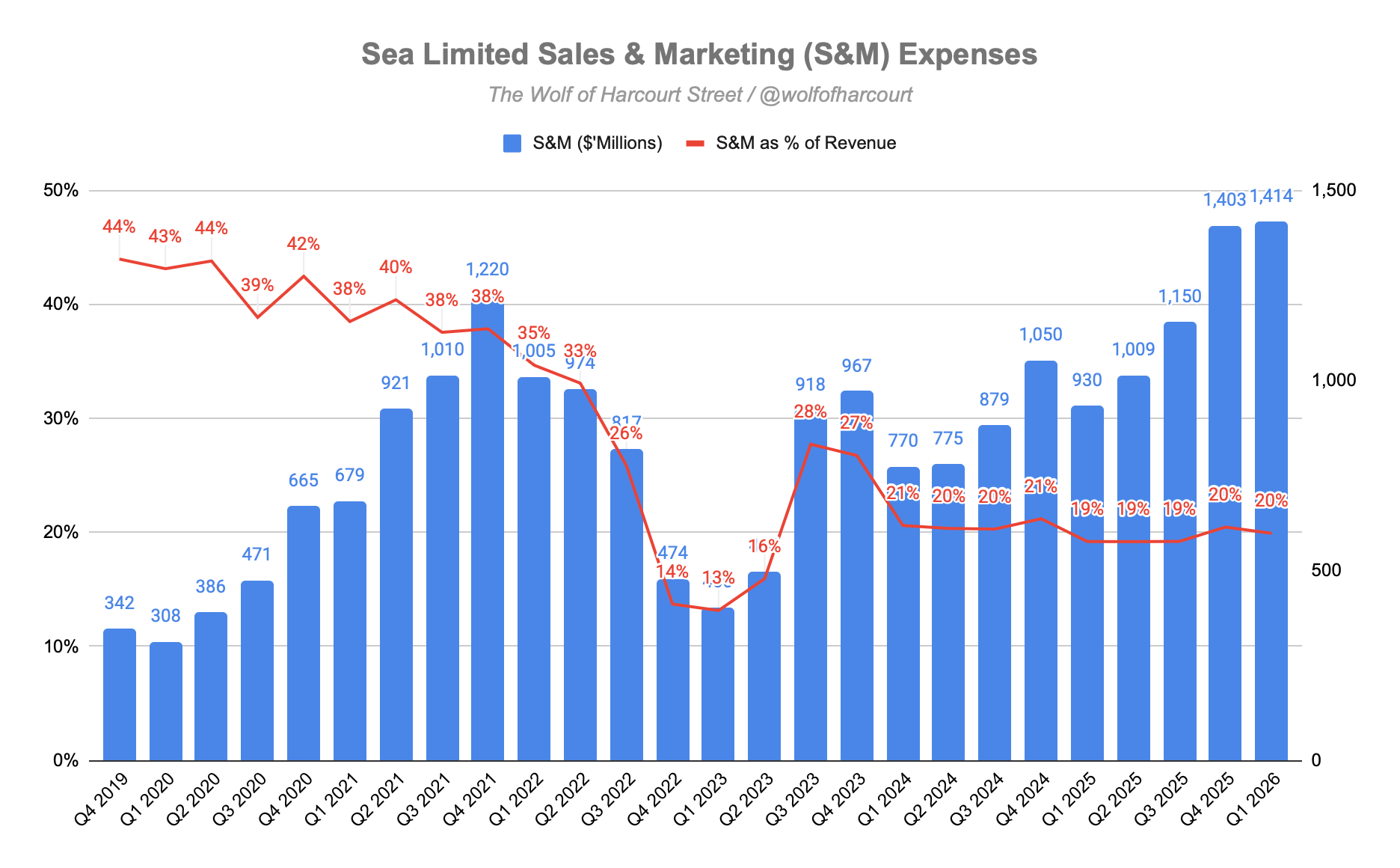

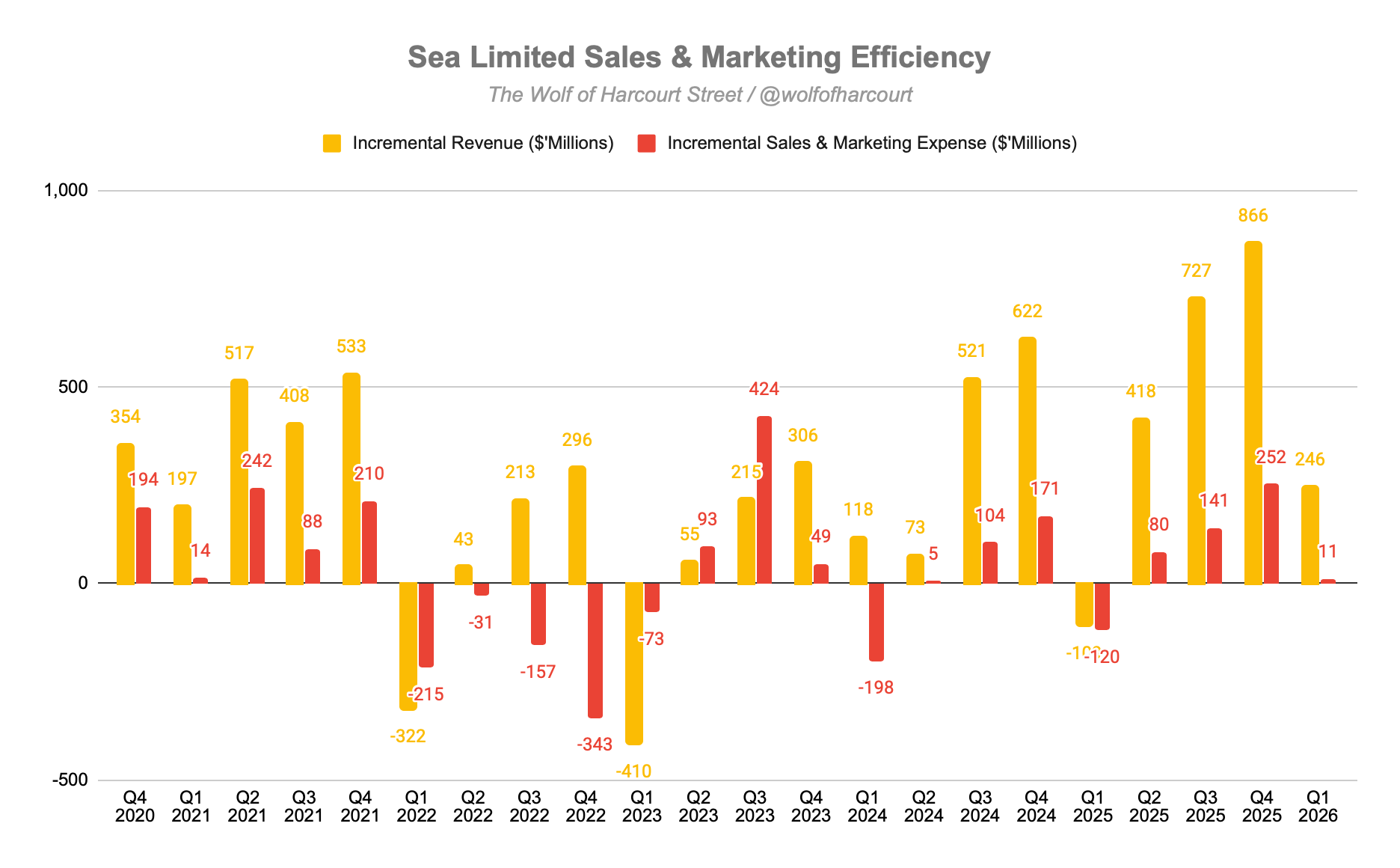

Total revenue accelerated 47% YoY to $7.1 billion, representing the company’s fastest growth rate in four years, since Q1 2022. Gross margin declined to 44% from 46% a year ago as cost of revenue increased 52%. Operating income reached a record $593 million, rising 30% YoY in absolute dollars, although the operating margin declined to 8% from 9% due to continued investment. Operating expenses grew 43%, while Sales and Marketing expenses increased 52% and rose to 20% of revenue from 19% a year ago. Notably, an incremental $11 million in spending generated an additional $246 million in revenue, underscoring improving efficiency and returns on investment.

The company generated adjusted EBITDA of $1.0 billion for the first time, representing 9% YoY growth. Overall, the quarter demonstrated strong absolute profitability growth, even as margins compressed due to deliberate investment. Management continues to prioritise market share gains and strengthening competitive moats over near-term margin optimisation.

Contents

Financial Highlights

Wall Street Expectations

E-Commerce

Digital Financial Services

Digital Entertainment

Financial Analysis

Guidance

Conclusion

Most investors are late to the Mag-7 party.

While these companies continue to get all the attention, Market Sentiment focuses on identifying the second-order effects early.

They were the first to cover the Optics Trade with the basket now up 79%. Their Advanced Packaging Thesis is also now playing out in real time with the portfolio up 75% in three months. They predicted the AI energy bottleneck last year.

