Nu Holdings: 2025 Financial Model and Valuation Update

What is the fair value of Nubank?

Nu Holdings (NU) stock has remained flat since its IPO in December 2021. During that time, its total customer base has grown 5x.

With the stock trading at its IPO price, what is NU’s fair value today, and is it a buy?

In this update, I present a revised financial model and fair value assessment. The starting point for this analysis is the 2024 financial results. I’ve already shared a detailed Q4 2024 earnings analysis, which can be accessed via the link below.

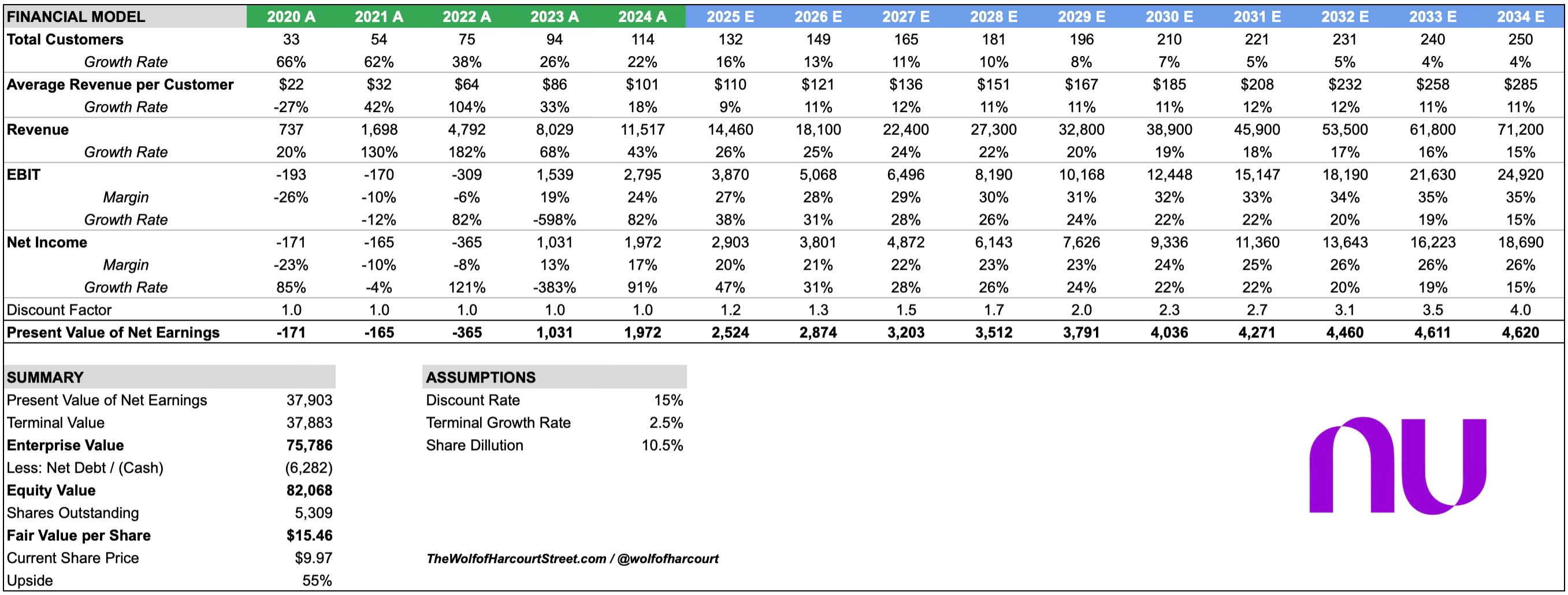

Financial Model

Unlike most companies I follow, NU’s reported cash flows are distorted because cash functions as both an input and output of the business. As a digital bank, NU is focused on growing its balance sheet by expanding its credit and loan portfolio. This expansion appears as negative cash flow, which can misrepresent the company’s financial health.

To address this, I’m using net income instead of free cash flow in the model. This approach simplifies the analysis while still capturing NU’s underlying profitability and operational efficiency.

Future earnings are projected over ten years using a 15% discount rate, reflecting NU’s exposure to credit risk and an emerging market risk premium. A terminal growth rate of 2.5% has been applied, acknowledging NU’s potential to benefit from inflation-driven interest rate increases that typically improve bank profitability.

Between 2019 and 2024, NU’s customer base grew at a CAGR of 42%. This forecast assumes total customers will reach 250 million by 2034, representing a CAGR of 8%. With Latin America's population expected to hit 700 million by 2034, NU would account for 36% of the total population, up from 17% today and just 3% five years ago.

Average revenue per customer (ARPU) is projected to nearly triple from $101 in 2024 to $285 in 2034. For comparison, incumbent banks in Brazil generate an ARPU about 4.5 times higher, leaving ample room for NU to grow its share of wallet and cross-sell more products. This, combined with customer growth, results in a projected revenue CAGR of 20% from 2024 to 2034.

The EBIT margin is forecast to rise from 24% in 2024 to 35% in 2034, benefiting from the operating leverage inherent in NU’s scalable model. Similarly, the net income margin is expected to improve from 17% to 26% over the same period. For context, Itaú Unibanco, Brazil’s largest bank, posted a 25% net income margin in 2024.

A 1% annual dilution rate has been assumed, consistent with recent trends, resulting in total shareholder dilution of approximately 10.5% over the forecast period.

Based on these assumptions, NU’s fair value is approximately $15.46 per share, implying a 55% upside compared to the $9.97 share price on 8 April 2025.

Conclusion

This analysis suggests that NU is undervalued, offering a high margin of safety. The forecast conservatively assumes NU will continue to gain market share, but still trails incumbent banks in ARPU and overall revenue market share. It also assumes NU’s net income margin only reaches levels broadly in line with traditional banks, despite its superior, asset-light digital model.

Key risks, such as credit exposure and emerging market volatility, are reflected in the 15% discount rate, adding further conservatism to the valuation.

One final point worth noting in light of recent U.S. tariff developments: NU offers exposure to an asset class unaffected by U.S. trade tensions. NU is exempt from these tariffs because it operates entirely outside the U.S. market. As a Brazil-based digital bank focused on Latin America, NU does not depend on the cross-border trade of physical goods, which are the primary target of recent tariffs.

If you'd like to support the work of an independent analyst, you can buy me a coffee. The proceeds will contribute to covering the annual running costs of the newsletter.

Join the community of informed investors – subscribe now to receive the latest content straight to your inbox each week and never miss out on valuable investment insights.

The Chat is a space designed to facilitate, real-time discussions, share knowledge and debate ideas with fellow investors. Join the conversation.

If you found today's edition helpful, please consider sharing it with your friends and colleagues on social media or via email. Your support helps to continue to provide this newsletter for FREE!

Happy investing

Wolf of Harcourt Street

Contact me

Twitter: @wolfofharcourt

Email: wolfofharcourtstreet@gmail.com

As a customer, I’m a big fan of Nubank’s service.

As an investor, I’m a big fan of David Vélez and the competitive advantages the bank has built.

That said, I do have some doubts about the growth projections - I think there are some structural barriers that might make it harder to replicate the business model in other Latin American countries. What's your take?

I’d argue you’re not considering the second order impacts of Tariffs. Mexico and Brazil are both among the biggest exporters to US…tariffs in general will harm both economies and therefore potentially impact NU