Welcome back to the Wolf of Harcourt Street Newsletter.

Every month, I'll provide you with an update on my portfolio, including all of the transactions, the current allocation, and my buy list. In addition, I'll share a recap of the articles you may have missed from the previous month.

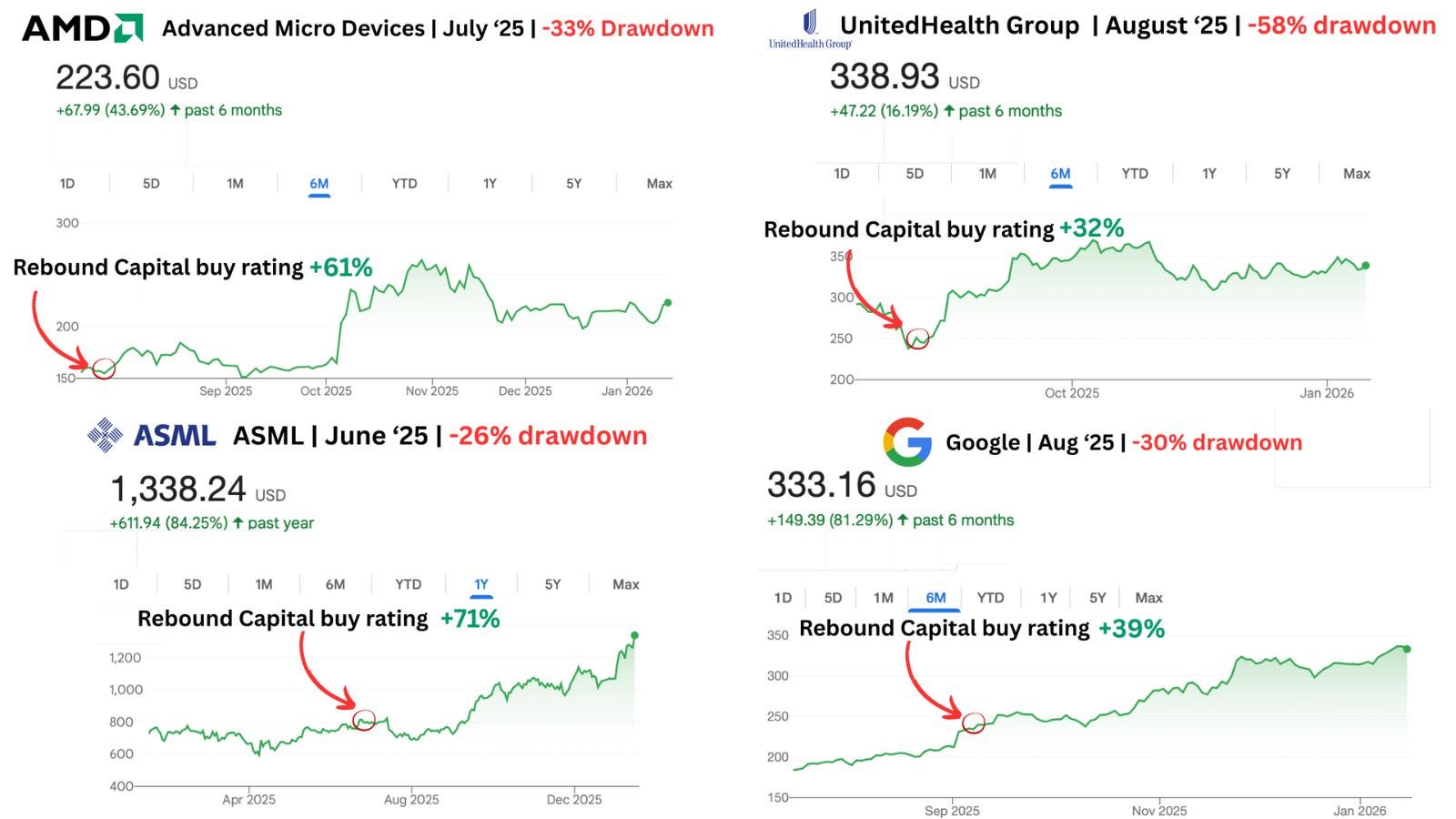

Top 10 Rebound Stocks for 2026

Meta once dropped 70%. Netflix: 50%. Amazon: 40%. Every investor had ruled them out, citing “the companies were done”.