Tomorrow, they are launching the Agentic Basket where they cover the second-order winners of the agent buildout.

For the next 24 hours, Wolf of Harcourt Street readers can now unlock full access to Market Sentiment at a special discounted rate.

1. Financial Highlights

Revenue: $7.1 billion (+47% YoY)

E-commerce: $5.1 billion (+45% YoY)

Digital Financial Services: $1.2 billion (+58% YoY)

Digital Entertainment: $697 million (+41% YoY)

Other: $44 million (+33% YoY)

Sale of Goods: $612 million (+51% YoY)

Operating Income: $593 million (+30% YoY)

Net Income: $438 million (+7% YoY)

Adjusted EBITDA: $1.0 billion (+9% YoY)

2. Wall Street Expectations

Revenue: $6.64 billion (beat by 7%)

Earnings per Share: $0.70 (miss by 4%)

3. E-Commerce

Shopee delivered another record-breaking quarter, with GMV reaching $37.3 billion, up 30% YoY, its strongest growth rate in two years. Gross orders exceeded 4.0 billion, up 29% YoY, driven by a 16% increase in monthly active buyers and approximately 12% growth in purchase frequency.

With GMV at $37.3 billion and marketplace revenue of $4.5 billion, the implied take rate reached 12.1%, up from 10.8% in Q1 2025. Achieving take rate expansion alongside rapid GMV and order growth is particularly impressive and highlights Shopee’s strengthening competitive position.

Exceptional Advertising Momentum

Advertising revenue was the primary growth driver, increasing approximately 80% YoY. The ad take rate expanded by more than 90 basis points YoY to roughly 2% of GMV. Both the number of ad-paying sellers and average seller spend increased by around 35% YoY, reflecting the strong ROI sellers are seeing from Shopee’s advertising products.

Importantly, with the ad take rate still only around 2%, there remains meaningful upside. Over the medium term, this could potentially expand toward 4-5% as AI-driven targeting and conversion tools improve further.

Logistics: Deepening the Moat

Shopee’s logistics advantage continues to widen. SPX Express remains one of the region’s largest e-commerce logistics providers, and investments in instant and same-day delivery are paying off.

In Indonesia, instant delivery can now fulfill orders in as little as two hours. Volume grew more than 35% in Q1 while cost-per-order declined approximately 20% YoY. This is a classic example of operating leverage, where higher scale drives lower unit costs.

The company also expanded partnerships with major offline retailers, including convenience chain Indomaret, bringing approximately 7,000 stores onto the instant delivery platform by quarter-end. This helps bridge online and offline commerce, particularly in higher-frequency categories such as groceries and pharmacy products.

Users of instant delivery services continue to demonstrate higher spending and stronger retention, reinforcing Shopee’s ecosystem flywheel.

Fulfillment is emerging as the next major growth lever. Order volumes through Shopee fulfillment centers grew approximately 25% QoQ, improving delivery speed and operational efficiency for sellers.

In Taiwan, Shopee expanded its collection point network to more than 3,100 locations, up nearly 50% YoY. Combined with innovations such as direct-to-locker shipping, which removes the need for additional packaging, buyer waiting times improved 12% YoY. The result was continued double-digit GMV growth in an already mature market.

ShopeeVIP: A Powerful Retention Engine

The subscription-based ShopeeVIP program is becoming an increasingly important driver of engagement and monetization.

Subscribers across Asian markets surpassed 10 million by the end of March, up more than 40% QoQ, while retention rates remained above 80%. ShopeeVIP members consistently show double-digit spending increases after subscribing, reaching as high as 30-40% in some markets.

The program now contributes approximately 20% of GMV across Asia and was launched in Brazil during April, creating another growth lever in Shopee’s fastest-growing market.

Content Ecosystem and Live Streaming

Shopee’s content ecosystem continues to strengthen user engagement.

AI tools are helping sellers create video content without expensive studio setups, lowering barriers to participation. In Southeast Asia, more than 20% of physical goods orders in Q2 originated from live streaming and short-form video content.

Shopee’s partnership with YouTube also remains a meaningful traffic driver, with more than 7 million videos featuring Shopee product links by June, up over 60% QoQ.

Brazil: The Standout Growth Market

Brazil was Shopee’s fastest-growing market in Q1, while also remaining profitable, an increasingly rare combination in global e-commerce.

Active buyers, purchase frequency, and basket size all expanded, supported by broad product assortment, competitive pricing, and improved logistics. Delivery times improved by more than one day YoY, while three additional fulfillment centers increased the total network to five.

