Welcome back to the Wolf of Harcourt Street Newsletter.

Every month, I'll provide you with an update on my portfolio, including all of the transactions, the current allocation, and my buy list. In addition, I'll share a recap of the articles you may have missed from the previous month.

10 AI-proof SaaS Stocks for 2026

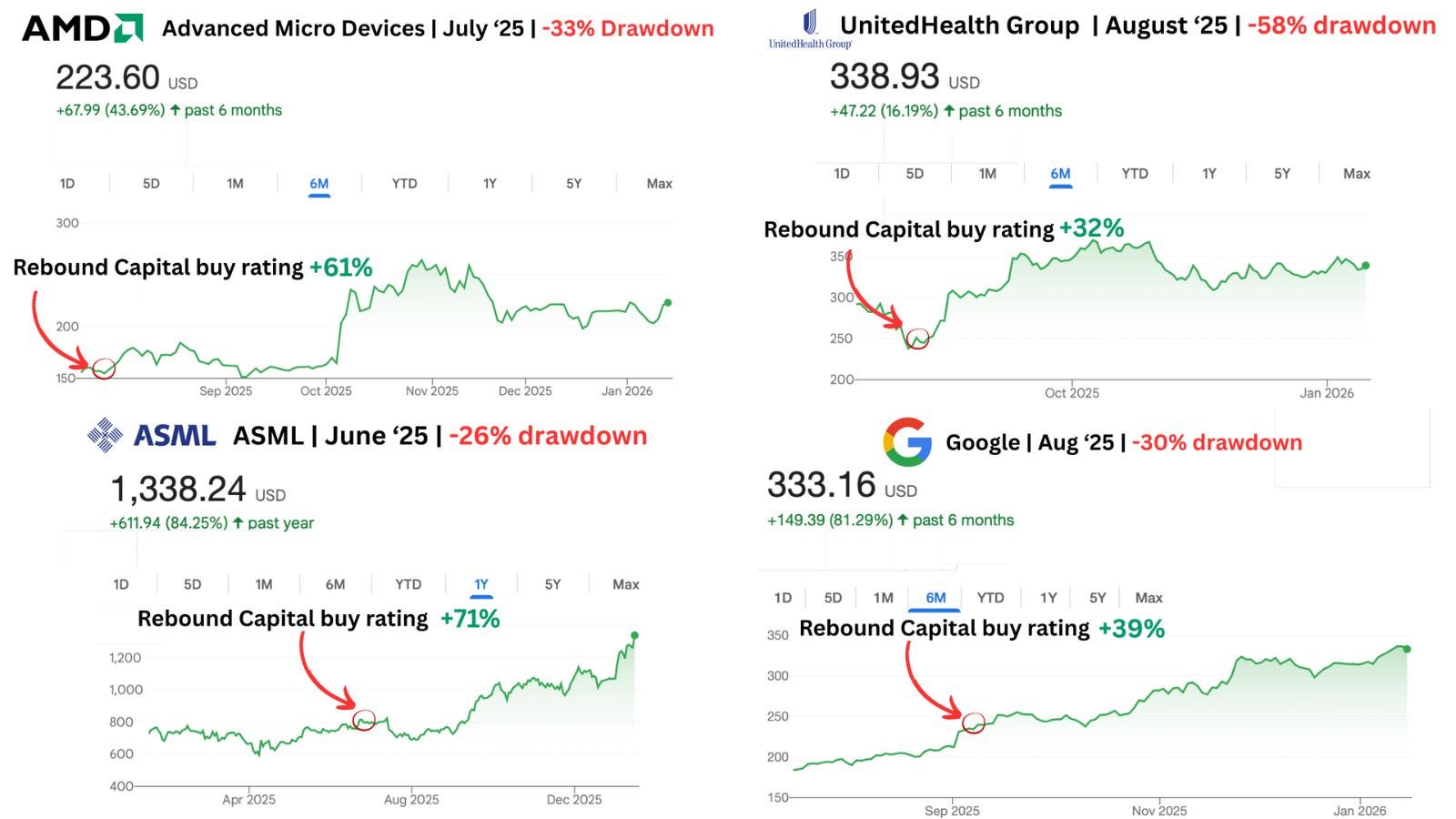

Meta once dropped 70%. Netflix: 50%. Amazon: 40%. Every investor had ruled them out, citing “the companies were done”.

But they all rebounded - Meta: 690%. Netflix: 540%. Amazon: 153%.

Every world-class company suffers deep drawdowns. Rebound Capital identifies high-quality companies undergoing drawdowns to capitalize on their eventual rebound.

Just last year, they identified ASML (up 58%), Google (up 40%), and AMD (up 61%) as ideal rebound prospects.

And now, SaaS is in peak pessimism due to AI-led disruption.

Rebound Capital has identified 10 AI-proof SaaS companies with deep moats in steep drawdowns.

Wolf of Harcourt Street readers can now unlock their exclusive 24-page AI-proof stock report for free!

Transactions

Evolution (EVO)

I sold my full position in EVO, which was just over 3% of the portfolio at the time of sale. This is a decision I had been sitting on for some time, as the thesis had broken down and my conviction had been fading. When the market presented more attractive opportunities elsewhere, I finally decided to act.

