Executive Summary

Total customers continue to grow but Datadog’s revenue mix is becoming increasingly concentrated. A small subset of high-value customers (10% of total) contributes around 85% of the company's ARR.

Trailing 12-month NRR dropped below 130% in Q2 for the first time in over three years. Despite some churn among smaller customers, Datadog maintains a strong gross revenue retention rate in the mid to high 90s. Anticipated NRR decline below 120% in the next quarter suggests potential moderation in customer growth despite increased product adoption.

Substantial customer portfolio growth continues to result strong revenue growth. Efficient management of cloud costs contributed to surpassing the long-term target gross margin in the high 70s. Opex increased by 31% YoY, a slowdown from the previous quarter's growth rate of 50%. Management note a controlled approach to spending amid macro uncertainties.

Contents

Key Highlights

Wall Street Expectations

Business Activity

Financial Analysis

Guidance

Conclusion

1. Key Highlights

Revenue: $509.5 million +25% year-over-year (YoY)

Gross Profit: $407.6 million +26% YoY

Operating Loss: $22 million compared to a loss of $3 million YoY

2. Wall Street Expectations

Revenue: $501 million (beat by 2%)

Adjusted Earnings per Share: 0.63 (beat by 29%)

Source: Zachs

3. Business Activity

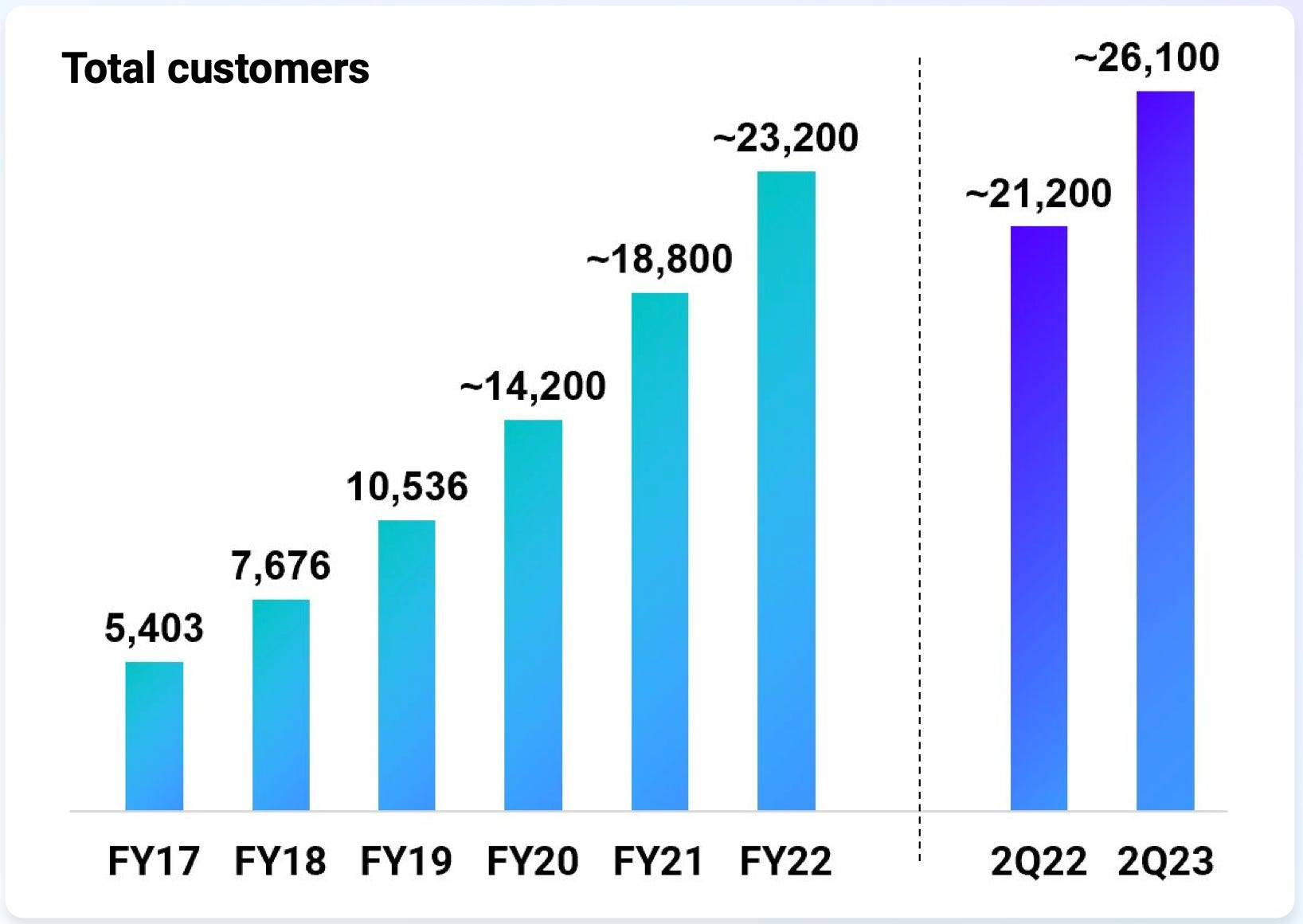

Total Customers

Total customers increased by 23% YoY to 26,100. On a sequential basis, total customers increased 2% quarter-over-quarter (QoQ).

While the total paying customer count was not disclosed in the earnings release, CFO David Obstler disclosed on the conference call that about 200 customers who were considered financially immaterial and were at the very low end in terms of spending were moved from the paying customer category to the free tier. This is a one-time action aimed at streamlining the customer base and focusing on more significant revenue-generating customers.

Annual Reoccurring Revenue (ARR)