These investments enabled Shopee to attract more premium merchants. ShopeeMall GMV more than doubled YoY and now represents approximately 15% of total GMV.

Given Brazil’s still relatively low e-commerce penetration, the long-term growth runway remains substantial.

AI: The Invisible Hand

Shopee’s practical use of AI is already producing measurable benefits.

AI-powered search and recommendation improvements lifted purchase conversion rates by 14% YoY. AI-generated content tools are also helping sellers create more effective listings at lower cost.

On the operational side, approximately 80% of customer queries are now handled by AI chatbots, reducing customer service cost-per-contact by roughly 30% YoY while maintaining strong satisfaction levels.

Looking ahead, Shopee is testing an AI shopping assistant for buyers and a virtual business advisor for sellers, both of which are expected to see broader rollouts over time.

4. Digital Financial Services

Monee delivered a stellar start to 2026, with the credit business continuing to act as the primary growth engine. The loan book reached $9.9 billion at quarter-end, comprising $8.8 billion on-book and $1.1 billion off-book, representing growth of more than 70% YoY.

The company added 4.9 million first-time borrowers during Q1, bringing active credit users to 38 million, up more than 35% YoY. Average loan outstanding per user increased 25% YoY to approximately $250, reflecting deeper engagement as users establish credit histories and qualify for larger borrowing limits.

The Three-Pronged Growth Strategy

Deepening Existing Relationships

As users successfully repay loans, Monee increases their credit limits and extends loan tenures. This creates a natural progression where borrowers gradually move up the credit ladder and borrow more over time.

Acquiring Higher-Quality Users

Monee is increasingly targeting more affluent users with stronger credit profiles. These customers typically demonstrate better repayment behavior and larger borrowing capacity.

Early campaigns focused on competitive pricing, higher limits, and longer tenures are already showing encouraging traction.

Expanding Off-Shopee Use Cases

This remains the largest long-term opportunity.

Off-Shopee SPayLater in Thailand and Indonesia exceeded 20% of the overall SPayLater portfolio by quarter-end. In Indonesia, growth has been particularly strong in higher-value categories such as electronics and two-wheelers, where installment financing plays an important role.

Personal cash loans, targeted toward reliable SPayLater users, nearly doubled YoY. Despite the strong growth, penetration remains relatively low, suggesting meaningful room for expansion.

Brazil: The Fourth Pillar

Brazil became Monee’s fourth market to surpass $1 billion in loan book size, growing more than 250% YoY.

Growth was driven by a localized product combining SPayLater and cash loans, designed specifically around Brazilian consumer credit behavior. This resulted in strong user adoption and higher repeat usage, with average loan outstanding per user more than doubling YoY.

SPayLater penetration on Shopee in Brazil currently sits at roughly 10% of GMV, still well below more mature markets such as Indonesia, where penetration is already in the mid-teens. This highlights the significant growth runway still ahead.

The SCFI license secured during the quarter further expands the range of financial services Monee can offer and strengthens its long-term positioning in the market.

Asset Quality

Despite expanding aggressively into new segments, geographies, and off-platform use cases, the 90-day NPL ratio remained stable at 1.1%, unchanged QoQ.

This consistency highlights the strength of Monee’s underwriting capabilities and disciplined growth strategy. The relatively short duration of most loans allows management to adjust the portfolio quickly, while real-time optimization of credit limits and loan tenures helps preserve asset quality as the business scales.

Management summarized the opportunity well:

“Expansion into more user segments, off-Shopee use cases, and early markets like Brazil are giving us a much larger addressable opportunity across our portfolio.”

Monee increasingly looks positioned to become a major long-term profit driver for Sea.

5. Digital Entertainment

Garena delivered its strongest quarter since 2021, with bookings rising 20% YoY to $931 million. The performance was driven by the continued strength of Free Fire alongside a record contribution from Arena of Valor.

Quarterly active users reached 667 million, roughly flat YoY. More importantly, quarterly paying users increased 12% YoY to 73 million, while the paying user ratio expanded to 10.9%, up from 9.8% a year ago.

This marks nine consecutive quarters of double-digit paying user growth following several years of decline. ARPPU also improved meaningfully, rising to $1.40 from $1.17 YoY, reflecting stronger monetization across the portfolio.

Free Fire: Eight Years and Still Growing

Free Fire continues to defy the normal lifecycle of mobile games, maintaining more than 100 million average daily active users eight years after launch.

A key reason is Garena’s ability to consistently execute high-quality IP collaborations.