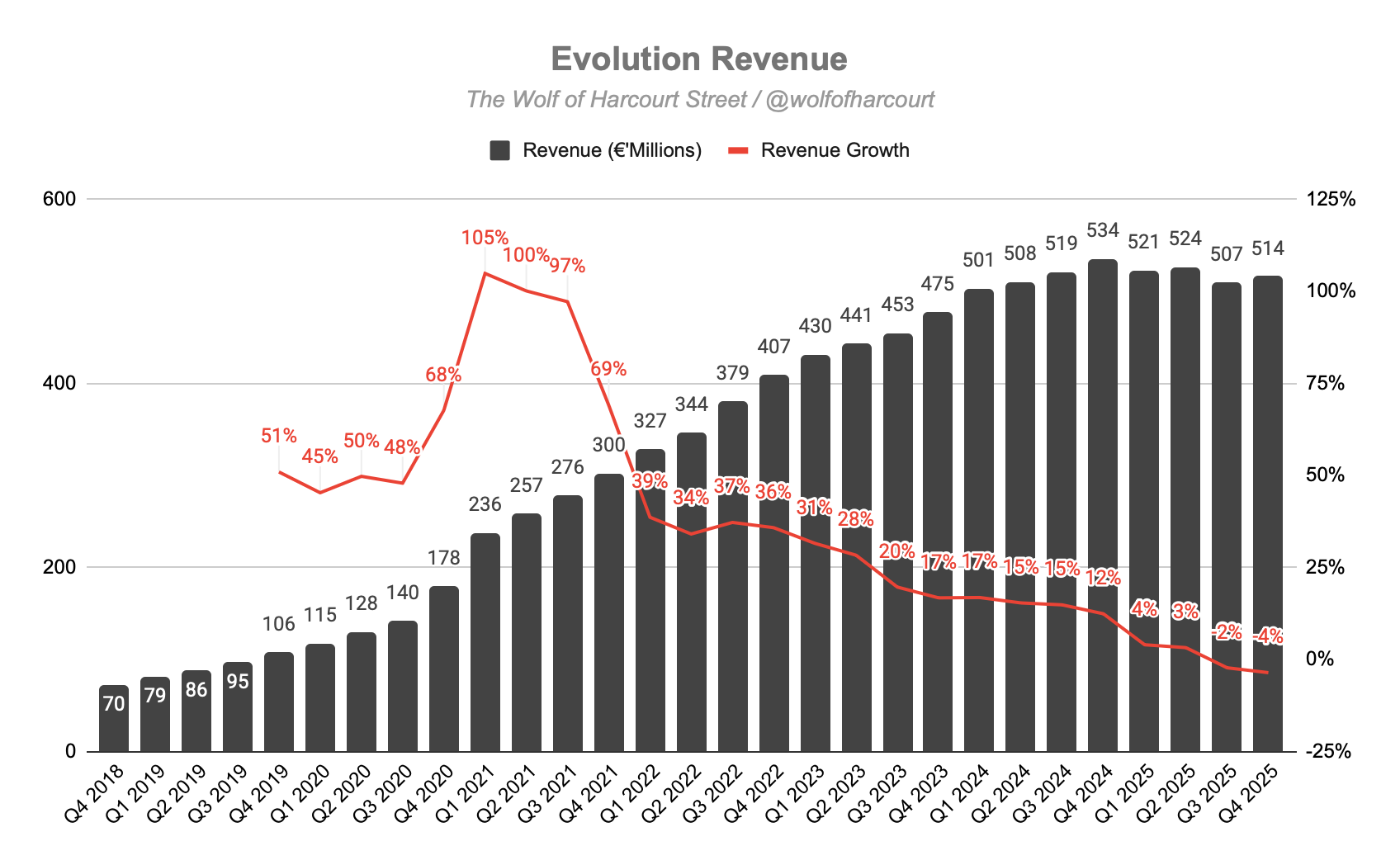

Before moving on, it’s important to go through the post-mortem. When I first published the EVO investment thesis in October 2023, the bull case felt almost self-evident. A business with 70% EBITDA margins, 26% revenue growth, durable network effects, and a near-unassailable position in live casino. It looked like a company you could hold for a decade.

The bull case rested on three pillars:

Structural moats. EVO’s advantage came from switching costs embedded in operator relationships, the network effects of the world’s largest live dealer studio network, and IP that competitors had repeatedly failed to replicate at scale.

Market growth as a tailwind. The global iGaming market was projected to grow from ~$73 billion in 2023 to over $127 billion by 2027. As the dominant B2B infrastructure layer, EVO was positioned to grow at least in line with the market and historically had grown well ahead of it.

Margin durability. A fixed-cost studio model with significant scalability meant each incremental game round carried extraordinary operating leverage. The margin profile was a feature of the business model.

None of these have disappeared entirely. But Q4 again showed that the growth engine has stalled, and in ways that aren’t easily reversed.