But they all rebounded - Meta: 690%. Netflix: 540%. Amazon: 153%.

Every world-class company suffers deep drawdowns. Rebound Capital identifies high-quality companies undergoing drawdowns to capitalize on their eventual rebound.

Just last year, they identified ASML (up 58%), Google (up 40%), and AMD (up 61%) as ideal rebound prospects. The Wolf of Harcourt Street readers can now unlock their exclusive 25-page report on the top 10 rebound opportunities for 2026 for free!

Transactions

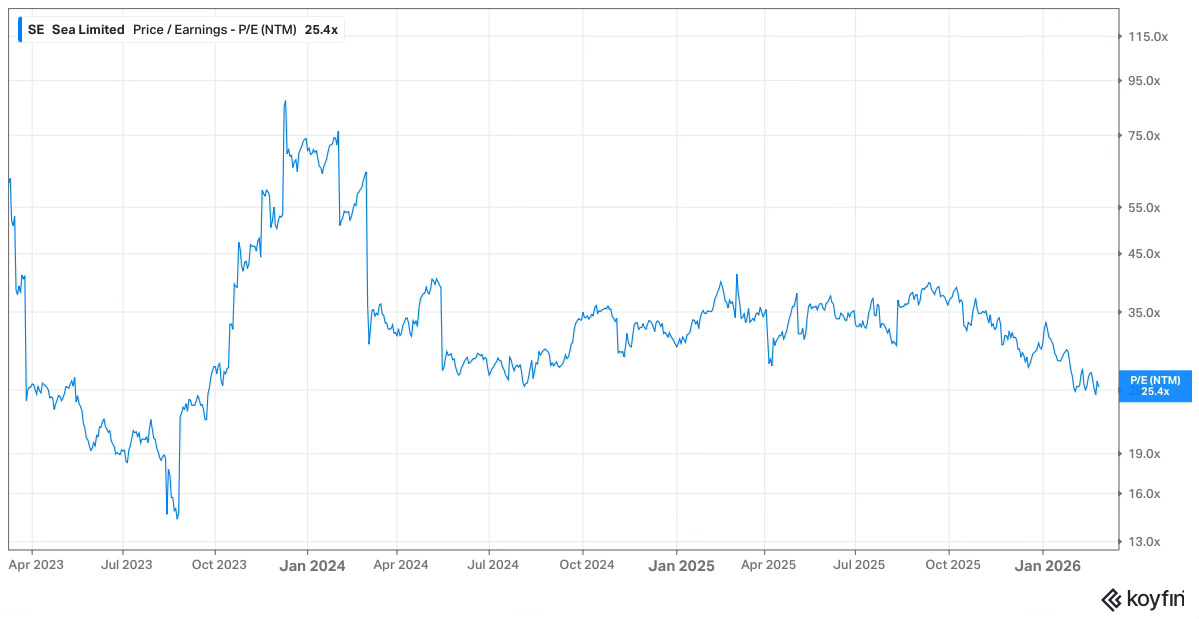

Sea Limited (SE)

I executed the buy decision in SE that I flagged in last month’s portfolio review. The stock continues to face pressure, despite being largely insulated from the AI disruption narrative. However, the underlying fundamentals remain as strong as ever.

Even more compelling, this growth business now trades at just 25 times forward earnings.