In January, Free Fire launched a major collaboration with the anime Jujutsu Kaisen, generating more than 700 million official content views. The event integrated iconic anime mechanics directly into gameplay, including themed environments and character abilities such as Gojo’s “Unlimited Void.”

The collaboration followed the highly successful Naruto Shippuden partnership in 2025 and further demonstrated Garena’s ability to create culturally relevant gaming experiences that resonate globally.

Beyond IP collaborations, Garena continues refining its localization strategy.

A strong example was the Ramadan campaign. Historically limited to Ramadan-observant regions, Garena expanded the concept into a global “Lost Treasure” event in Q1 2026. Players in relevant markets viewed it as a culturally tailored celebration, while global users experienced it as a fresh desert-themed gameplay event.

The campaign generated more than 120 billion social media impressions, up approximately 70% YoY.

Arena of Valor: Longevity at Scale

Arena of Valor achieved record quarterly bookings in its tenth year of operation, a rare feat in gaming.

The continued success of both Free Fire and Arena of Valor highlights Garena’s unique capability to operate gaming franchises profitably across multiple genres, markets, and time horizons through continuous innovation and engagement.

AI: The Next Enabler

Garena sees AI as an important long-term growth enabler across development, engagement, and content creation.

AI tools are already accelerating asset creation and enabling higher-quality content production at scale. AI-driven game agents may also improve retention by supporting solo players.

Longer term, Garena is experimenting with generative content that could allow players to create in-game assets themselves, although scalability and quality control remain key priorities.

6. Financial Analysis

Revenue

Total revenue accelerated 47% YoY to $7.1 billion, the fastest growth rate in four years and the strongest since Q1 2022.

The acceleration is particularly notable given Sea’s scale and reflects strong momentum across all three core businesses.

E-commerce revenue grew 44% to $4.5 billion, driven by GMV growth and improved monetization, particularly advertising.

Digital Financial Services revenue surged 58% to $1.2 billion, fueled by rapid credit expansion.

Digital Entertainment revenue increased 41% to $697 million, supported by improved monetization and stronger user conversion.