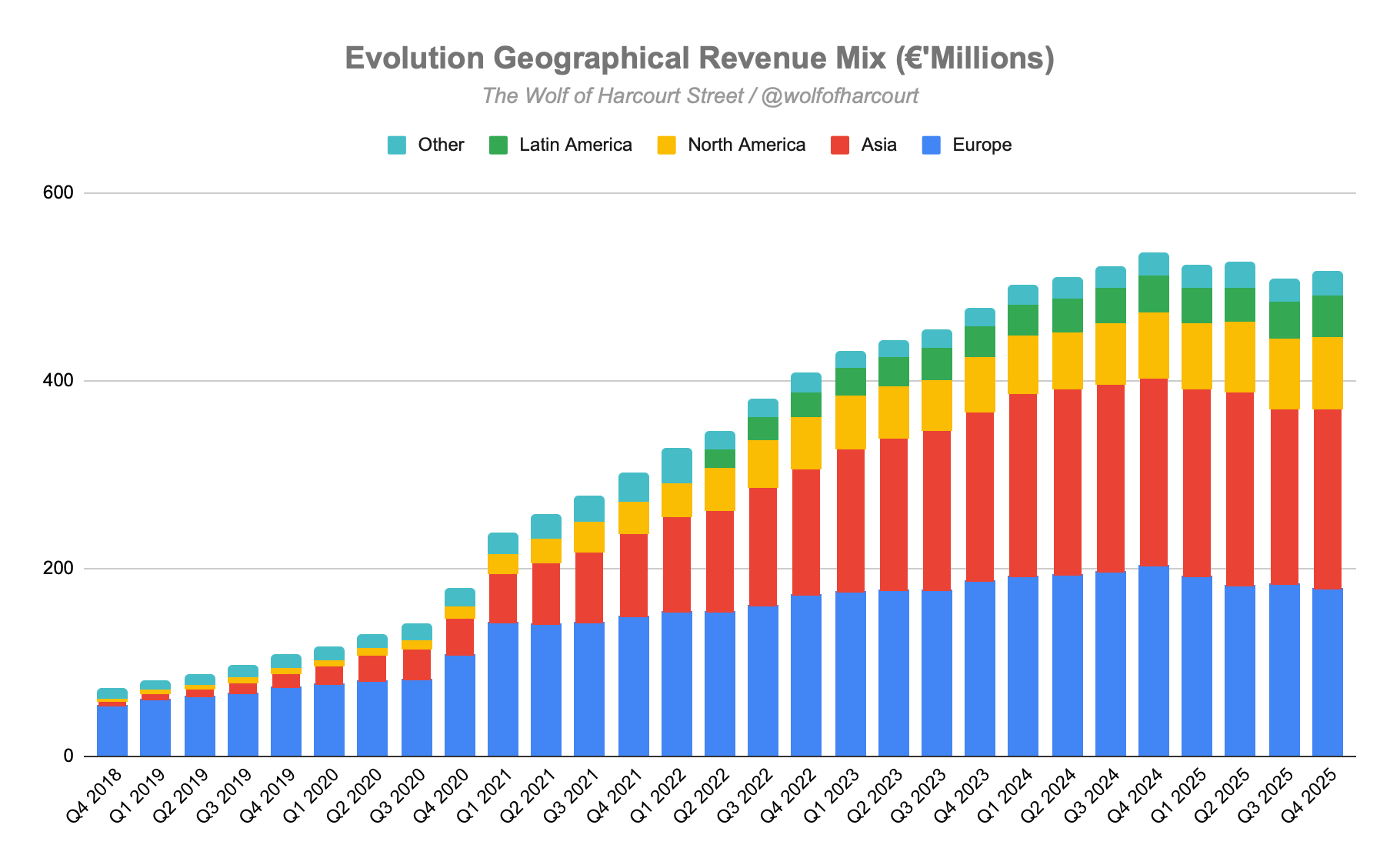

Europe is the problem that won’t go away. Channelisation is working against EVO. Ring-fencing measures across key European markets are shrinking the addressable pool, and management gave no credible timeline for reversal. This has been a headwind for several quarters.

Asia has a similar issue, but with a different root cause. Cybercrime, specifically the hijacking of Evolution’s video streams, has been a known issue since 2024. I gave management the benefit of the doubt when they described it as solvable. Twelve months later, the answer on the Q4 call was effectively “slow, methodical progress.”

Meanwhile, the growth that does exist in North America (+9%) and Latin America (+12%) comes with an important caveat. Combined, these regions still represent just over half of Asia’s revenue alone. Even at double-digit growth rates, they cannot offset the structural decline in EVO’s core markets within a reasonable time horizon.

There was one line in the Q4 earnings call that stood out. When asked what it would take for financial performance to finally match operational progress, CEO Martin Carlesund replied: “Just a stable environment. No more, no less.”

That was the tell. When a company’s re-acceleration depends primarily on external circumstances rather than controllable execution, the investment changes. You are no longer underwriting a business, you are underwriting a macro bet on regulatory stability in Europe and law enforcement effectiveness in Asia.

That is not the original thesis.

EVO remains a high-quality operator and will likely continue to generate significant cash and return it to shareholders. But the original thesis assumed double-digit growth with stable margins. Those assumptions are no longer valid, not in Europe, not in Asia, and not at a pace that the Americas can offset. For full transparency, I sold the entire position for an overall 41% loss.

Mercado Libre (MELI)

The capital freed up from EVO found a natural home. As I referenced in last month’s portfolio review, MELI sold off after Q4 2025 earnings on margin concerns. Operating margin compressed to 10% as the company leaned into fulfilment infrastructure, free shipping, and AI tooling across the platform.

I have seen this movie before with MELI: deliberate investment cycles that look like deterioration but turn out to be the foundation for the next leg of growth. When a business is growing revenue at 45%, adding 16 million new buyers in a single quarter, and building an advertising business growing 67%, a near-term margin dip is not a thesis breaker, it is the price of admission. The add was straightforward.