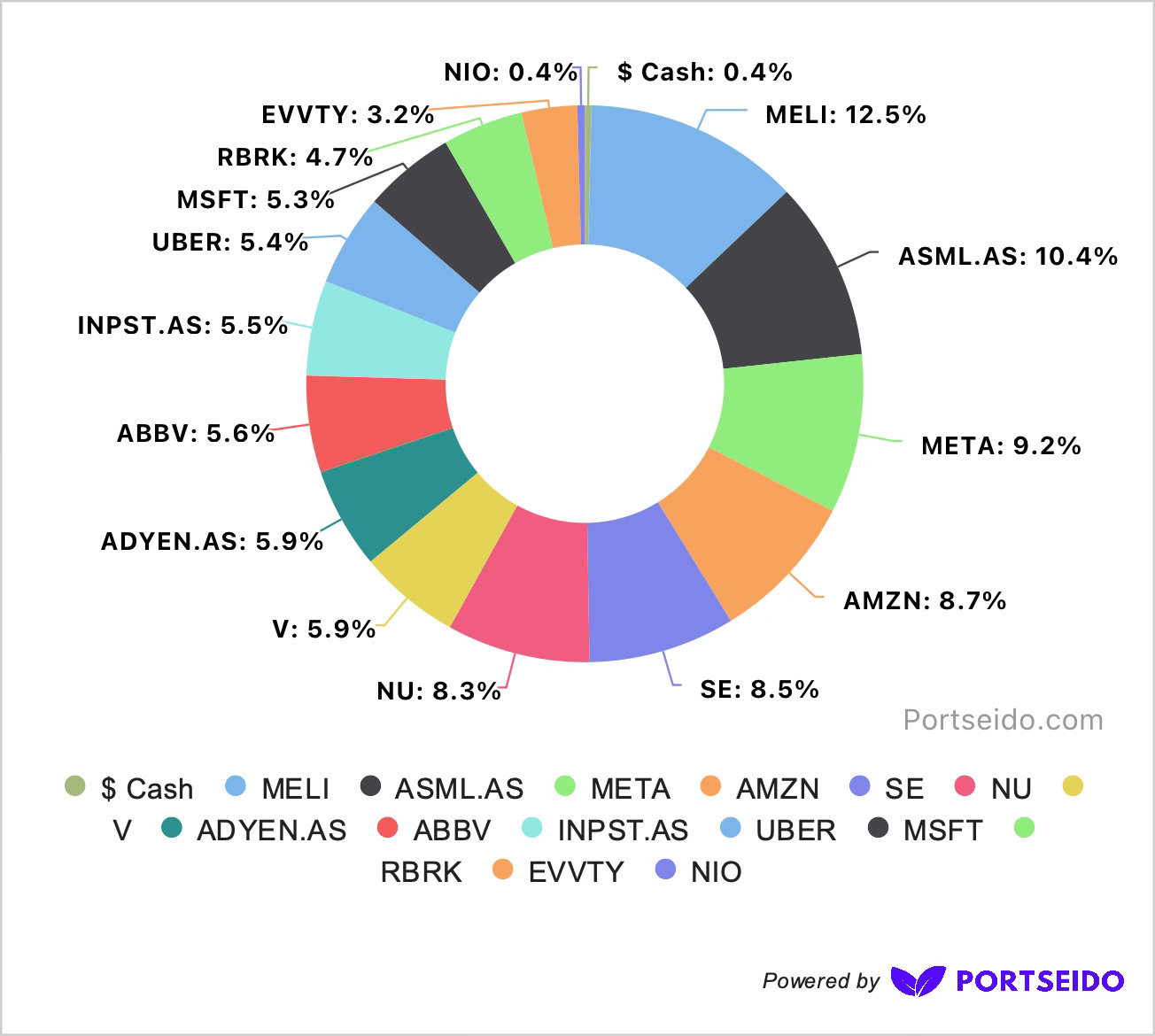

Allocation

I’ve been using Portseido to track my portfolio for years, and I highly recommend it. It consolidates all my transactions in one place, while its data visualisation and analytics capabilities guide my future decision-making and, ultimately, enhance my returns.

Sign up using my affiliate link here.

