MercadoLibre: 2026 Financial Model and Valuation Update

What is the fair value of MercadoLibre?

MercadoLibre (MELI) stock has had a brutal twelve months, falling 23%, compared to a 23% gain for the S&P 500 over the same period. That's a 46 percentage point swing in relative performance from where we stood this time last year, when MELI had delivered a 34% return against an 11% gain for the broader market.

The stock now sits more than 30% below its all-time high of $2,645, reached in June 2025. More surprisingly, it has fallen even as the underlying business has done something the market seemingly didn’t want: accelerate its growth.

So the key question this update needs to answer is simple: What is MELI actually worth, and has the market overreacted?

The starting point for this analysis is the FY2025 results together with the Q1 2026 earnings release, which gave us the first clear look at where margins are heading under new leadership. On 1 January 2026, founder Marcos Galperin stepped back to become Executive Chairman, handing the CEO role to Ariel Szarfsztejn, a company veteran since 2017. It’s worth keeping that transition in mind as we work through the margin discussion later.

ReviewSignal: Consumer-Review Data You Can Audit

On July 4, ReviewSignal pre-registered a call on Domino's ($DPZ) — built from

public consumer reviews (670,000+ across 18,600+ locations in 79 chains,

updated daily) — and locked it on a hashed, append-only public ledger.

It gets graded July 18. Domino's reports July 20. Hit or miss, it stays up.

No "AI predicts stocks" claims — just observable consumer-experience data and calls you can check yourself.

Want to look under the hood? The €49 Preview Data License is a 5-chain

sample pack with full methodology and coverage notes.

The Backdrop

Let's begin with what actually happened in 2025, because it wasn't what most models, mine included, had pencilled in. You can view my 2025 financial model below.

FY2025 revenue reached $28.9 billion, up 39% year over year, almost double the 24% growth my model had assumed at the start of the year. Q4 revenue alone increased 45% to $8.76 billion, and that momentum has carried into 2026. Q1 revenue reached $8.85 billion, up 49% year over year, marking MELI’s fastest growth since Q2 2022.

That’s the good news.

The trade-off has been margins.

Gross margin declined to 44.5% in FY2025 from 46% in 2024, primarily due to a lower free shipping threshold in Brazil and higher funding costs within the fintech business. Operating margin fell from 13% to 11% as MELI invested more aggressively in credit card issuance, first-party commerce, and logistics.

That pressure intensified in Q1 2026. Operating margin fell to 7%, a 600 basis point decline from the 13% reported a year earlier, while net margin dropped from 8% to 5%.

The biggest driver was the provision for doubtful accounts, MELI’s reserve for expected credit losses. This reached $3.09 billion in FY2025, or 11% of revenue, up from 9% the previous year. In Q1 alone, the provision more than doubled year over year, rising from $603 million to $1.24 billion, as the credit card portfolio nearly doubled to $14.6 billion.

Management has been clear that this is intentional. The company is willingly sacrificing near-term profitability to capture share in credit cards, expand free shipping, and continue building out its logistics network ahead of what it believes is a very long growth runway.

Whether that’s disciplined capital allocation or evidence that margin discipline is beginning to slip has become the central debate surrounding the stock. Barclays and Raymond James have reduced their price targets while maintaining Buy ratings. UBS downgraded the shares to Neutral, arguing that margin pressure could persist through 2027. Meanwhile, at least one well-known value investor, best known for The Big Short, reportedly built a position following the Q1 sell-off, believing the market is treating a cyclical margin trough as though it were a permanent impairment.

I don’t think you need to settle that debate to build a sensible valuation model. You simply need to make a reasonable assumption about how long margins remain under pressure and how much they eventually recover, then let the cash flows do the talking.