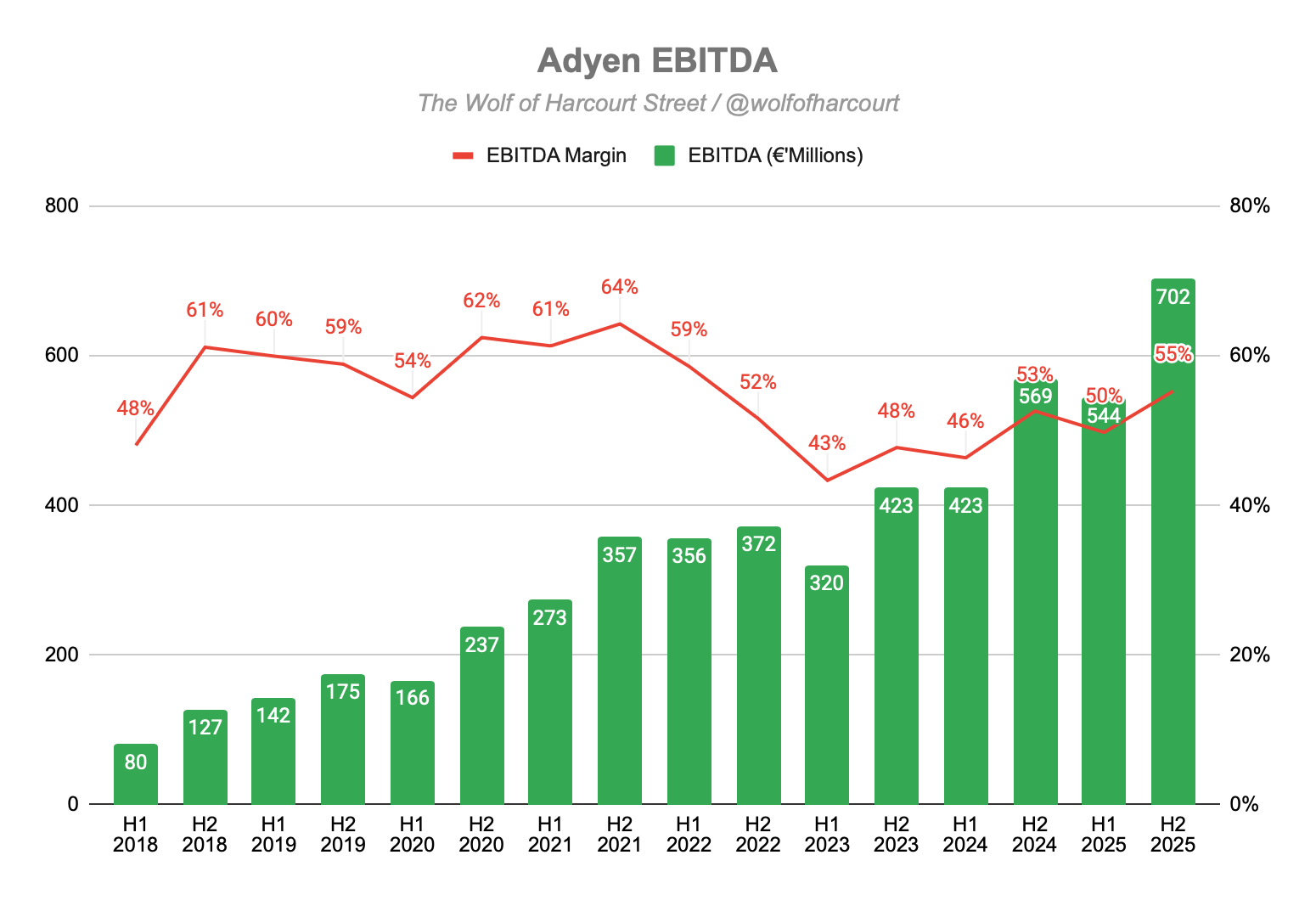

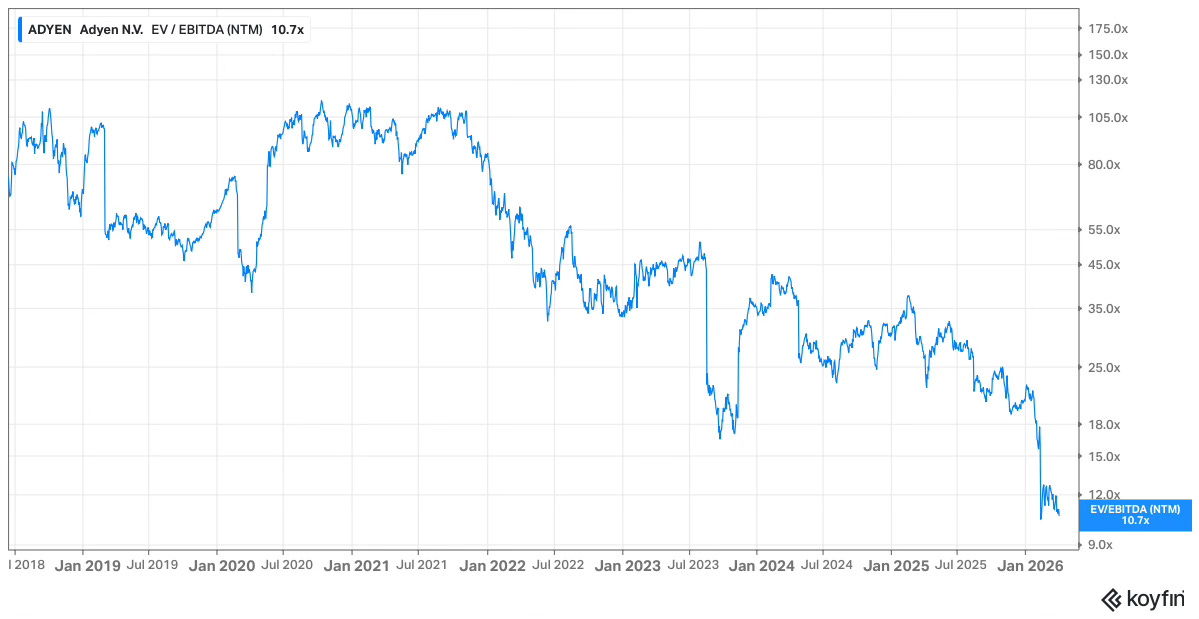

Adyen (ADYEN)

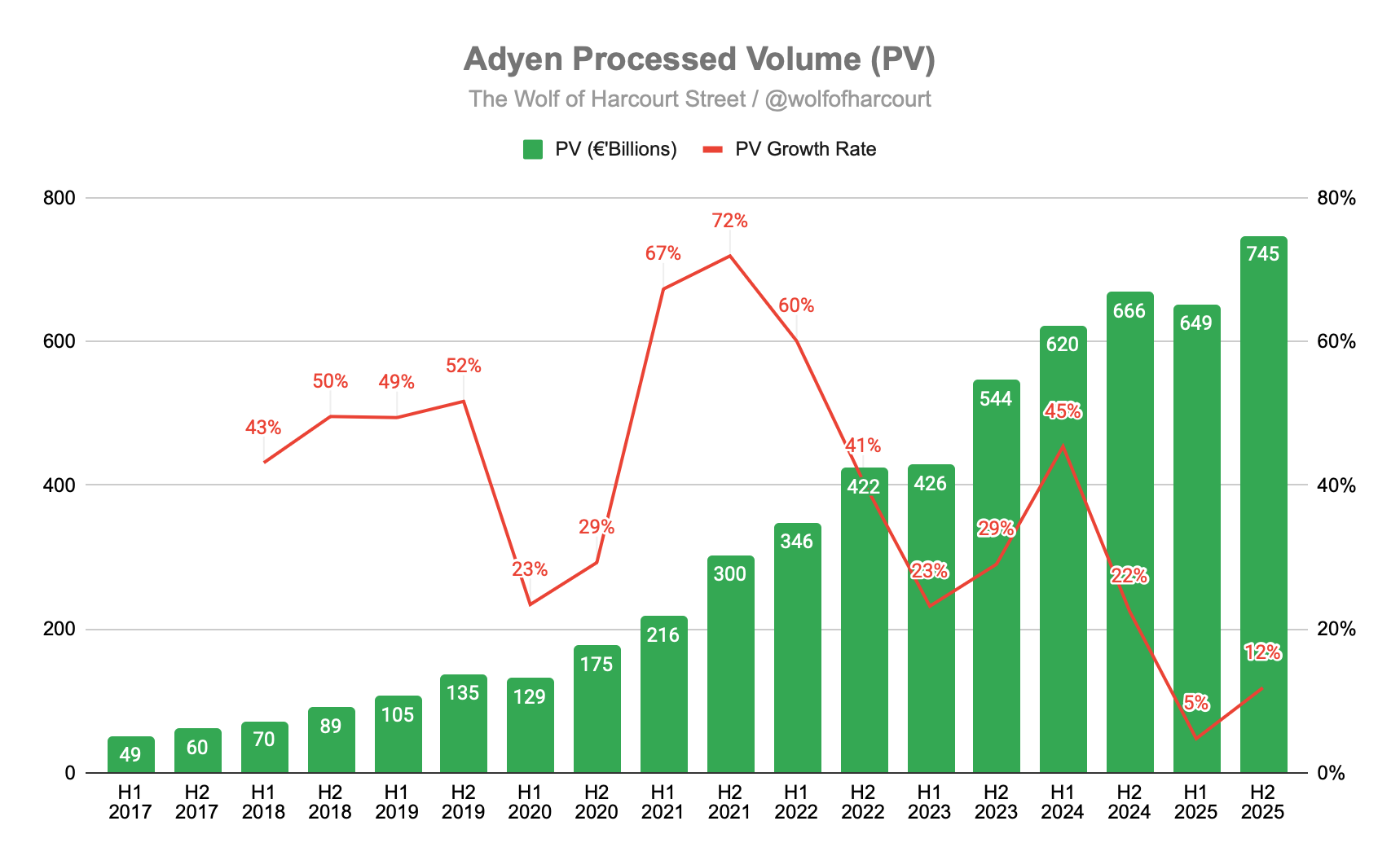

Adyen’s H2 2025 results were solid. Net revenue grew 21% on a constant currency basis, EBITDA grew 23%, and margin expanded to 55%, yet the market punished the stock by nearly 19%. The culprit was processed volume.