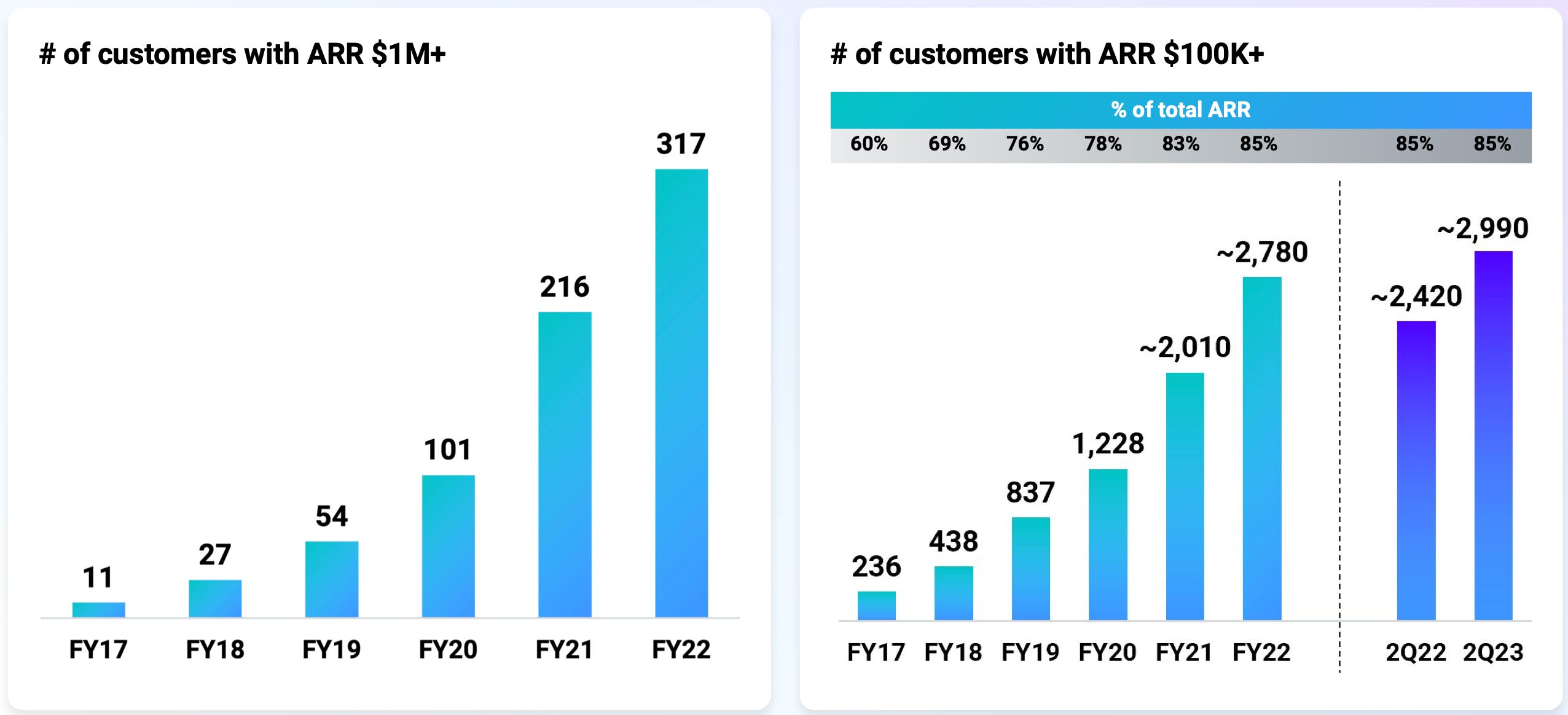

Datadog’s ARR base continues to increase with the number of customers with ARR $100k+ growing 24% to 2,990.

A significant portion of the company's ARR is derived from a relatively small subset of customers. The data reveals that these high-value customers with an ARR of $100,000 or more contribute substantially to the company's revenue stream. The mentioned subset of customers, representing around 10% of the total customer count, collectively account for approximately 85% of the company's ARR.

Platform Adoption

Datadog platform adoption is showing no signs of slowing down as customers continue to use more products on the platform. As of the end of Q2, 82% of customers are utilizing two or more products, indicating a steady increase from the previous year's 79%.

The trend of adopting more products is even more pronounced further along the spectrum.

45% of customers are now using four or more products, marking a significant rise from the 37% reported a year ago.

21% of customers have embraced six or more products, demonstrating substantial growth compared to the 14% from the previous year.

The increasing multiproduct adoption isn't limited to existing offerings; it also extends to the company's latest products. Approximately 30% of customers have integrated at least one of the products launched since 2021 into their operations. This includes products like CI visibility, database monitoring, cloud security management, sensitive data scanner, Cloudcraft, and others.

Customer Retention Rate

Datadog is observing churn among smaller customers, but management have suggested that their impact on overall revenues is limited. Despite this churn, the gross revenue retention rate remains strong, staying in the mid to high 90s range. This indicates that customers are finding value in the product and consider it important for their operations.

In Q2, the trailing 12-month Net Retention Rate (NRR) rated dropped below 130% for the first time in over three years. Despite the decline in NRR from the previous quarter, it remained above 120% due to customers focusing on optimising their technology costs and enhancing efficiency.

Management anticipates a potential decrease in NRR below 120% in the next quarter if the current growth trajectory is maintained, which suggests that while existing customers are adopting more products, the rate of growth might moderate.

4. Financial Analysis

The impressive growth and expansion of Datadog's customer portfolio have led to a substantial increase in revenue over the recent years. This trend continued in Q2 with revenue growing 25% YoY.

