Executive Summary

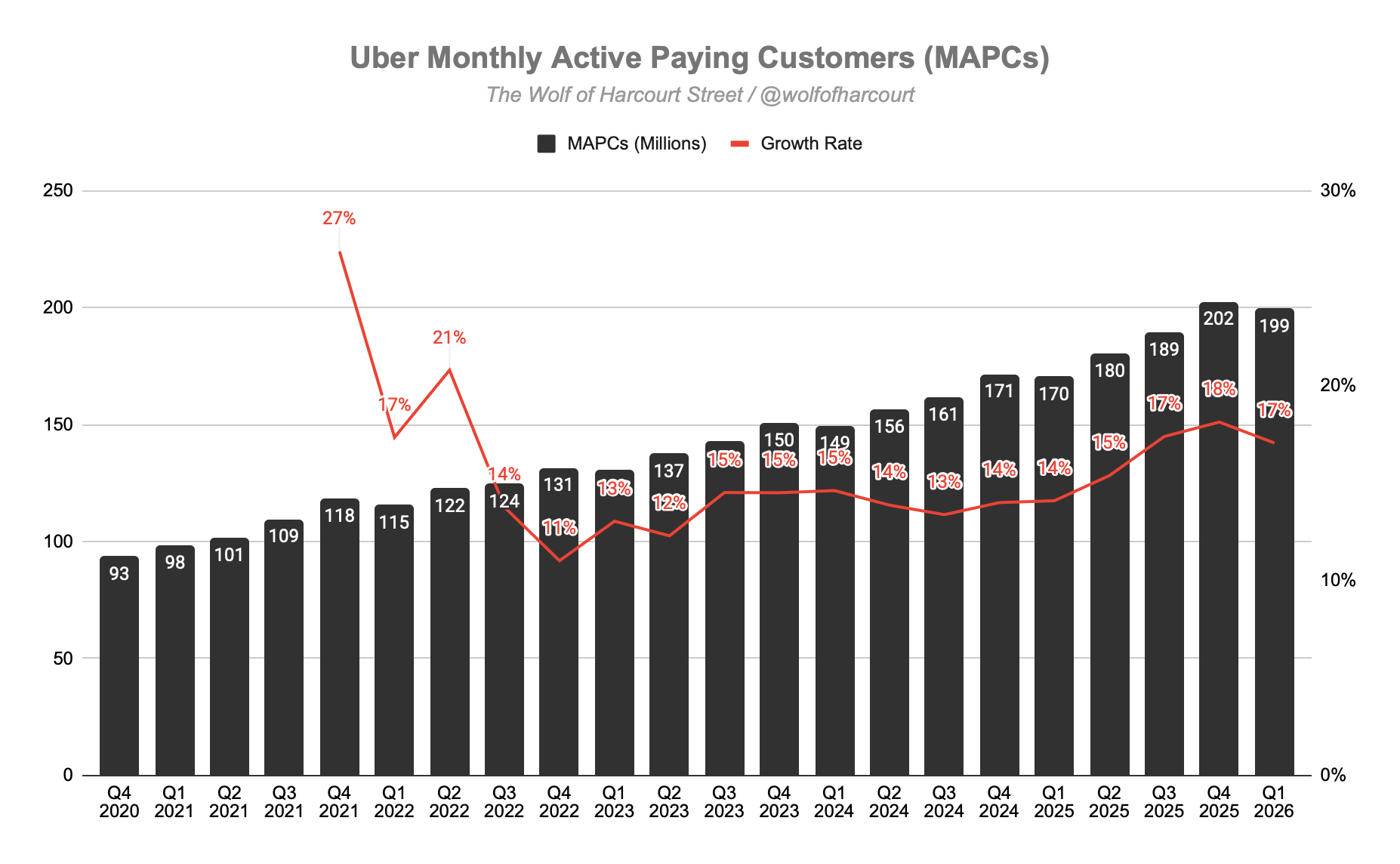

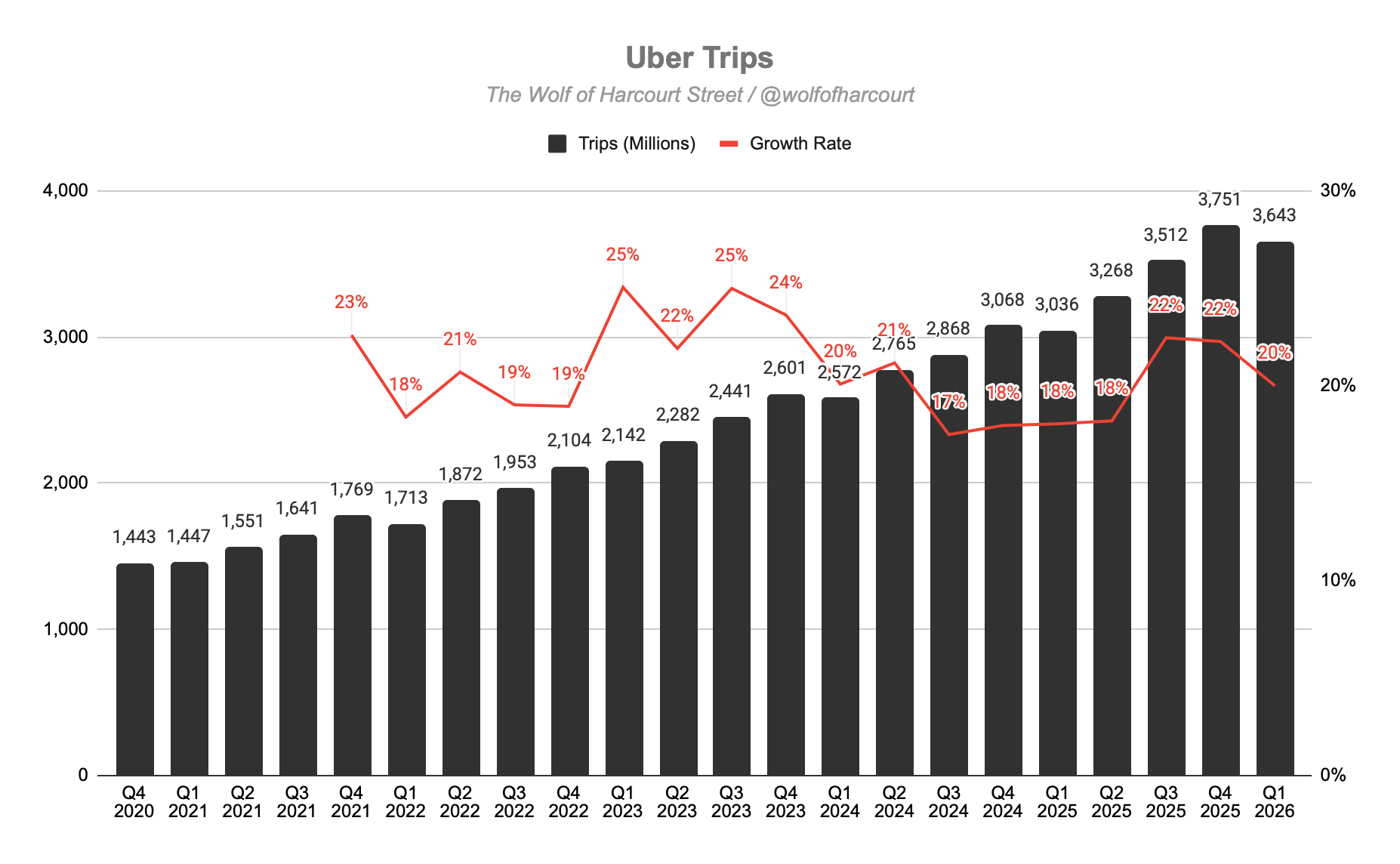

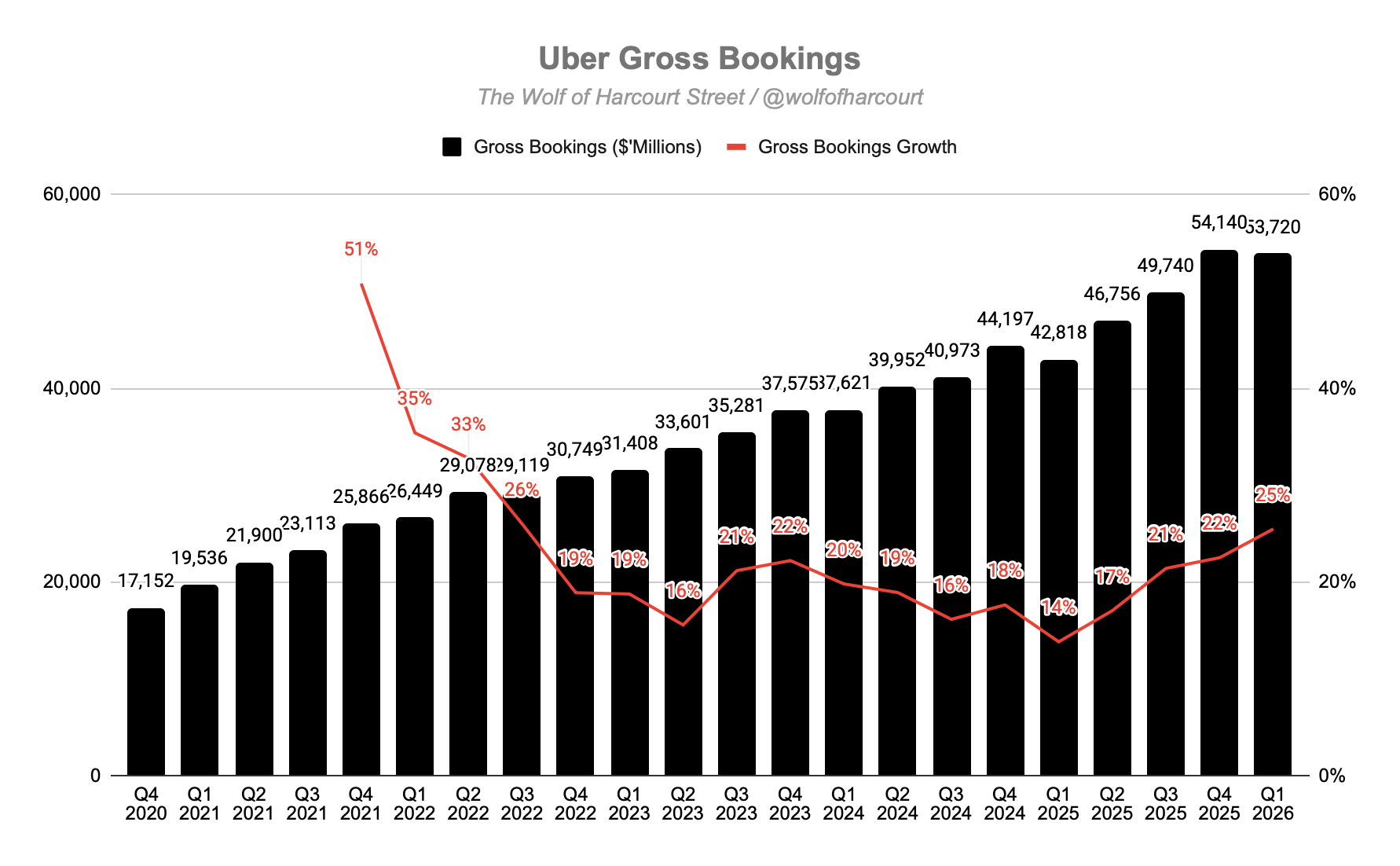

MAPCs grew 17% YoY to 199 million, accelerating from 15% growth in Q4 2025. Trip volumes surged 20% YoY to 3.6 billion while frequency remained strong at 6.1 trips per customer per month, up 3% YoY and sustaining the record engagement levels first reached in Q2 2025. Gross Bookings accelerated to 21% constant currency growth, reaching $53.7 billion.

Uber One surpassed a major milestone of 50 million members, up from 30 million at the end of 2024, meaning the company added 20 million members in just over one year. Members now account for more than 50% of combined Mobility and Delivery Gross Bookings and spend 3x more than non-members. The program continues to be the company’s primary cross-platform engagement driver.