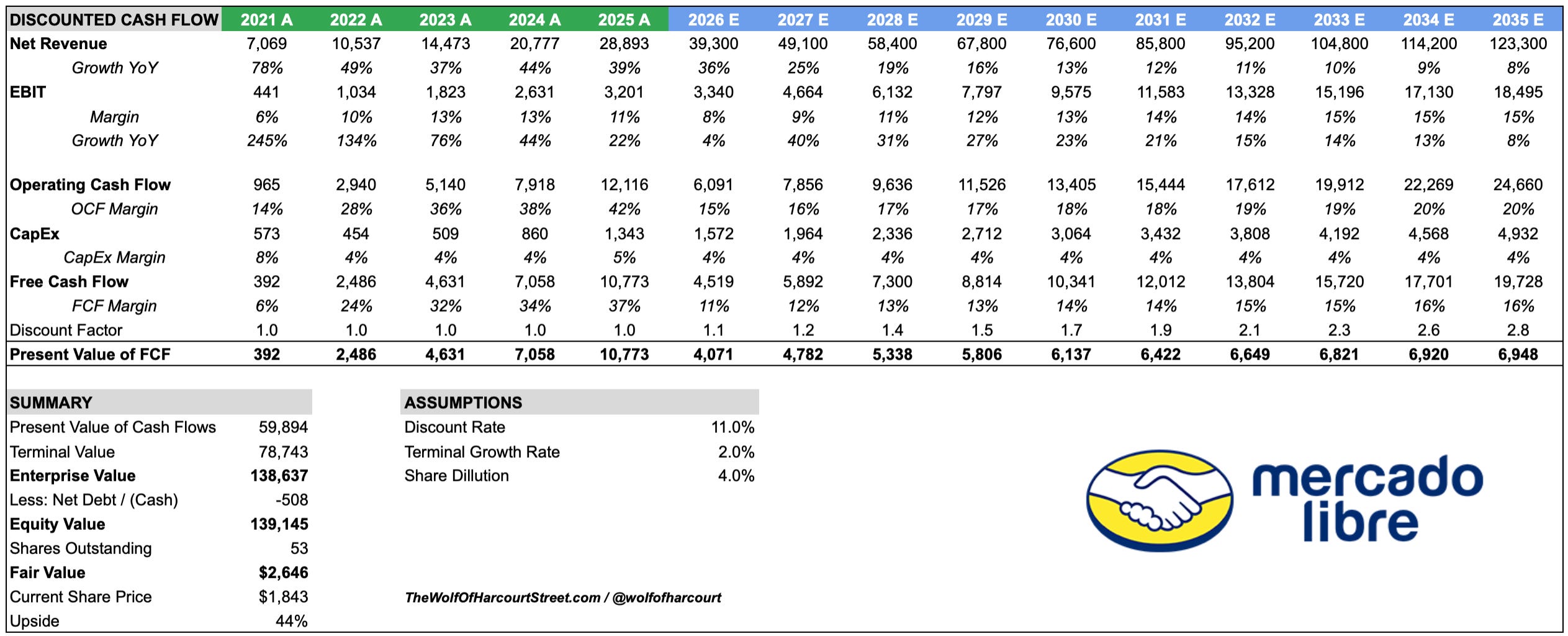

Discounted Cash Flow Analysis

Future cash flows are projected over ten years (2026 to 2035). One notable change from last year is the discount rate, which I’ve increased from 10% to 11%. MELI’s credit book has grown faster than its balance sheet cushion, funding costs have increased, and the FX and regulatory backdrop across Brazil, Mexico, and Argentina remains highly unpredictable. Together, those factors justify a higher risk premium. Terminal growth remains unchanged at 2%, still toward the lower end of the range given the long term currency devaluation risk across the markets where MELI operates.

Revenue

I project a 16% revenue CAGR from 2025 to 2035, identical to the assumption used in last year’s model over 2024 to 2034. That’s despite 2025 growth comfortably exceeding what I had originally forecast.

Growth is expected to slow from 36% in 2026 to 8% by 2035 as the revenue base compounds into the hundreds of billions and the law of large numbers begins to take effect. Even with that deceleration, the model still implies MELI roughly quadruples revenue over the next decade, reaching more than $120 billion by 2035.