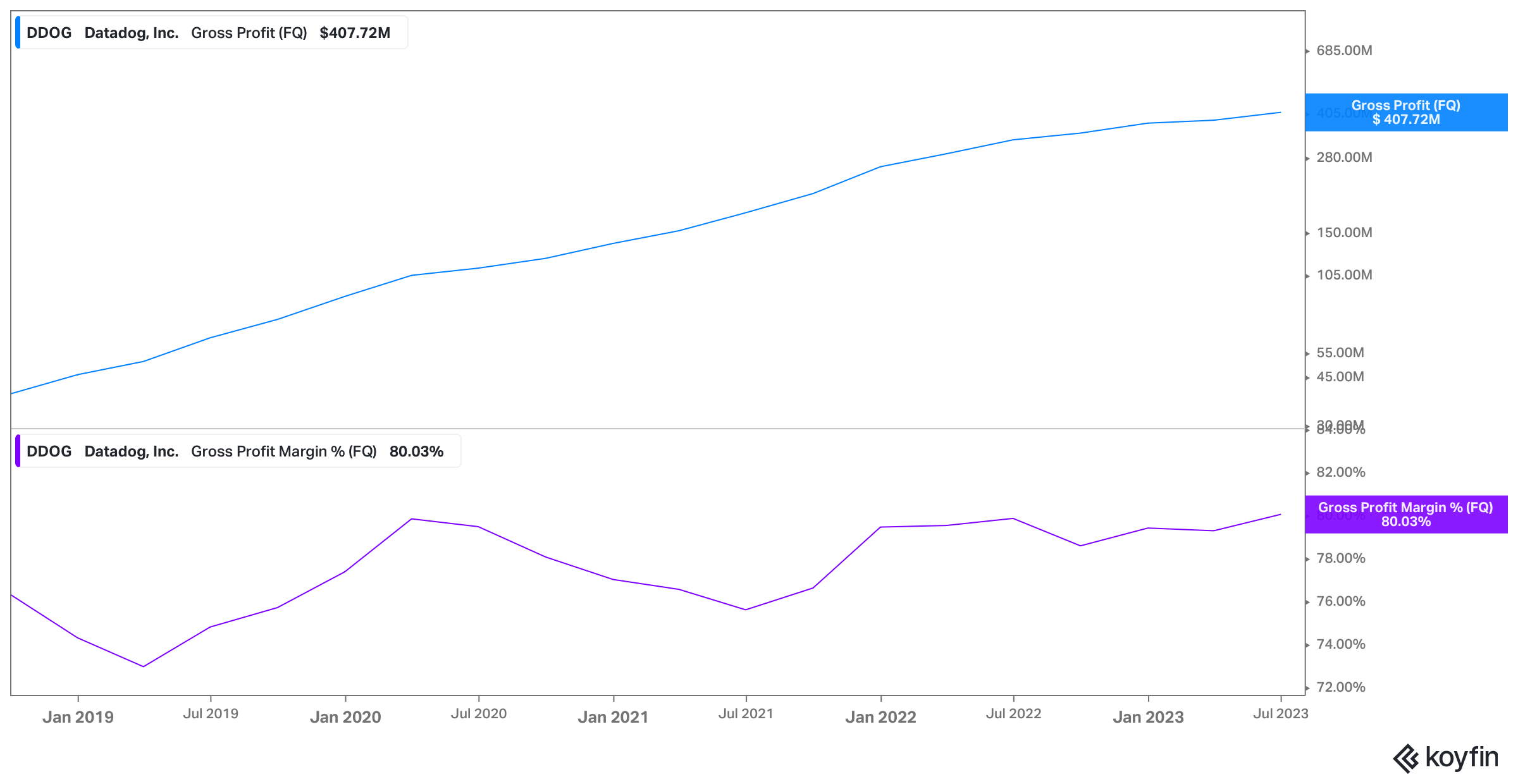

Datadog reported an 80% gross margin for Q2 representing an increase compared to the previous quarter's gross margin of 79% and in line with the gross margin of 80% in the same quarter of the previous year.

All of the subsequent charts are from Koyfin which is the tool that I use to screen and analyse stocks. In my opinion, it is the most comprehensive financial data and visualisation tool that makes the research process so much easier for investors. If you would like to try it for yourself, follow the link below to receive a 10% discount.

The sequential improved gross margin is attributed to the company's ongoing efforts to achieve efficiencies in cloud costs, which are reflected in the Cost of Goods Sold (COGS). Cloud costs generally refer to the expenses associated with using third-party cloud computing resources and services, which are a significant component of many technology companies' cost structures. Datadog's ability to optimize and manage these costs more efficiently contributed to the higher gross margin which is exceeding the company's target in the high 70s.