Full-year TPV grew just 8% versus 33% in 2024, with the Digital segment contracting 1% in H2, mainly due to the off-boarding of low-margin Cash App revenue. Currency headwinds and softer volumes from APAC-based merchants exposed to US tariff uncertainty also had a negative impact.

The market saw volume deceleration and sold first. I read it differently. Unified Commerce and Platform, the two segments that reflect Adyen’s strategic direction and long-term wallet share, both grew. EBITDA margin hit 53% for the full year, up from prior periods.

The land-and-expand model is working. Existing customers are expanding across geographies and sales channels, India is emerging as a meaningful new market, and embedded financial products, issuing, capital, and bank accounts, are inflecting. Management guided 20–22% net revenue growth for 2026 on a constant currency basis, underpinned by detailed customer conversations rather than top-down aspiration.

A forward EV/EBITDA of 11 on a business with >50% EBITDA margins, a clean balance sheet, and a durable competitive position in enterprise payments looks like an opportunity to me. I added accordingly.

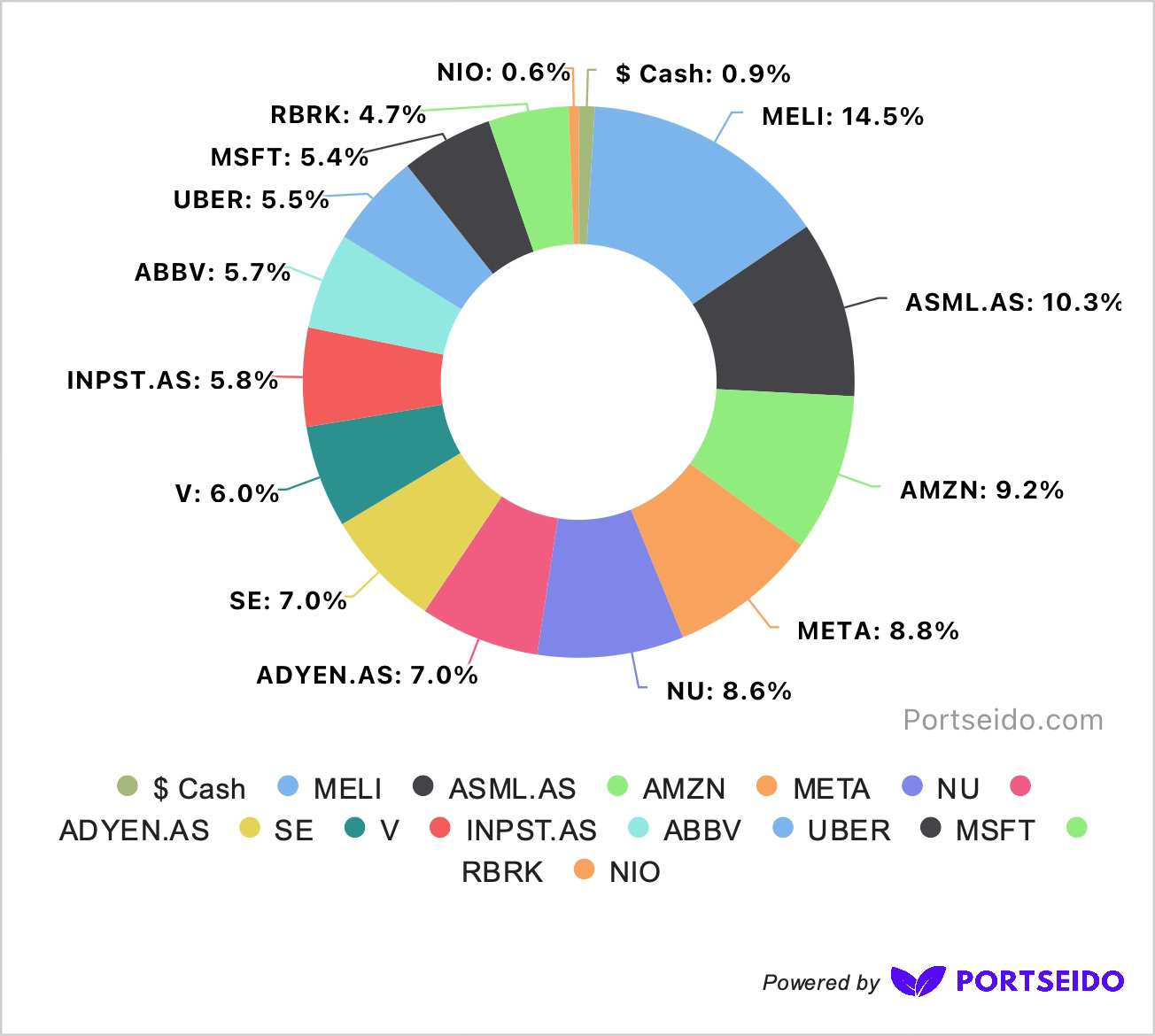

Allocation

I’ve been using Portseido to track my portfolio for years, and I highly recommend it. It consolidates all my transactions in one place, while its data visualisation and analytics capabilities guide my future decision-making and, ultimately, enhance my returns.

Sign up using my affiliate link here.