The broader market opportunity continues to support that outlook. A joint Endeavor and MELI report published in early 2026 estimates Latin American e-commerce sales will reach $215 billion in 2026 alone, growing 1.5 times faster than the global average. Argentina, Brazil, and Mexico account for nearly 85% of regional volume. Meanwhile, PCMI’s longer term forecasts still point to the region’s e-commerce market surpassing $1 trillion by 2027. The structural growth story hasn’t changed. If anything, MELI’s 2025 results suggest it is playing out even faster than expected.

EBIT Margin

This is where the model differs most from last year’s version.

Previously, I assumed EBIT margin would remain at 13% through 2025 before expanding steadily to 20% by year ten. Instead, FY2025 came in at 11%, while Q1 2026 fell further to 7%.

Rather than fighting the trend, this model assumes EBIT margin bottoms at roughly 8% in 2026, broadly in line with the current run rate, before gradually recovering to 15% by 2035. That’s 5 percentage points below last year’s terminal assumption.

The downgrade is intentional. Management has signalled no near term margin recovery, while investments in the credit card business, first party commerce, and Brazil’s free shipping programme increasingly resemble a multi-year reinvestment cycle rather than a temporary headwind. I’d rather build a model that’s too conservative than one that needs to be walked back again next year.

Normalised Operating Cash Flow

The distortion I highlighted last year hasn’t disappeared. It’s become even larger.

Reported operating cash flow reached $12.1 billion in FY2025, representing an eye-catching 42% margin. However, that figure is even less useful as a measure of underlying cash generation because it’s inflated by the same accounting dynamic.

The provision for doubtful accounts is a non-cash expense recognised before actual credit losses occur, and it increased 66% year over year to $3.09 billion. Combined with the large working capital swings associated with the credit and payments businesses, reported operating cash flow increasingly reflects how quickly the credit portfolio is expanding rather than the underlying cash generation of the business.

Using the same adjustment methodology as last year, I estimate a normalised operating cash flow margin of roughly 19% for FY2025, essentially unchanged from the prior year’s normalised figure despite the much larger reported cash flow.

It’s also worth noting that MELI now reports its own stricter measure, Adjusted Free Cash Flow, which treats changes in the credit portfolio as a cash outflow. On that basis, FY2025 adjusted free cash flow was just $1.48 billion, reflecting approximately $6.7 billion of net credit portfolio growth, partially offset by $2.35 billion of third party fintech funding.

That approach is more conservative than the one used in my model. I view credit growth in the same way as the company’s broader operating investments, as reinvestment to support future growth rather than a permanent drag on cash generation, provided credit performance remains healthy.

Normalised operating cash flow margin is forecast to trough at roughly 15% in 2026 before recovering to 20% by 2035, below last year’s 25% terminal assumption, reflecting the more conservative margin outlook discussed above.

CapEx and Dilution

CapEx represented 4.6% of revenue in FY2025, or $1.33 billion on $28.9 billion of revenue, up from 4.1% the previous year. I assume a steady 4% CapEx margin throughout the forecast period, broadly consistent with recent history and with the fact that most of MELI’s logistics investment is recognised through operating expenses rather than capital expenditure.

Share dilution has remained minimal. Diluted share count ended FY2025 at roughly 50.7 million, essentially unchanged from 2024, while the company also repurchased a small amount of stock during the year.

That’s a materially better outcome than I assumed in last year’s model, which incorporated 5.4% cumulative dilution over the decade. I’ve reduced that assumption to 4% cumulative dilution, reflecting management’s demonstrated willingness to maintain a disciplined share count despite aggressively investing in the credit business.

Discounting these cash flows at an 11% discount rate, using a 2% terminal growth rate, produces the following valuation:

Present value of forecast free cash flow (2026 to 2035): $59.9 billion

Present value of terminal value: $78.7 billion (57% of enterprise value)

Implied enterprise value: $138.6 billion

Dividing by an estimated 52.6 million diluted shares in 2035, reflecting modest dilution over the forecast period, results in an intrinsic value of approximately $2,646 per share. Compared with MELI’s closing price of $1,843 on 15 July 2026, that implies 44% upside.