Operating expenses (Opex) grew by 31% YoY Q2 representing a decline from the previous quarter's opex growth rate of 50% YoY. This suggests that the company managed to slow down the rate at which its operating expenses were increasing, reflecting a more controlled approach to spending. On the conference call, management noted that “we moderated our hiring pace and executed on controlling costs given the macro uncertainties”.

The most significant component of Opex is Research & Development (R&D) expenses which increased by 35% to $239 million. Datadog's dedication to innovation and staying ahead is evident in the rise of R&D expenditure as a share of revenue, climbing from 23% in 2017 to 47% in Q2 2023. This underscores their commitment to sustaining competitiveness through continuous investment in novel products and features.

Sales & Marketing (S&M) costs rose by 28% to $147 million, aligned with a 25% revenue increase. Notably, S&M spending relative to revenue has decreased over six years, dropping from 45% in 2018 to 29% in Q2 2023. Datadog directs gross profit into R&D for enhanced product features, prioritizing existing and potential customers over customer acquisition expenses.

Cash Flow Analysis

Datadog’s operating cash flow more than doubled in Q2 to $153 million. A significant portion of this increase can be attributed to the sharp rise in stock-based compensation (SBC) expenses. The 44% Q2 increase in SBC to $118 million, almost twice the pace of revenue growth, implies a significant allocation of stock-based compensation to staff.

Overall, Datadog produced free cash flow (FCF) of $151 million more than doubled from $67 million YoY. This is resulting in a very healthy FCF margin of 30%. FCF margin excluding SBC is 6%.

5. Guidance

Q3 2023

Revenue: $521 million to $525 million, which represents a 19% to 20% YoY growth.

Adjusted EPS: $0.33 to $0.35.

Full Year 2023

Revenue: $2.05 billion to $2.06 billion, which represents 22% to 23% YoY. This is lowered from the previous guidance of between $2.08 billion and $2.10 billion.

Adjusted EPS: $1.30 to $1.34. This is risen from the previous guidance of between $1.13 and $1.20.

6. Conclusion

Datadog's Q2 performance showed continued growth in key financial metrics, including revenue and customer base. While beating Wall Street revenue and earnings expectations, the company achieved a solid increase in total customers, with significant growth in the ARR base, particularly among high-value customers. Platform adoption remained robust, marked by a steady increase in multi-product usage.

However, attention is drawn to the lowering of future guidance, reflecting a more conservative outlook for revenue growth in Q3 and the full fiscal year 2023. This adjustment aligns with the observation that Datadog's trailing 12-month Net Retention Rate (NRR) experienced a decline below 130% for the first time in over three years. This suggests a moderation in growth, possibly driven by existing customers' focus on optimising costs and enhancing efficiency.

With the share price up over 60% YTD before reporting earnings, Datadog traded at a forward P/E of 95. After selling off post earnings, Datadog still trades at a lofty forward P/E of 64.

The market reaction to lowering future guidance by 2% might first appear overblown. It is important to remember that when stocks are priced to perfection, even the smallest miss on growth expectations can cause short-term pain to investors.

So, are the dog days over? The answer for me is a comprehensive no. The long-term thesis is still very much intact. The full thesis from earlier this year is linked below for any new readers.

Rating: 3 out of 5. Meets expectations.

If you'd like to support the work of an independent analyst, you can buy me a coffee. The proceeds will contribute to covering the annual running costs of the newsletter.

Join the community of informed investors – subscribe now to receive the latest content straight to your inbox each week and never miss out on valuable investment insights.

If you found today's edition helpful, please consider sharing it with your friends and colleagues on social media or via email. Your support helps to continue to provide this newsletter for FREE!

Happy investing

Wolf of Harcourt Street

Contact me

Twitter: @wolfofharcourt

Email: wolfofharcourtstreet@gmail.com