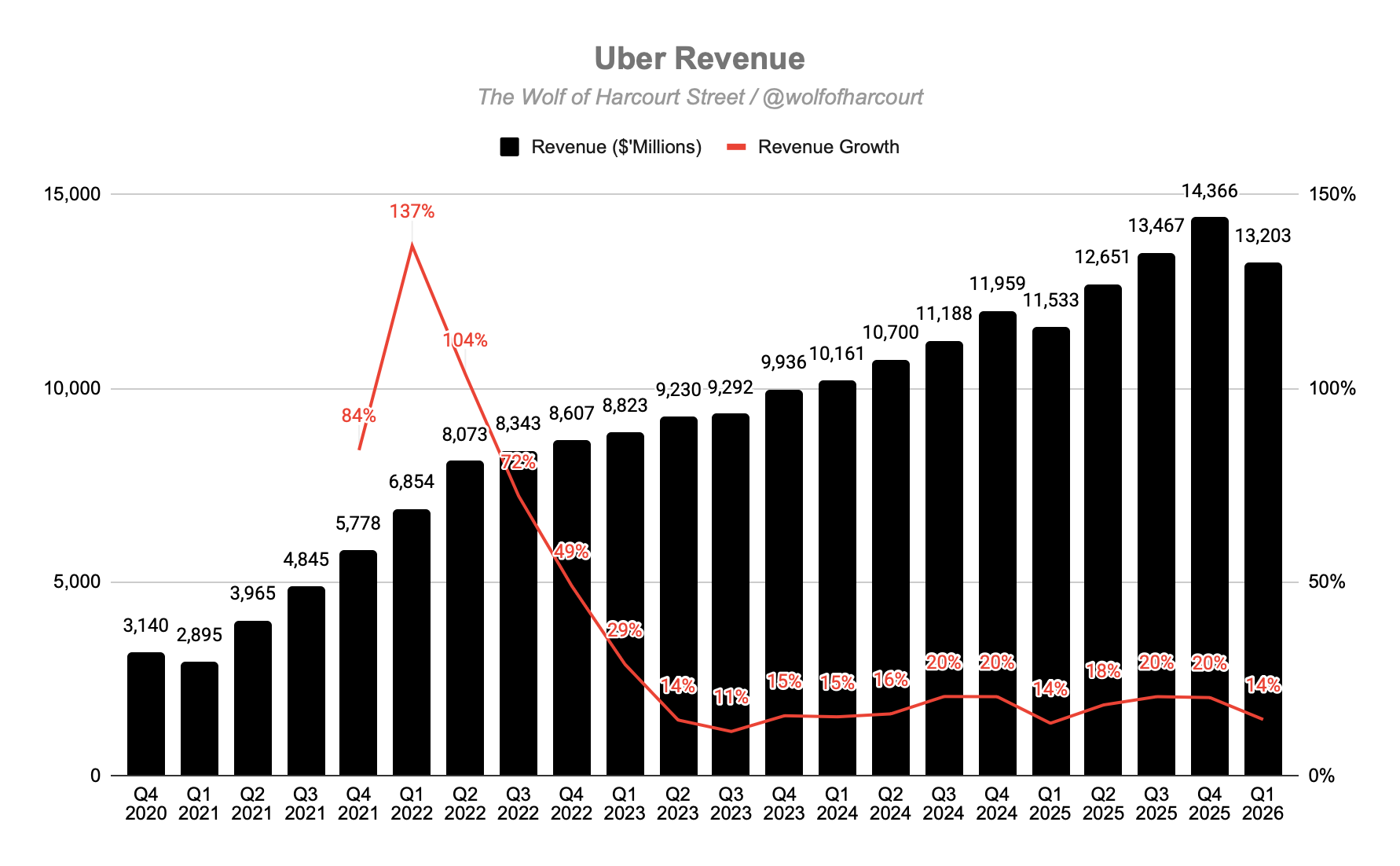

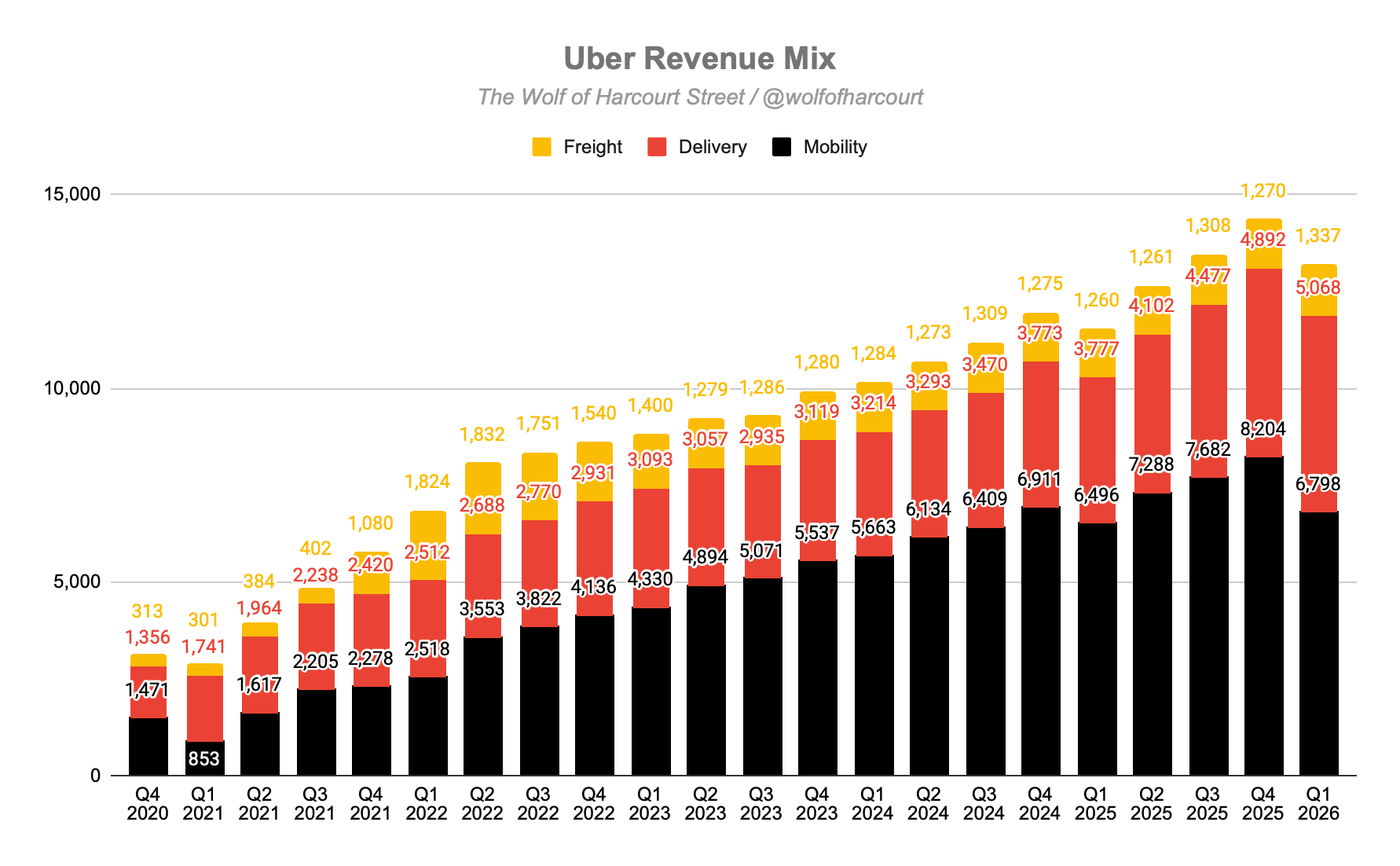

Revenue increased 14% YoY to $13.2 billion, or 10% in constant currency. Growth was impacted by business model changes that reduced reported growth by 9 percentage points, or 8 percentage points in constant currency. Mobility revenue rose 5% YoY to $6.8 billion, or 1% in constant currency, while Delivery revenue surged 34% YoY to $5.1 billion, or 28% in constant currency, driven by grocery and retail expansion alongside growing membership adoption.