Buy List

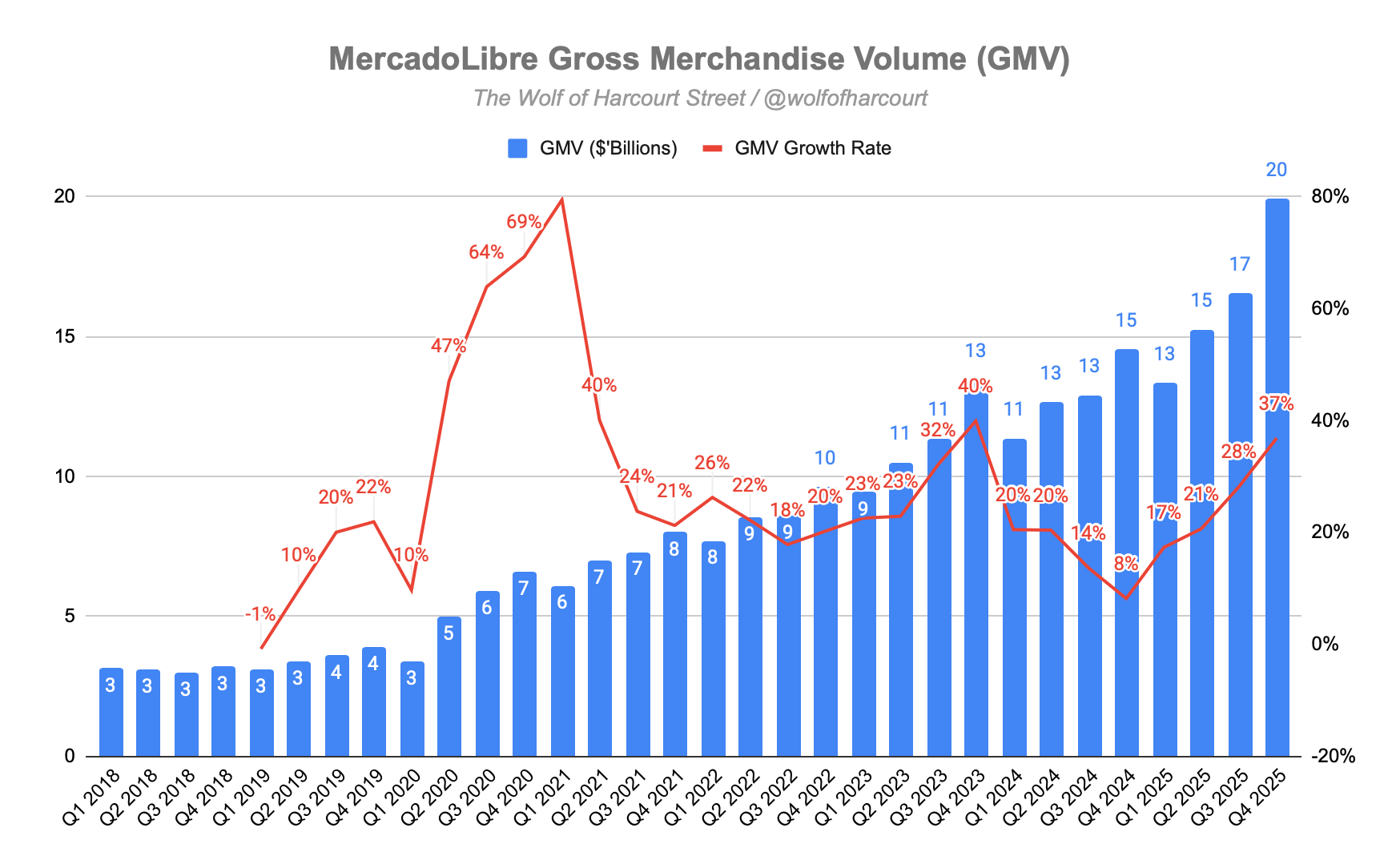

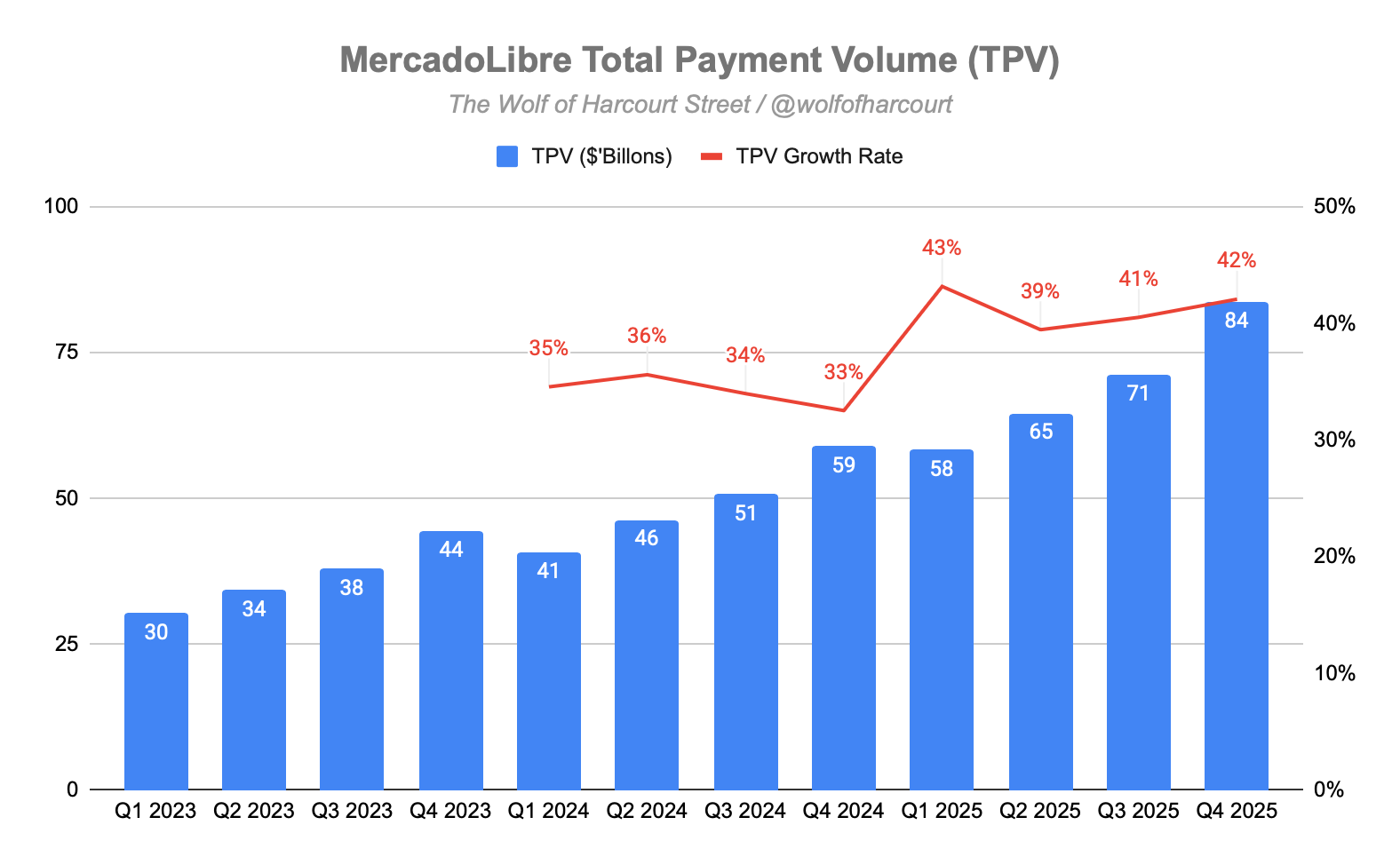

Mercado Libre (MELI)

My largest holding reported earnings this week and delivered another exceptional quarter, with revenue growing 45% year over year and comfortably beating expectations.

Long term readers will know that MELI does not issue guidance. As a result, Wall Street analysts have a poor track record forecasting its results. This quarter was no different. Earnings per share came in below estimates because management chose to invest aggressively for long term growth at the expense of short term profitability.

That is exactly what you want to see.

When a business has a vast market opportunity and a long reinvestment runway, it should be reinvesting as much as possible. I repeat this every quarter, but the message remains the same. The key performance indicators continue to validate the strategy, and I will be looking to make my largest position even larger.