What Actually Changed From Last Year

It’s worth being explicit about the moving parts, because this year’s update landed in a very different place than a simple “roll the model forward” exercise would suggest.

Growth improved. Revenue grew 39% in 2025 versus my 24% assumption, while Q1 2026 revenue accelerated 49%, the fastest pace in four years.

Margins deteriorated faster than expected. EBIT margin fell to 11% in 2025 and 7% in Q1 2026, well below the flat 13%, then expanding trajectory I assumed a year ago.

The discount rate increased. I raised it from 10% to 11% to reflect a faster-growing, more heavily funded credit book, alongside persistent foreign exchange risk across the region.

Dilution assumptions improved. I reduced cumulative dilution from 5.4% to 4%, reflecting genuinely disciplined share count management.

Leadership changed. Ariel Szarfsztejn is now CEO, while Marcos Galperin has moved to Executive Chairman. It marks the first CEO transition in the company’s 27 year history, arriving at exactly the moment investors are most focused on capital allocation and margin discipline..

Netting all of that out, my fair value declined only marginally, from $2,749 to $2,646, despite the much stronger revenue trajectory. The margin downgrade and higher discount rate largely offset the growth upgrade.

To me, that’s the honest state of play. The bear case on margins is real, and I’ve tried to reflect that in the model rather than dismiss it. The bull case is that the market has taken the same margin story and knocked roughly 30% off the share price. Once you run the cash flows through a long-term valuation model, rather than reacting to a single quarter’s operating margin, that sell-off looks increasingly disproportionate.

Conclusion

The growth runway for MELI remains enormous. If anything, 2025 provided the clearest evidence yet that its addressable market is real rather than theoretical.

Latin American e-commerce is now on track to reach $215 billion in sales during 2026, growing roughly 1.5 times faster than the global average. The region is still expected to surpass $1 trillion in annual e-commerce volume by 2027. Yet online retail penetration remains only in the mid-teens as a percentage of total retail sales, roughly a decade behind the United States. At the same time, financial inclusion, particularly in Mexico, continues to lag Brazil, leaving Mercado Pago with a substantial runway to expand its payments and credit ecosystem.

The more difficult question this year isn’t whether the opportunity exists. It’s whether MELI’s aggressive investment in credit, free shipping, and logistics represents smart capital allocation that will look obvious in hindsight, or whether it signals a structural reset in the company’s long-term margin profile.

I’ve built this model to acknowledge that uncertainty. Rather than assuming margins return to 20%, I now model EBIT margins recovering to 15% by 2035. I’ve also increased the discount rate by a full percentage point versus last year’s analysis.

Even with those more conservative assumptions, the valuation still points to meaningful upside from today’s share price. To me, that suggests the market’s reaction to recent margin compression has gone further than the underlying cash flow mathematics justify.

MELI has spent more than two decades navigating currency crises, recessions, rising competition, and now its first ever CEO transition. That doesn’t guarantee the next decade will look the same, but it does make me reluctant to bet against a management team that has consistently proven capable of compounding value through periods of uncertainty.

If you'd like to support the work of an independent analyst, you can buy me a coffee. The proceeds will contribute to covering the annual running costs of the newsletter.

Join the community of informed investors – subscribe now to receive the latest content straight to your inbox each week and never miss out on valuable investment insights.

The Chat is a space designed to facilitate, real-time discussions, share knowledge and debate ideas with fellow investors. Join the conversation.

If you found today's edition helpful, please consider sharing it with your friends and colleagues on social media or via email. Your support helps to continue to provide this newsletter for FREE!

Happy investing

Wolf of Harcourt Street

Contact me

Twitter: @wolfofharcourt

Email: wolfofharcourtstreet@gmail.com