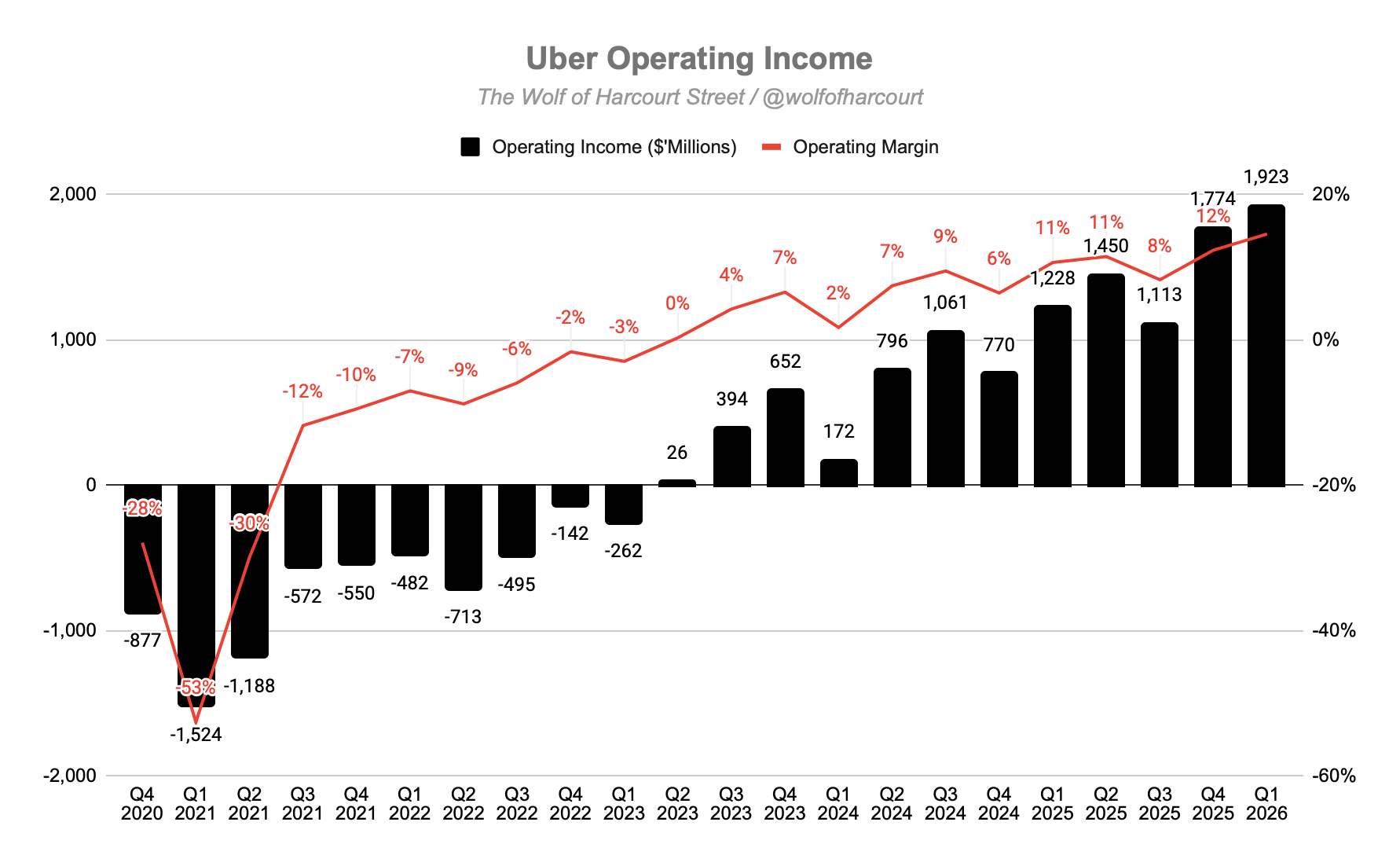

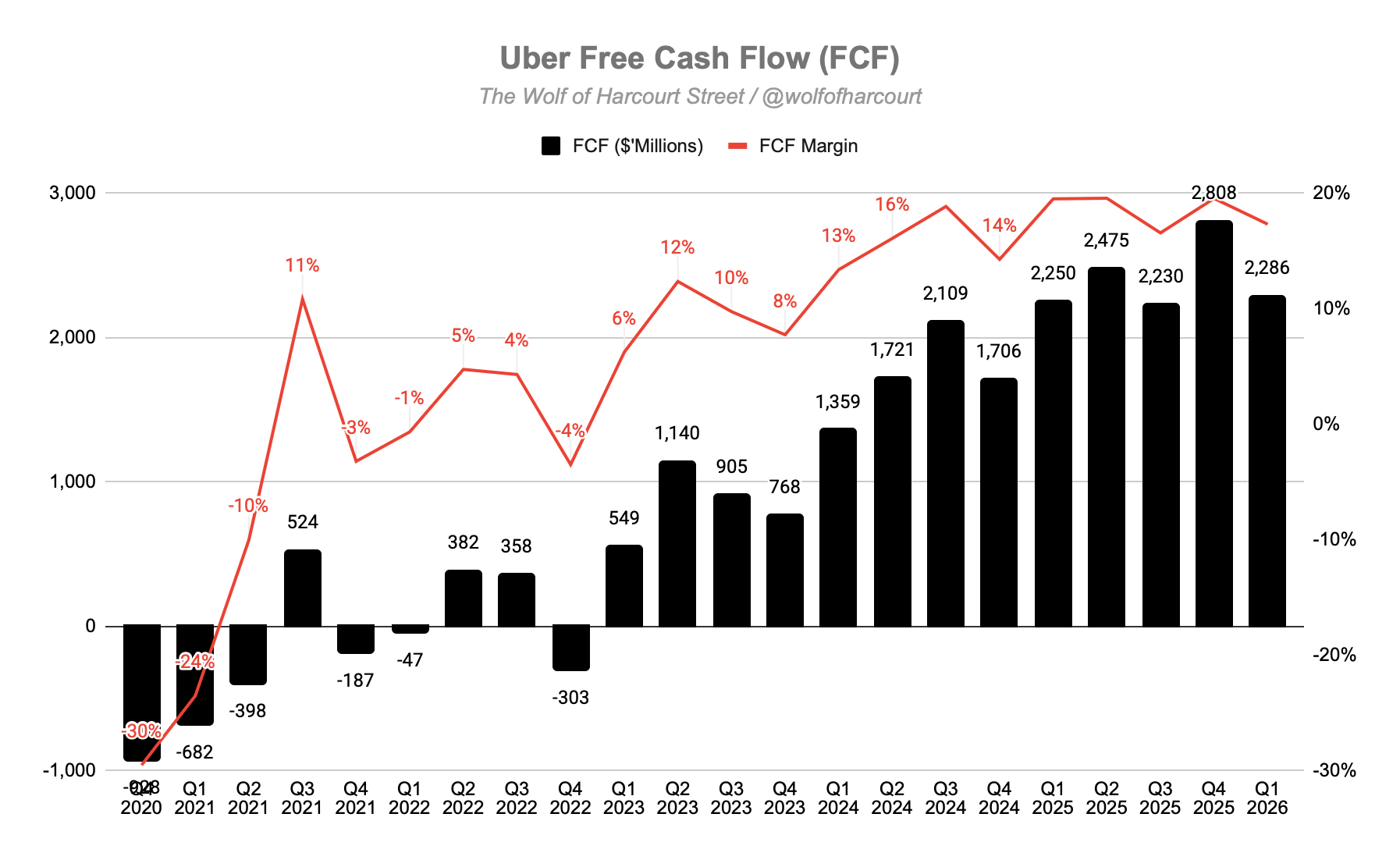

Operating income reached $1.9 billion, with margins expanding to 15% from 11% in Q1 2025, representing 57% YoY growth. Free cash flow totaled $2.3 billion, flat YoY, while the company returned a record $3.0 billion to shareholders through buybacks during the quarter. Management also expects insurance cost savings of hundreds of millions of dollars in 2026, with those savings expected to be passed on to consumers to help accelerate US Mobility growth through the remainder of the year.

Autonomous vehicle deployments increased more than 10x YoY, with Uber on track to operate in up to 15 cities by year-end through partnerships with more than 30 AV companies. New partnerships with Zoox, Nuro, Lucid, and others were announced, while the company also launched Uber Autonomous Solutions, a platform designed to provide fleet management and data infrastructure for AV partners.

Contents

Financial Highlights

Wall Street Expectations

Business Activity

Financial Analysis

Guidance

Conclusion

1. Financial Highlights

Revenue: $13.20 billion (+14% YoY)

Mobility: $6.80 billion (+5% YoY)

Delivery: $5.07 billion (+34% YoY)

Freight: $1.34 billion (+6% YoY)

Operating Income: $1.92 billion (+57% YoY)

Adjusted EBITDA: $2.48 billion (+33% YoY)

Free Cash Flow: $2.29 billion (+2% YoY)

2. Wall Street Expectations

Revenue: $13.26 billion (miss by 4%)

EPS: $0.69 (beat by 4%)

3. Business Activity

Monthly Active Paying Customers (MAPCs)

MAPCs grew 17% YoY to 199 million, accelerating from 15% in Q4 2025. This reacceleration is notable given Uber’s scale and highlights continued momentum in customer acquisition.

Management also noted that cross-platform consumers, users engaging with both Mobility and Delivery, are growing 1.5x faster than overall consumer growth. This validates Uber’s strategy of driving engagement across multiple services.

Trips

Trip volumes reached 3.6 billion, up 20% YoY.

CEO Dara Khosrowshahi highlighted that trip growth in sparse and suburban markets is growing 2x faster than core urban markets globally, representing a significant long-term expansion opportunity.