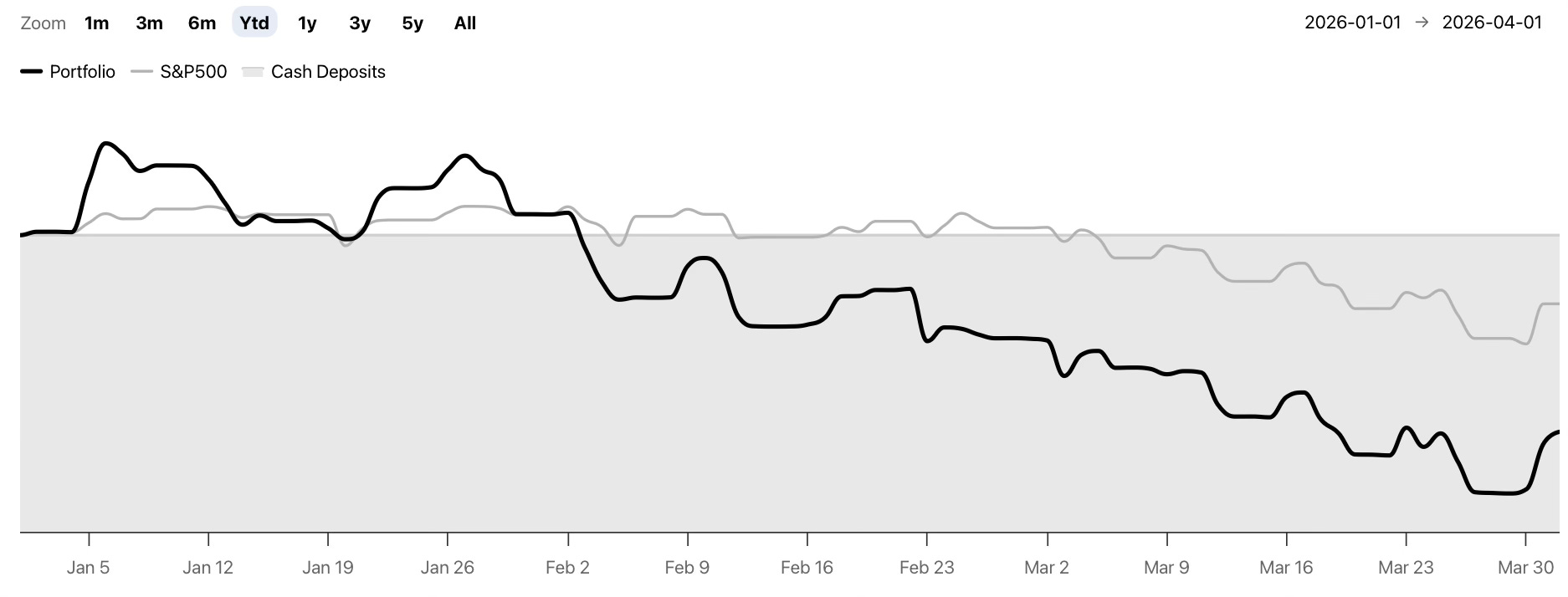

Performance

Q1: -13.2% vs. S&P -4.6%

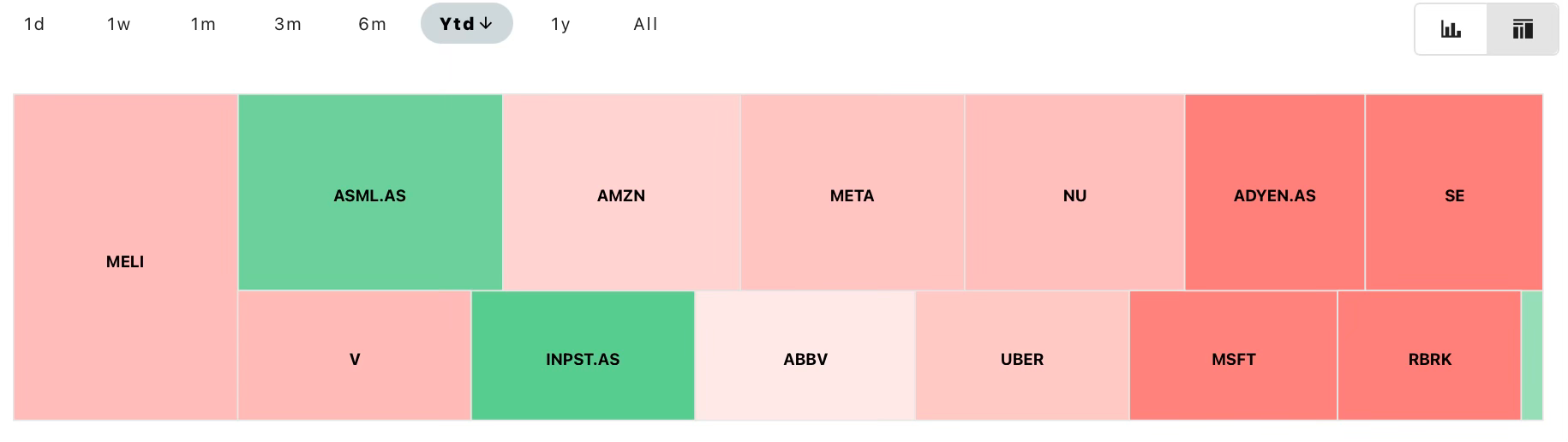

Top Contributors YTD:

INPST: +43%

ASML: +25%

NIO: +18%

Largest Detractors:

RBRK: -40%

SE: -39%

ADYEN: -37%

MSFT: -27%

V: -15%

Buy List

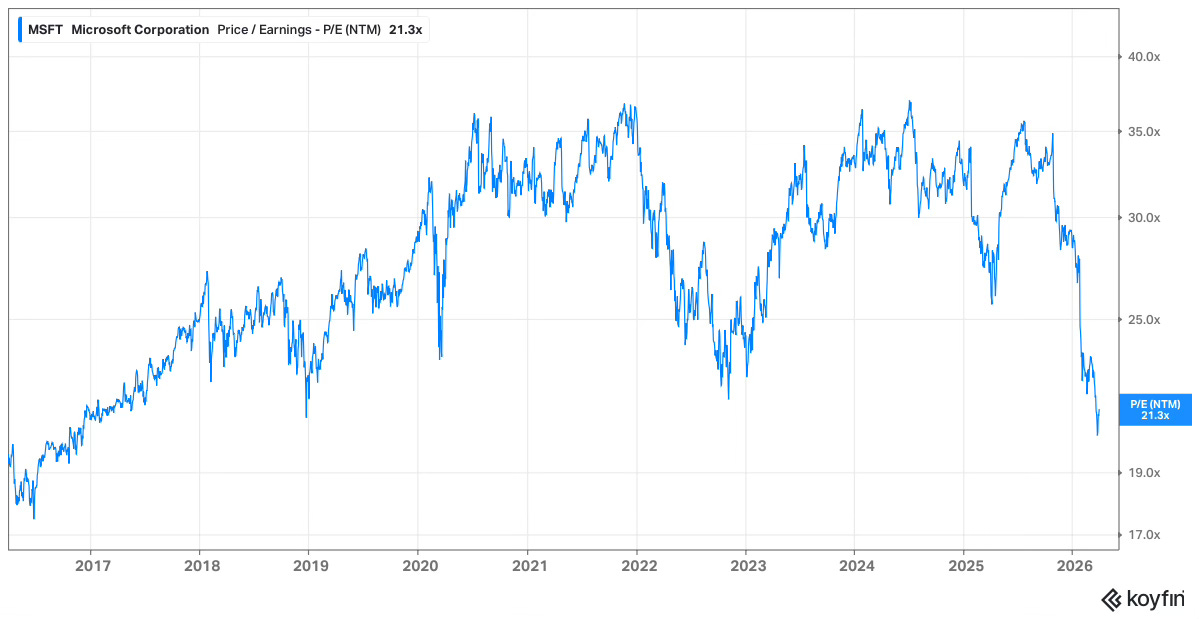

Microsoft (MSFT)

Microsoft is on the buy list for one reason above all others: Azure. During Q2 FY26, Azure grew 39%, with Q3 guided to 37–38%.

What makes the current setup interesting is valuation. Microsoft is trading at approximately 21x forward earnings, well below its five-year average of ~33x. A business compounding operating income at 21%, with Azure re-accelerating and a 47% operating margin, does not often trade at 21x earnings.

The bear case centres on CapEx, and it is a fair concern. Capital intensity is running at historically high levels as Microsoft builds infrastructure to meet backlog demand. But this is the same debate investors had when Amazon was pouring cash into AWS in its early years. Microsoft is now at its lowest earnings multiple since 2017. Even during the pandemic, the stock did not fall this low.

Visa (V)

I recently came across the Death by Claude tool, a SaaSpocalypse survival scanner, and it had this to say about Visa:

“Visa will be processing the payment for your funeral, your grandchildren's funerals, and the funerals of whatever sentient species replaces us. They survived the internet, crypto, Apple Pay, and now they'll survive Claude. They literally just sit between money and collect a toll - they're the final boss of capitalism."

Visa is probably one of the highest quality businesses in the world and is now trading close to the low end of its 10-year valuation range.

In Case You Missed It

Some of the articles you might have missed during the past month:

Final Words

The decision to sell EVO had been made some time ago, but I acted on it this month to free up cash and deploy it into what I believe are more attractive opportunities.

From a performance perspective, this was an ugly quarter and the worst for the portfolio since Q2 2022. From a concentration perspective, the portfolio is now down to 14 positions, which I am comfortable with. There are many opportunities in the market at the moment, both within the portfolio and on the watch list.

I deployed the majority of the EVO proceeds but still have almost 1% in cash. While tensions in the Middle East are having very real impacts on lives and markets, these periods often create some of the best opportunities in equities.

If you'd like to support the work of an independent analyst, you can buy me a coffee. The proceeds will contribute to covering the annual running costs of the newsletter.

Join the community of informed investors – subscribe now to receive the latest content straight to your inbox each week and never miss out on valuable investment insights.

The Chat is a space designed to facilitate, real-time discussions, share knowledge and debate ideas with fellow investors. Join the conversation.

If you found today's edition helpful, please consider sharing it with your friends and colleagues on social media or via email. Your support helps to continue to provide this newsletter for FREE!

Happy investing

Wolf of Harcourt Street

Contact me

Twitter: @wolfofharcourt

Email: wolfofharcourtstreet@gmail.com

Adyen & Meli are great here. Been buying both the past three months as well

Thanks for the updates. I have been waiting for an opportunity to buy Adyen and this feels a decent opportunity. Glad you concur!

Curious re RBRK not being added to / on the buy watchlist? Is this just driven by position sizing or something else? Thank you!