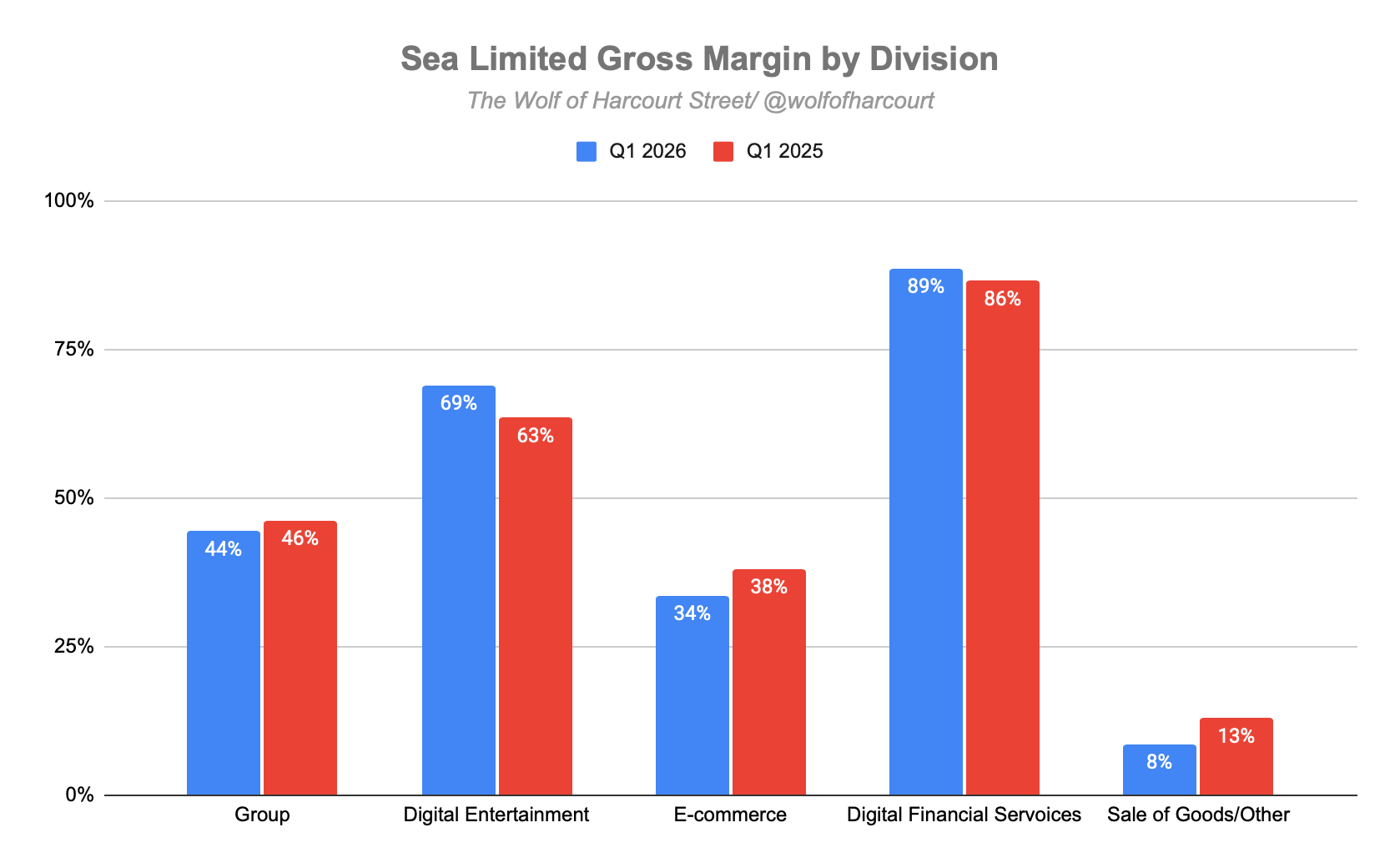

Gross Margin

Sea reported a gross margin of 44%, down from 46% in Q1 2025.

Cost of revenue increased 52% YoY to $4.0 billion, outpacing revenue growth. The margin compression reflects deliberate investment across instant delivery, fulfillment infrastructure, ShopeeVIP subsidies, and user acquisition.