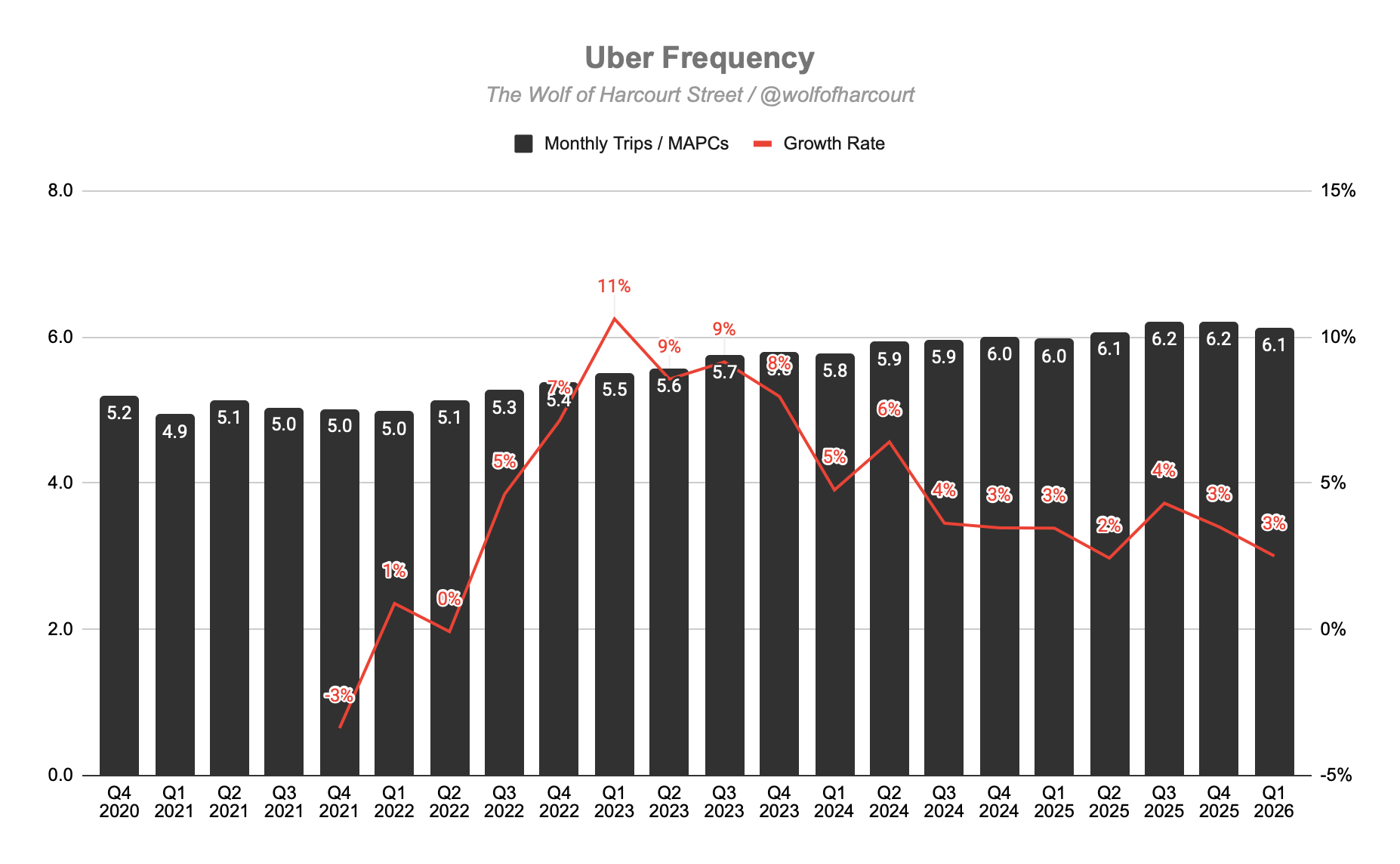

Frequency

Trips per MAPC reached 6.1 per month, compared to 6.0 in Q1 2025, representing 3% YoY growth.

Frequency has now remained in the 6.0 to 6.2 range for seven consecutive quarters, a meaningful improvement from the 5.0 to 5.5 range seen between 2020 and early 2023. Uber has successfully evolved from an occasional convenience into habitual consumer infrastructure.

Membership

Uber One reached 50 million members, up 50% YoY from roughly 36 million in Q2 2025 and 30 million at year-end 2024. That equates to 20 million net additions in just over one year.

Members now account for over 50% of combined Mobility and Delivery Gross Bookings and spend 3x more than non-members.

Management highlighted several new benefits supporting continued adoption:

10% Uber credits on hotel bookings through the new Expedia partnership, covering 700,000 hotels

Up to 20% additional savings on 10,000+ select hotels

Global membership benefits for international travelers

No delivery fees on grocery orders over $50

Member Days promotional events

Khosrowshahi commented:

“We’ve seen this growth going on for a long time. We’ve kind of wondered when it’s going to slow down. At this point we don’t see it slowing down thanks to the innovation of the team.”

Gross Bookings

Gross Bookings reached $53.7 billion, up 21% YoY on a constant currency basis, or 25% reported. This marked an acceleration from 18% constant currency growth in Q4 2025.

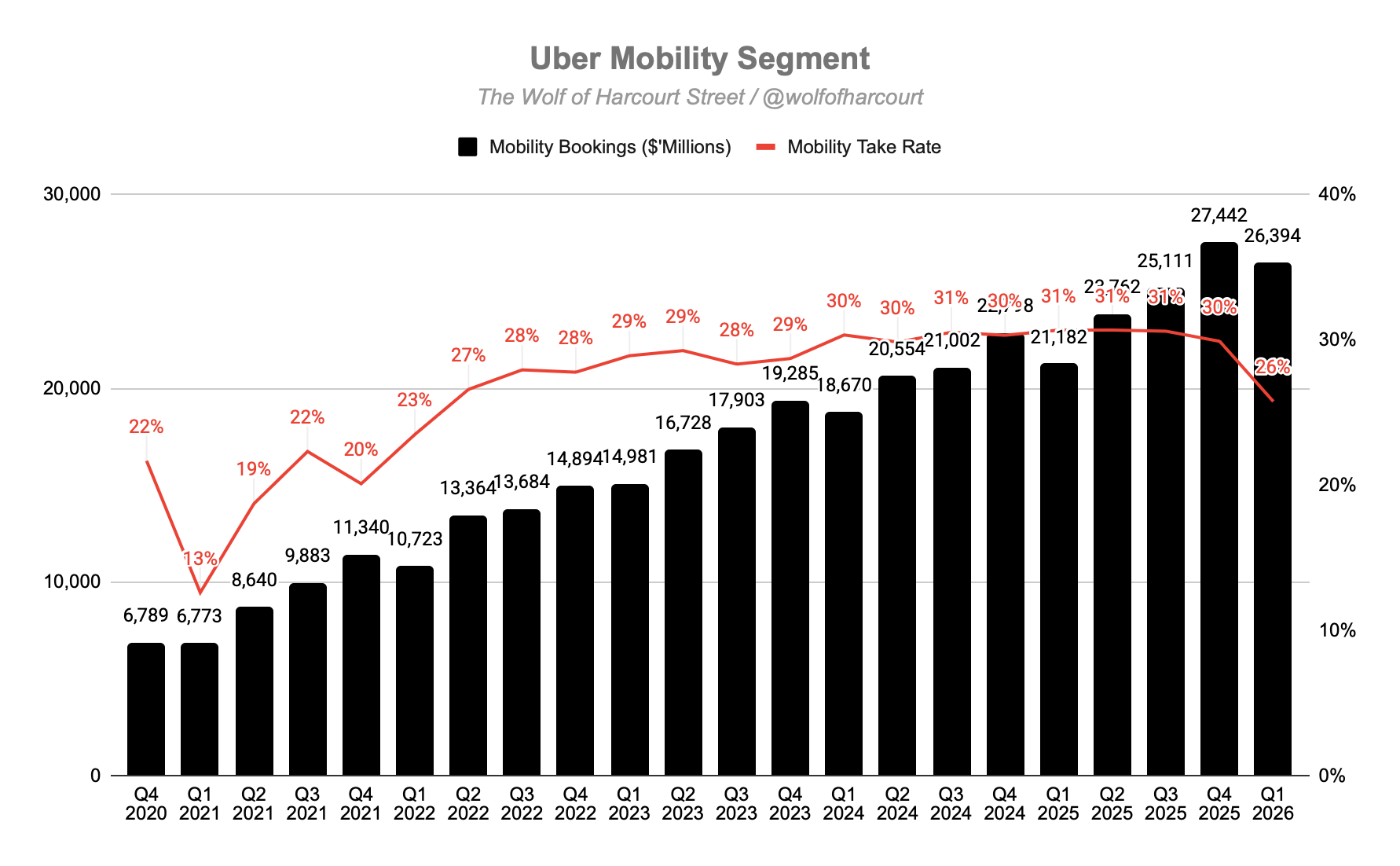

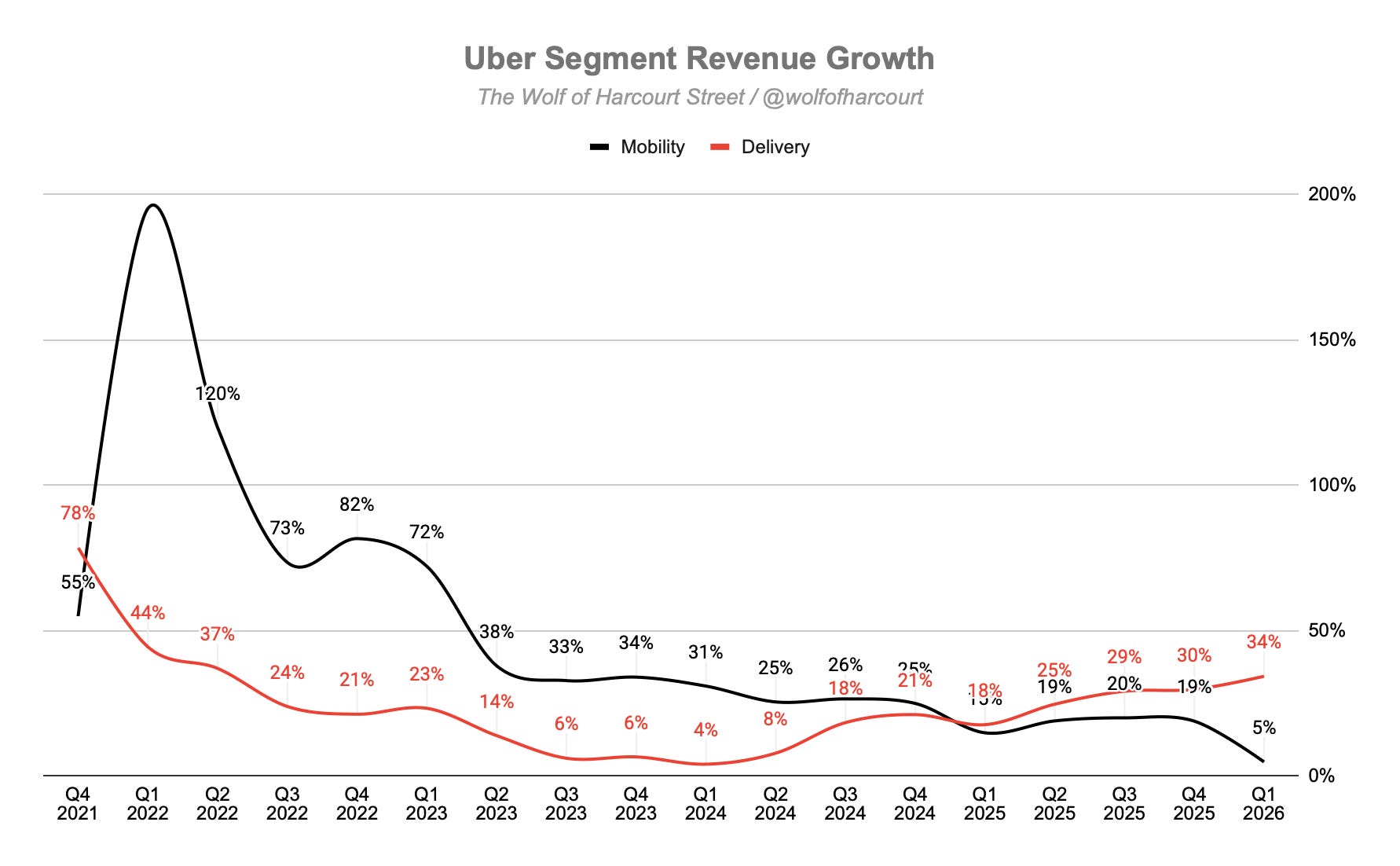

Mobility Segment

Mobility Gross Bookings grew 20% constant currency to $26.4 billion, continuing to accelerate from prior quarters. Take rates remained above 25%.

Management highlighted a “barbell strategy” supporting growth:

Affordability

Moto, two and three-wheelers, exceeded $1.5 billion in annual bookings with 40%+ trip growth

Wait & Save and shared rides continued expanding

Premium

Comfort, SUV, and Black surpassed $10 billion in annualized Gross Bookings with 35%+ trip growth

Reserve grew “well in excess” of the core business