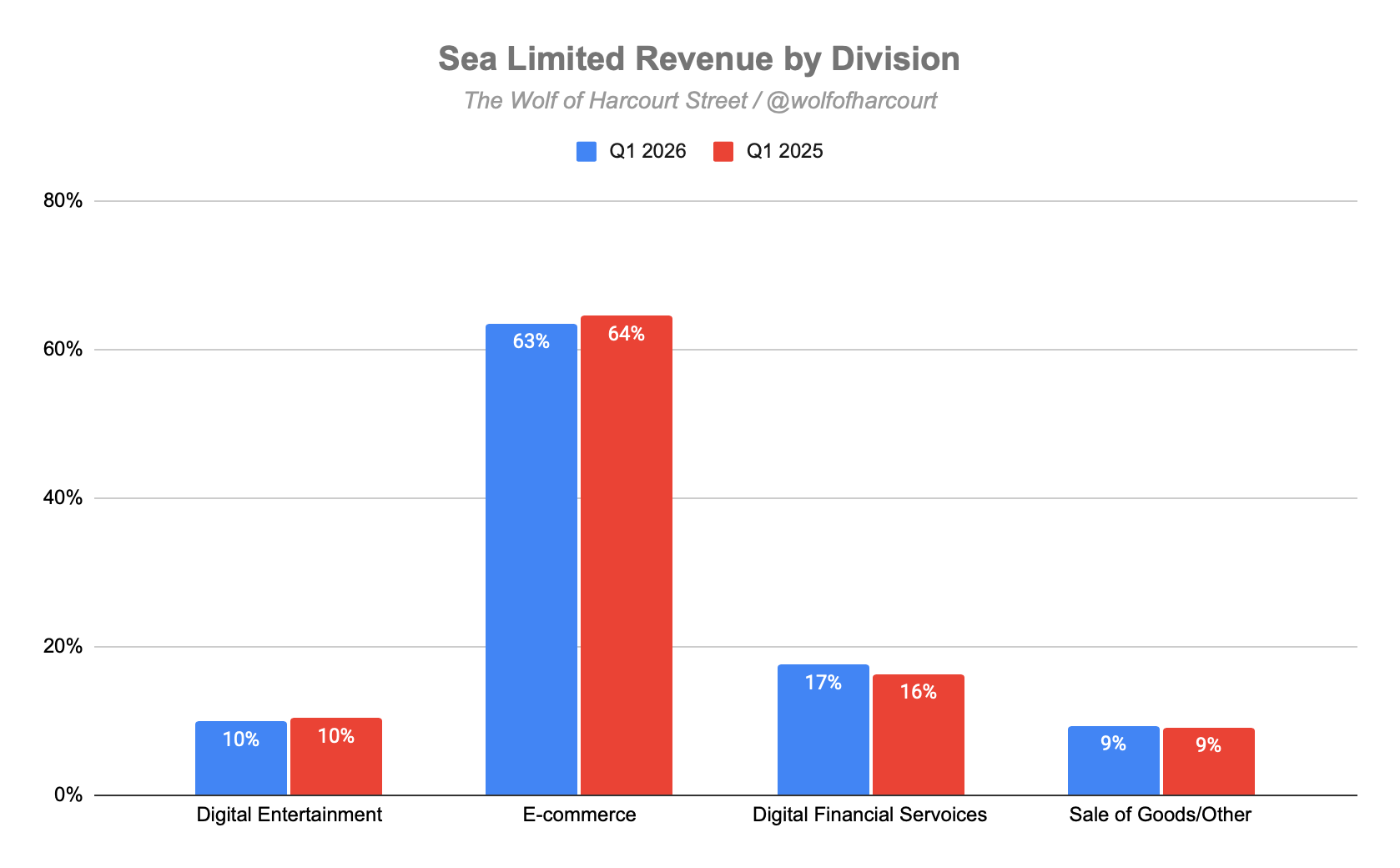

The business mix remained relatively stable:

Digital Entertainment represented 10% of revenue

Digital Financial Services increased from 16% to 17%

E-commerce declined modestly from 64% to 63%

This suggests most of the gross margin pressure came from e-commerce investments rather than structural deterioration elsewhere in the business.

Notably, both Digital Entertainment and Digital Financial Services improved their gross margins during the quarter. Digital Financial Services, in particular, expanded gross margin from 86% to 89%.

Given that Digital Financial Services is both Sea’s highest-margin and fastest-growing business segment, it is likely to become a larger share of overall revenue over time. If that trend continues, Sea’s consolidated gross margin could potentially exceed 50% over the longer term.

Operating Margin

Sea delivered record operating income of $593 million, up 30% YoY in absolute dollars, although operating margin declined slightly to 8% from 9% a year earlier.

Operating expenses increased 43% YoY to $2.6 billion, slightly below revenue growth but not enough to fully offset gross margin pressure.

Sales and marketing expense rose 52% YoY to $1.4 billion, although it remained relatively stable at roughly 20% of revenue.

The key takeaway is that marketing efficiency continues to improve.

From Q4 2025 to Q1 2026, Sea invested an additional $11 million into sales and marketing, generating approximately $246 million in incremental revenue. This suggests increasingly efficient customer acquisition and monetization across the ecosystem.

Other notable cost trends included:

Provision for credit losses increased 65% to $466 million, reflecting rapid loan book expansion while remaining manageable relative to growth.

General and administrative expense rose 32% to $404 million, broadly in line with company growth.

Research and development expense remained flat at $297 million, reflecting disciplined investment while maintaining innovation capacity.