Corporate travel grew nearly 30%

CFO Balaji Krishnamurthy provided important commentary on insurance costs:

“This will be the first year since COVID where we expect to see good leverage on our insurance cost line for the US Mobility business.”

Auto insurance renewals in March produced favorable terms, with management expecting hundreds of millions of dollars in insurance savings during 2026. These savings are being reinvested into lower prices to accelerate trip growth.

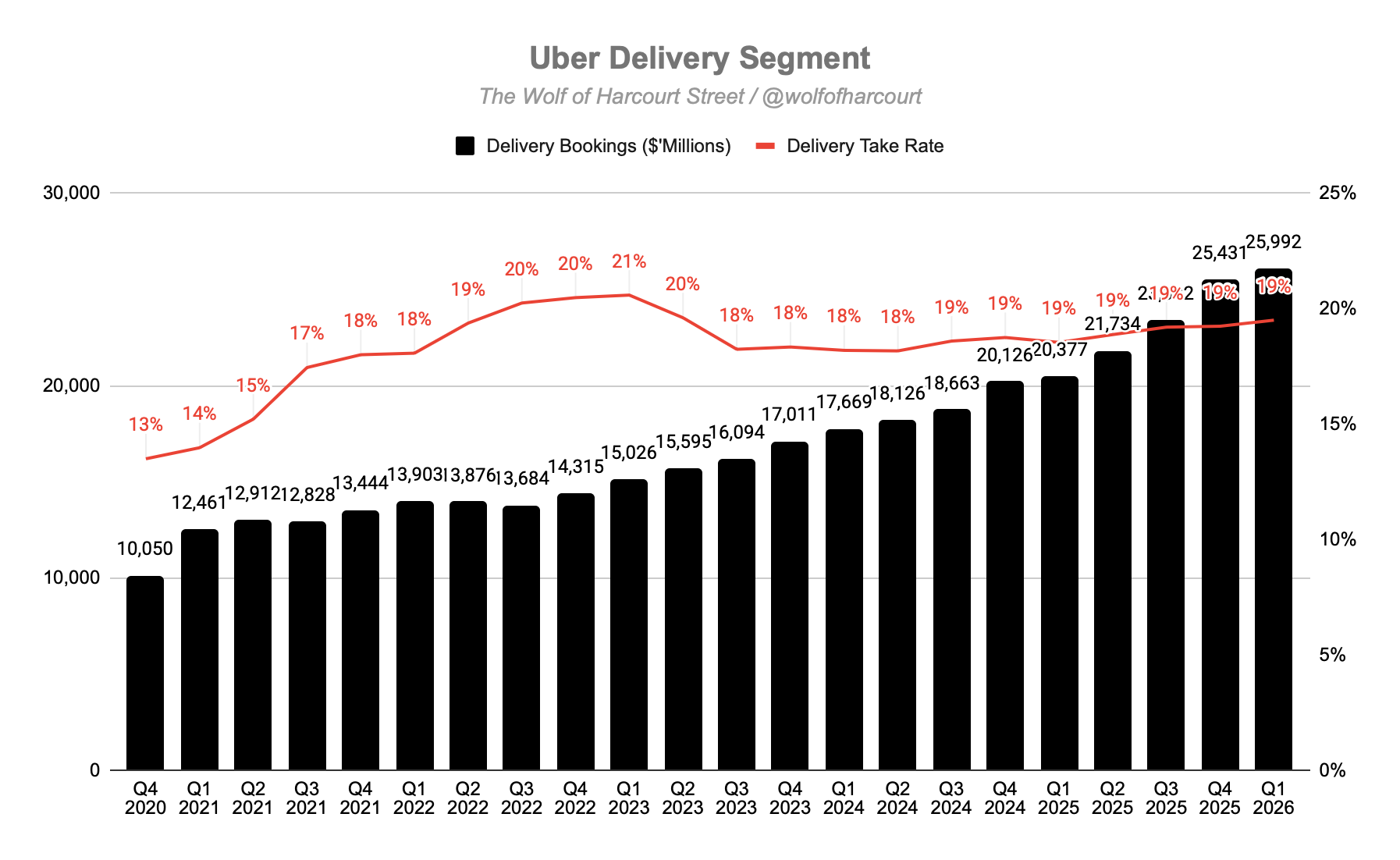

Delivery Segment

Delivery Gross Bookings grew 23% constant currency to $26.0 billion, while take rates remained steady at 19%.

This was the fourth consecutive quarter of accelerating growth, driven by:

Grocery & Retail expansion, with selection growth at its fastest pace in nearly three years

Rising Uber One adoption, which drives materially higher frequency

Cross-platform engagement across the Uber ecosystem

Management noted that the Delivery tab inside the Mobility app generated $15 billion in annualized Delivery Gross Bookings, nearly $4 billion per quarter, while also acquiring 30% of first-time Delivery customers.

Importantly, 30% of eligible Mobility users have never tried Delivery, while 75% have never used Grocery & Retail. This represents a massive long-term cross-sell opportunity.

Freight Segment

Freight returned to growth for the first time in nearly two years, with Gross Bookings rising 6% YoY to $1.3 billion.

The segment still represents less than 3% of total company Gross Bookings.

4. Financial Analysis

Revenue

Revenue grew 14% YoY to $13.2 billion, or 10% in constant currency.

However, business model changes negatively impacted reported growth by 9 percentage points. Excluding these changes, underlying revenue growth would have been approximately 23% YoY, much closer to the company’s 21% constant currency Gross Bookings growth.

The revenue mix continues to differ materially from Gross Bookings due to varying take rates:

Mobility represented 49% of Gross Bookings but 52% of revenue

Delivery represented 48% of Gross Bookings but only 38% of revenue

Mobility revenue grew 5% YoY to $6.8 billion. The relatively modest growth versus 20% Gross Bookings growth reflects both business model changes and management’s decision to pass insurance savings back to consumers through lower prices.

Delivery revenue grew 34% YoY to $5.1 billion, marking the fastest growth rate since Q2 2022. Growth was driven by Grocery & Retail expansion, rising Uber One adoption, and stronger cross-platform engagement.

Operating Margin

Operating income reached $1.92 billion, with operating margins expanding to 15% of revenue versus 11% in Q1 2025. Absolute operating income increased 57% YoY.

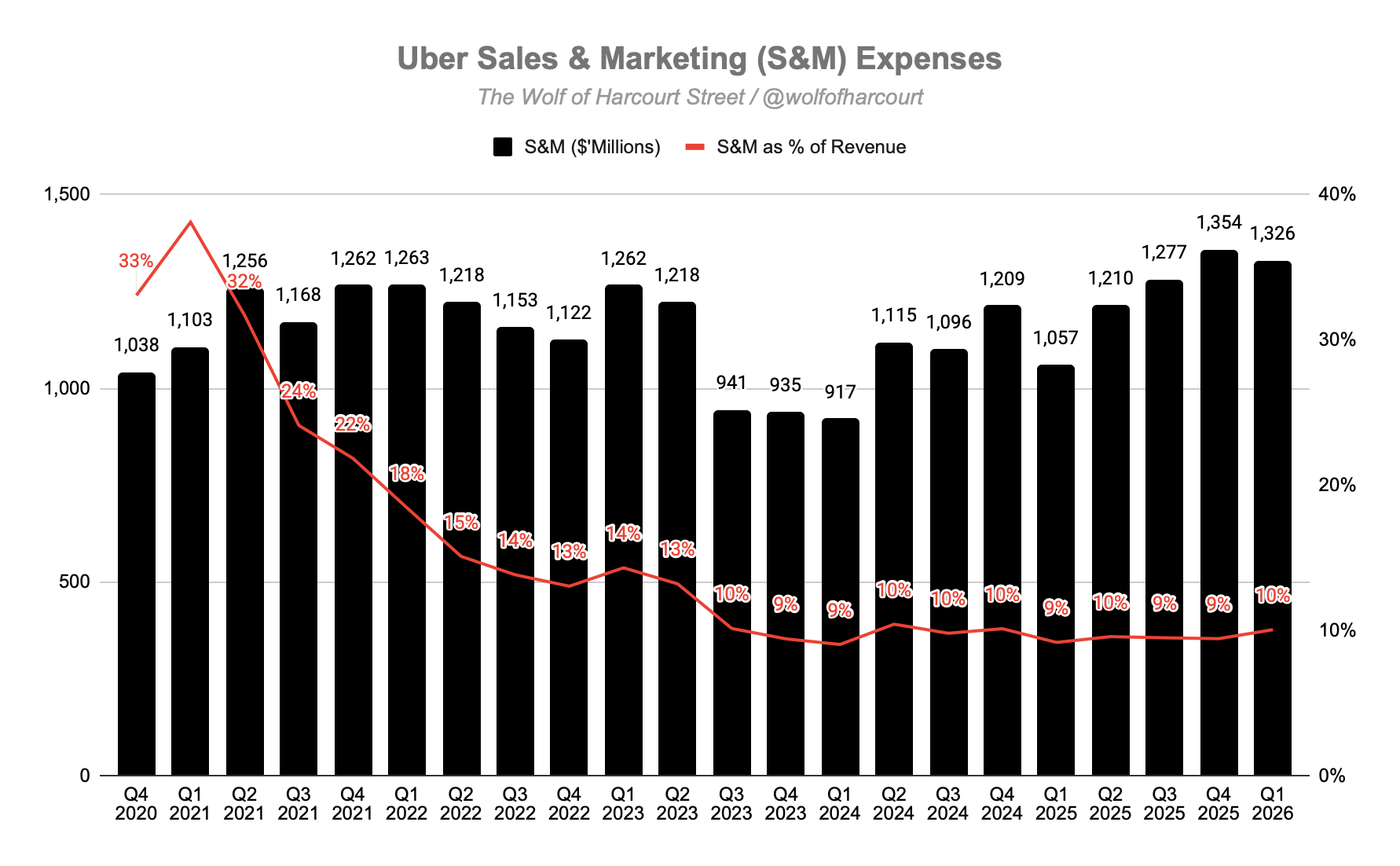

Sales & Marketing remains Uber’s largest operating expense. This line includes customer promotions, though driver incentives are recorded within cost of revenue.

At its peak, Uber spent nearly 40% of revenue on Sales & Marketing. That figure has now stabilised between 9% and 10% over the past two and a half years, a dramatic improvement in efficiency.

Khosrowshahi also highlighted the growing impact of AI on productivity:

“About 10% of our code now that is committed is built by agents, autonomous agents...if every person in this company can increase their throughput by 20%, 30%, 50%, 100%, then I think metering head count growth and leaning in on AI investment is going to be well worth it.”

Krishnamurthy added further context around the company’s investment strategy:

“On our barbell for Mobility, the low-cost products that we’ve been investing behind, they drive 75% higher frequency than our core products. And on the other end of the spectrum, our higher fare premium products drive 3.5 times higher profit growth for the company.”

Net Margin

Uber reported net income of $263 million, impacted by a $1.5 billion pre-tax headwind related to revaluations of equity investments.

Cash Flow Analysis

Free cash flow reached $2.29 billion, up 2% YoY, with trailing twelve-month FCF now exceeding $9 billion.

Operating cash flow totaled $2.35 billion, while CapEx remained extremely low at just $65 million, reinforcing the strength of Uber’s asset-light business model.

The company also returned a record $3.0 billion to shareholders through buybacks during Q1 2026, part of the broader $20 billion buyback program announced in 2025.