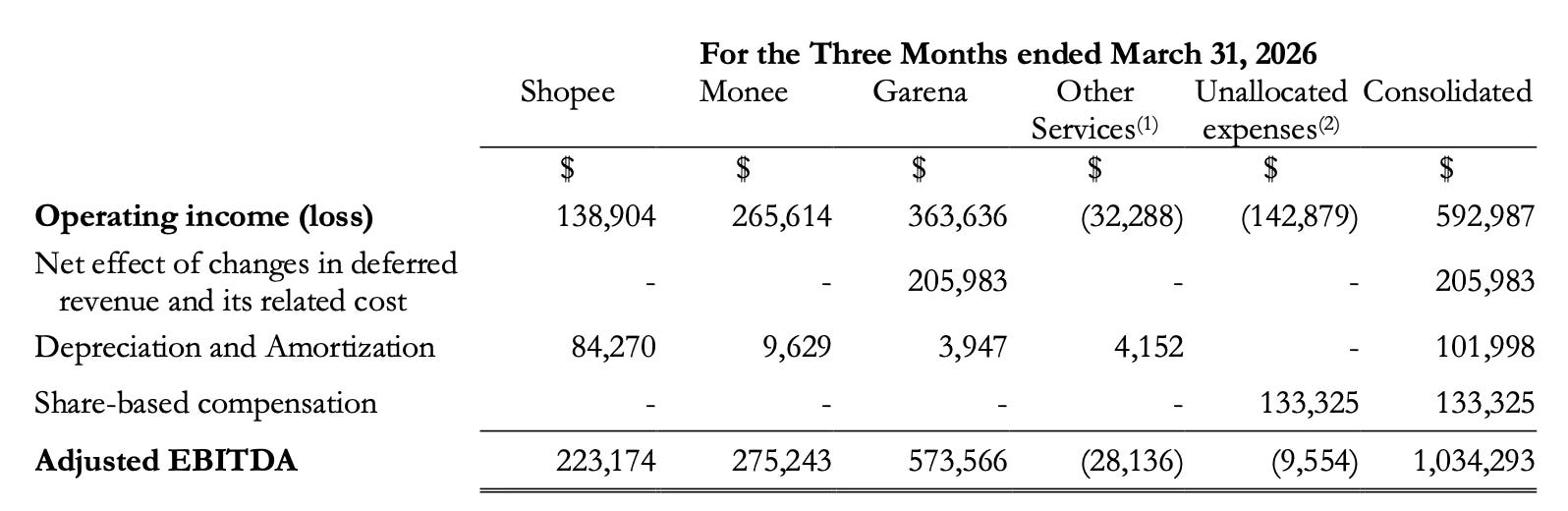

Adjusted EBITDA

Sea surpassed $1 billion in adjusted EBITDA for the first time, up 9% YoY.

Shopee’s adjusted EBITDA declined from $264 million to $223 million as management prioritized long-term investments in delivery, fulfillment, ShopeeVIP, and customer acquisition. However, improving unit economics suggest this pressure is likely temporary rather than structural.

7. Guidance

Management does not provide formal quantitative guidance but offered several important qualitative updates.

E-commerce

2026 GMV growth target of approximately 25% YoY was reaffirmed.

Full-year adjusted EBITDA is still expected to be no lower than 2025 in absolute dollar terms.

With Q1 GMV growth already reaching 30%, Shopee appears ahead of pace relative to its full-year target.

Digital Financial Services

Loan book growth is expected to continue outpacing Shopee GMV growth.

Expansion into off-Shopee use cases and Brazil remains at an early stage.

Management remains focused on maintaining stable asset quality while scaling.

Digital Entertainment

Management expects strong momentum at Garena to continue throughout 2026.

Wall Street 2026 Estimates

Current analyst expectations are:

Revenue: $29.7 billion, up 29% YoY

Adjusted EPS: $3.91, up 23% YoY

Following the Q1 results, upward estimate revisions appear likely, continuing a trend that has persisted over the past two years.

8. Conclusion

Sea Limited delivered an exceptionally strong Q1 2026, combining its fastest revenue growth in four years with record levels of absolute profitability.

Revenue increased 47% YoY to $7.1 billion, while operating income reached $593 million and adjusted EBITDA exceeded $1 billion for the first time.

At the same time, margins compressed modestly as management accelerated investment across logistics, fulfillment, ShopeeVIP, user acquisition, and off-Shopee credit expansion. Importantly, these investments appear strategic rather than defensive.

All three core businesses are performing well:

Shopee continues strengthening its logistics, content, and membership ecosystem while maintaining 30% GMV growth.

Monee is scaling rapidly across new users, geographies, and use cases while preserving excellent asset quality.

Garena has returned to growth with stronger monetization and sustained user engagement.

Most importantly, the underlying unit economics are improving:

Instant delivery costs per order declined approximately 20% YoY despite strong volume growth.

AI chatbots reduced customer service costs by roughly 30% YoY.

ShopeeVIP members demonstrated 30-40% spending uplifts.

Marketing efficiency continues improving as incremental spend drives disproportionately higher revenue growth.

These trends strongly suggest the current margin pressure is temporary and tied to investment timing rather than structural weakness.

Management’s guidance reinforces this view. Shopee still expects full-year adjusted EBITDA to be at least in line with 2025 levels while simultaneously pursuing approximately 25% GMV growth.

Perhaps most importantly, Sea is making these investments from a position of strength: strong profitability, healthy cash generation, a robust balance sheet, and leadership positions across all three businesses.

Rating: 4 out of 5. Exceeds expectations.

If you'd like to support the work of an independent analyst, you can buy me a coffee. The proceeds will contribute to covering the annual running costs of the newsletter.

Join the community of informed investors – subscribe now to receive the latest content straight to your inbox each week and never miss out on valuable investment insights.

The Chat is a space designed to facilitate, real-time discussions, share knowledge and debate ideas with fellow investors. Join the conversation.

If you found today's edition helpful, please consider sharing it with your friends and colleagues on social media or via email. Your support helps to continue to provide this newsletter for FREE!

Happy investing

Wolf of Harcourt Street

Contact me

Twitter: @wolfofharcourt

Email: wolfofharcourtstreet@gmail.com

Awesome work! The review was excellent and goes really deep in the details. Thank you!

Sea is one of the cleanest emerging market multibaggers hiding in plain sight. Free cash flow inflected hard in 2024 once the Garena drag faded, and Shopee logistics density in Indonesia is now a real moat. Curious what your read is on the SeaMoney loan book risk.