5. Guidance

For Q2 2026, management expects:

Gross Bookings growth of 18% to 22% constant currency, equating to approximately $56.25 billion to $57.75 billion

Adjusted EBITDA of $2.70 billion to $2.80 billion, representing 31% to 38% YoY growth

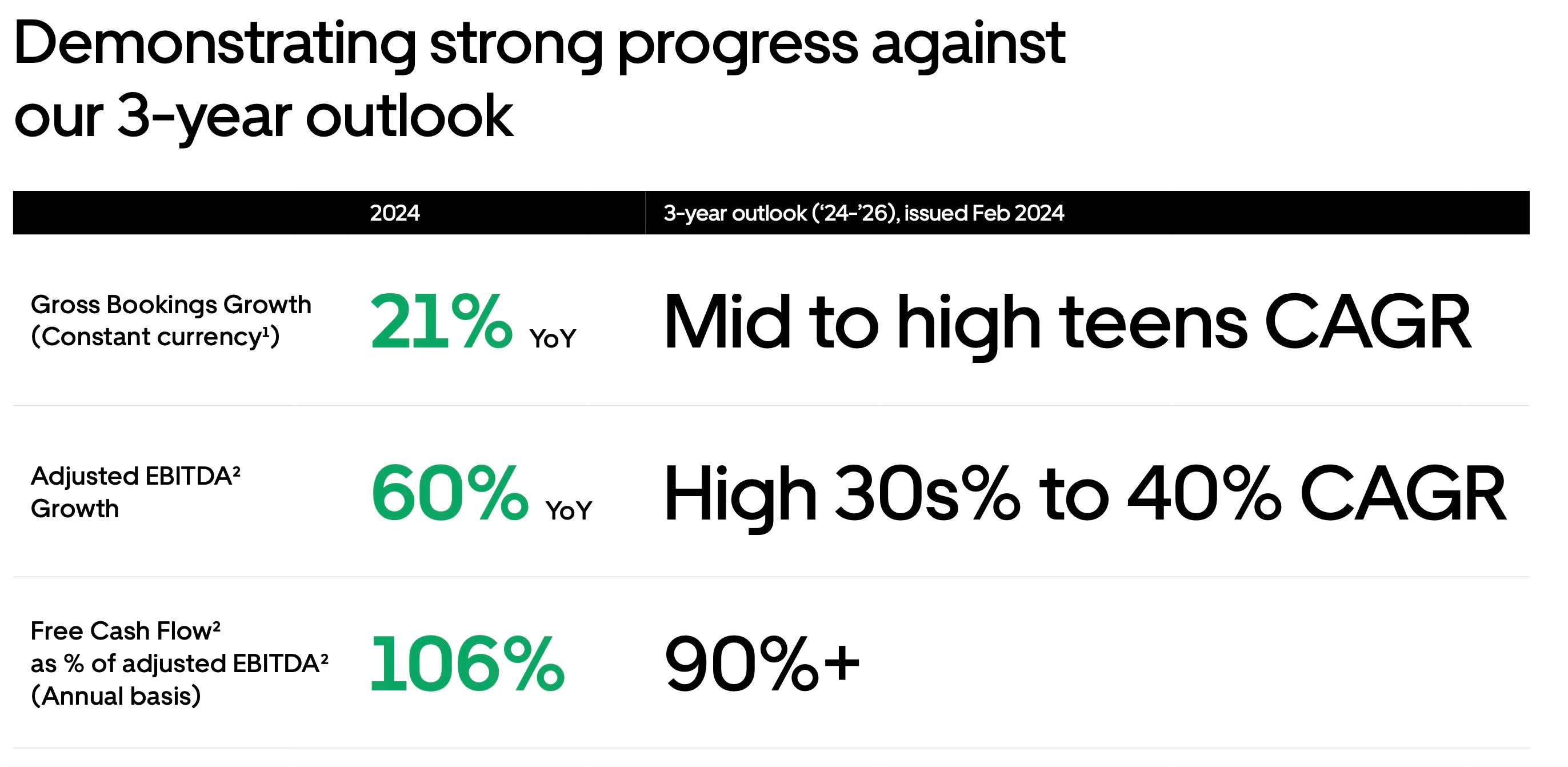

Importantly, guidance remains comfortably within the company’s three-year outlook issued in February 2024.

6. Conclusion

Uber delivered an outstanding Q1 2026, further reinforcing the strength and durability of its platform model.

1. The Uber One flywheel is accelerating

Uber One reached 50 million members, up from 30 million just one year ago. Members now account for more than 50% of Gross Bookings and spend 3x more than non-members.

With new benefits such as hotel partnerships being layered into the ecosystem, Uber is building a powerful consumer subscription model that competitors will struggle to replicate.

2. Growth is reaccelerating across the business

MAPCs: +17%, accelerating from +15%

Trips: +20%, the strongest growth since Q3 2023

Gross Bookings: +21% constant currency, accelerating from +18%

The narrative that Uber is becoming a mature, slower-growth business increasingly looks outdated. Delivering 20% trip growth at a base of 3.6 billion quarterly trips is exceptional execution.

3. Insurance savings are becoming a major tailwind

Management’s commentary around insurance costs was among the most bullish in years.

With hundreds of millions in expected savings being reinvested into lower pricing, Uber appears positioned for sustained acceleration in US Mobility. Management specifically highlighted improved trends in Los Angeles, historically one of the company’s most insurance-constrained markets.

4. The cross-platform opportunity remains enormous

Management disclosed that 30% of Mobility users have never tried Delivery, while 75% have never engaged with Grocery & Retail.

Meanwhile, the Mobility app already generates $15 billion in annualized Delivery Gross Bookings. The scale of the cross-sell opportunity remains underappreciated and still appears to be in its early innings.

5. AI is improving productivity, not just increasing costs

Uber’s AI investments are already showing tangible operational benefits.

Management disclosed that 10% of committed code is now agent-generated, while engineering productivity continues improving. Combined with moderated headcount growth, this positions Uber to continue expanding margins while still investing aggressively in growth initiatives.

Overall, Q1 2026 demonstrated how far Uber has evolved from its earlier “growth at all costs” era.

The company is now simultaneously compounding growth, profitability, and free cash flow, while maintaining strong strategic focus across AI, autonomous vehicles, sparse markets, and platform expansion.

Khosrowshahi continues to establish himself as one of the strongest non-founder CEOs in public markets. Returning $3 billion to shareholders in a single quarter while still investing heavily for future growth highlights both disciplined capital allocation and exceptional execution.

If you'd like to support the work of an independent analyst, you can buy me a coffee. The proceeds will contribute to covering the annual running costs of the newsletter.

Join the community of informed investors – subscribe now to receive the latest content straight to your inbox each week and never miss out on valuable investment insights.

The Chat is a space designed to facilitate, real-time discussions, share knowledge and debate ideas with fellow investors. Join the conversation.

If you found today's edition helpful, please consider sharing it with your friends and colleagues on social media or via email. Your support helps to continue to provide this newsletter for FREE!

Happy investing

Wolf of Harcourt Street

Contact me

Twitter: @wolfofharcourt

Email: wolfofharcourtstreet@gmail.com

Hi Wolf,

Been a while!

Great write-up as always. One thing I'd love to hear your thoughts on: the mobility segment did 25% more in gross bookings YoY but only 5% more in revenue (flat in constant currency). You attribute this largely to business model changes and the reinvestment of insurance savings, but a bear would argue that Uber was forced to cut prices to sustain volume growth in an increasingly competitive mobility market - particularly with Waymo now at ~40% rideshare market share in SF and expanding into LA, Phoenix, Austin, Atlanta, and Miami.

Two specific questions:

- If the insurance savings are truly being chosen to reinvest rather than required to remain competitive, why isn't that showing up as margin expansion in mobility specifically rather than just at the consolidated level? Wouldn't a company with pricing power keep some of the savings?

- You highlight that 30% of mobility users haven't tried delivery and frame it as upside optionality. But couldn't you flip that around if cross-sell conversion hasn't happened after years of pushing it, is it really latent demand or just a segment that doesn't want delivery?

Not trying to rain on the parade. I'm genuinely curious how you'd stress-test the bull case against the pricing/take rate compression trend in mobility.

Uber is executing exceptionally right now, Uber one has an incredible price/value ratio which I can personally atone to, It gives me so much back in direct cost savings and credits that for the price I couldn't imagine cancelling it. I think it has great potential and has long played an important part in my thesis considering the effect it has on increased usage as well as strengthening the moat