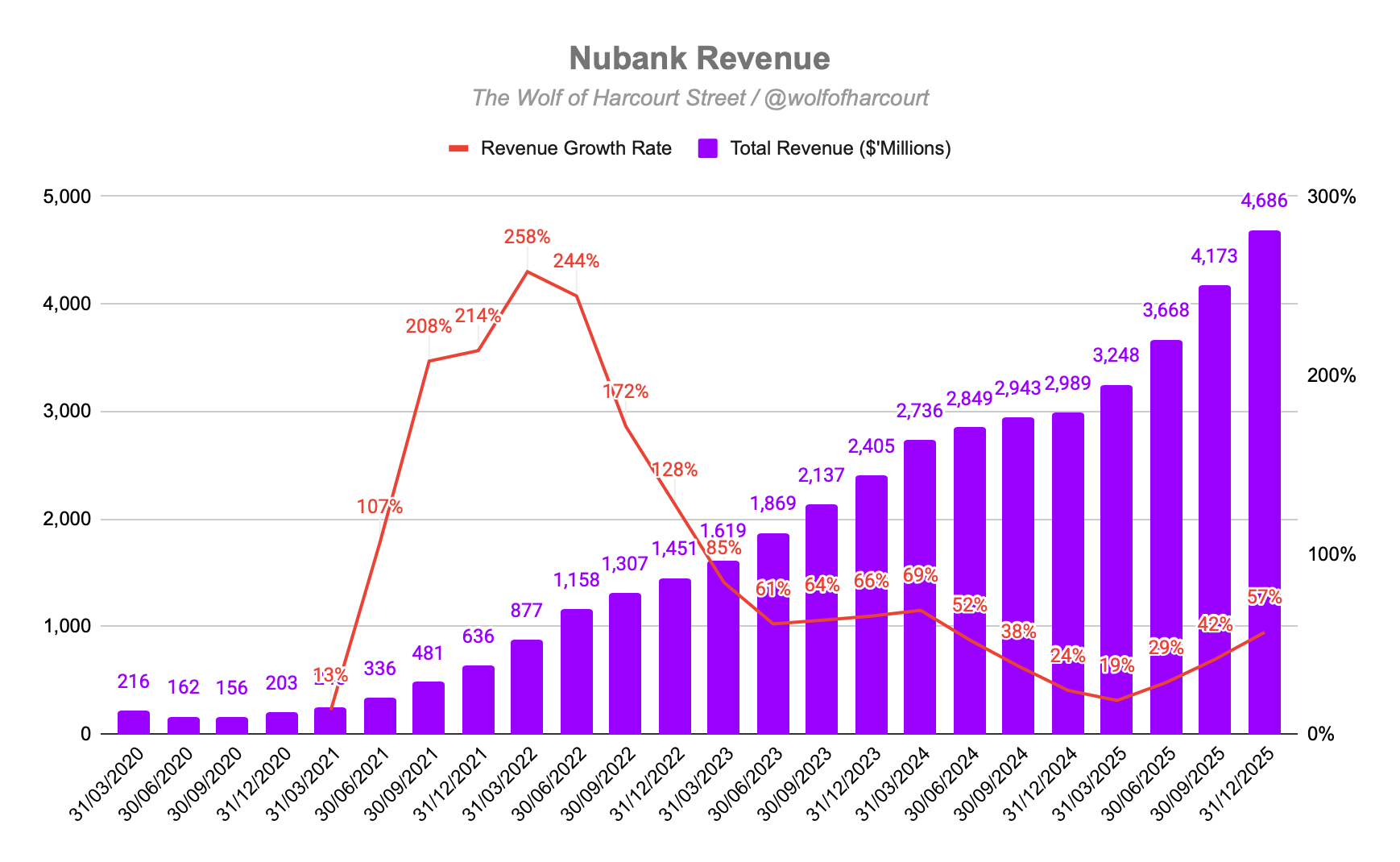

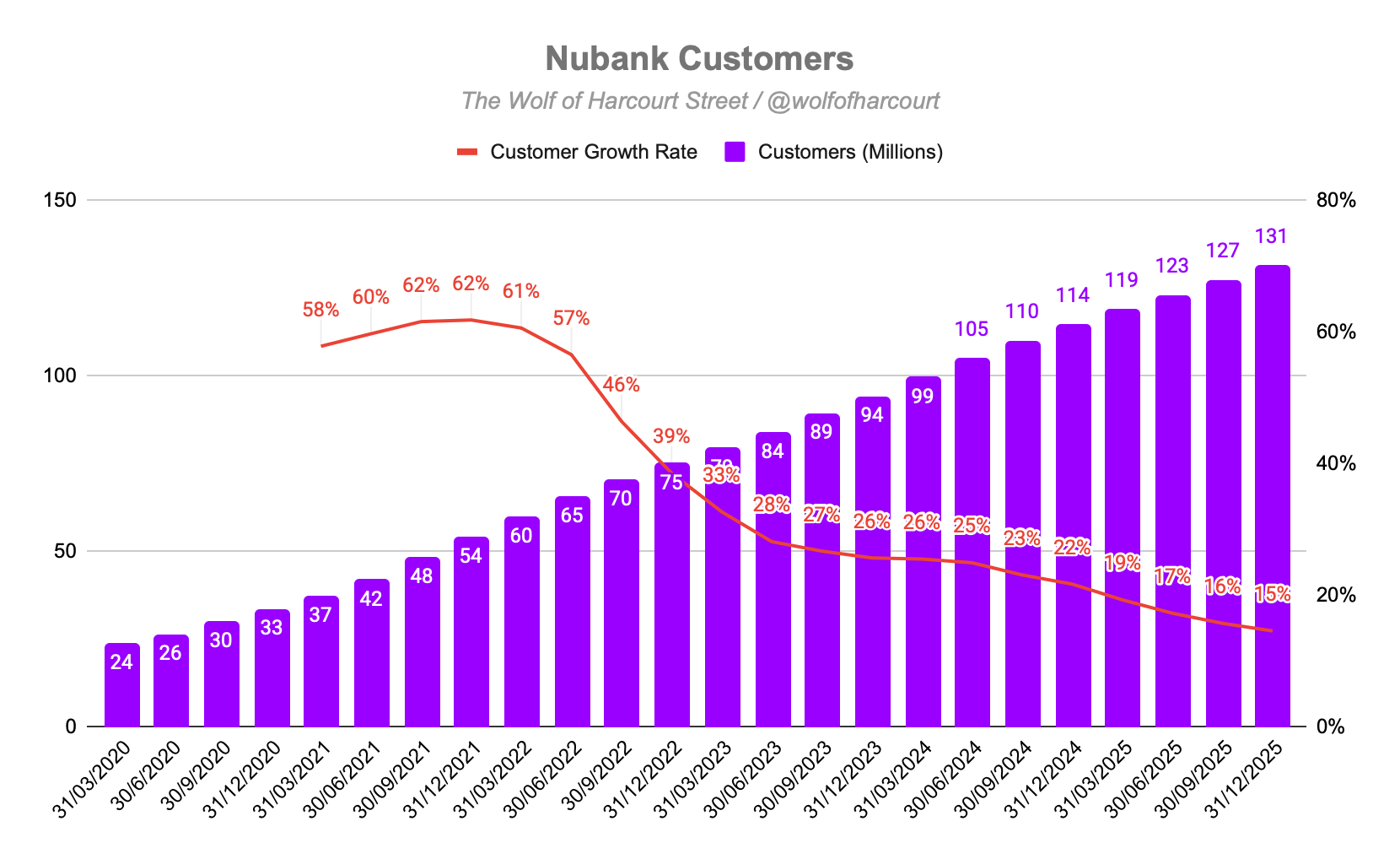

Nubank (NU)

NU also reported a strong quarter and, similarly, was punished by the market. Revenue beat estimates, with growth accelerating for the third consecutive quarter, marking the fastest growth rate since Q1 2024.

Despite its scale, NU continues to add roughly 4 million customers per quarter. Most of that growth still comes from Brazil, even though Mexico and Colombia are growing faster on a relative basis.

Importantly, nearly half of NU’s customer base joined within the past three years. Even so, average revenue per active customer, ARPAC, reached a record $15. That is already 19 times its cost to serve, before considering increased wallet share and monetisation as cohorts mature.

Customers who have been with NU for eight years generate ARPAC of $30.20. As the newer cohorts age, ARPAC should naturally expand.

In a previous article, I modelled a credible path for NU to triple revenue by 2030 from its existing customer base alone. That thesis is steadily playing out. I recommend revisiting that piece if you missed it.

In Case You Missed It

Some of the articles you might have missed during the past month:

Final Words

Investing is often described as an art rather than a science. Nothing captures that better than the discipline of doing nothing.

The past month has been highly volatile, particularly across technology, software, and payments. Yet it has been one of my least active months in some time. That has been intentional. I avoid emotional decisions and prefer to let the dust settle before acting.

I am currently contemplating two potential sales:

Evolution (EVO)

The company reported another disappointing quarter. It was a humbling reminder that situations can deteriorate further than expected.

As I acknowledged in my 2025 Annual Report, holding despite clear fundamental decline has been one of my larger mistakes. My conviction has faded. It is now a question of when, not if, I sell.

InPost (INPST)

Earlier this month, an offer was tabled to take INPST private at €15.60 per share. If completed, this would be deeply disappointing. It would mark the second time the company has gone private, and in both cases minority shareholders would bear the cost.

CEO Rafal Brzoska would see his ownership increase from 13% to 16%, which speaks to where incentives lie. Leverage has been cited as the rationale, but the alignment is clear.

With the current share price around €15.20, the remaining upside is roughly 2.5%. This could ultimately become a forced sale outside my control.

If you'd like to support the work of an independent analyst, you can buy me a coffee. The proceeds will contribute to covering the annual running costs of the newsletter.

Join the community of informed investors – subscribe now to receive the latest content straight to your inbox each week and never miss out on valuable investment insights.

The Chat is a space designed to facilitate, real-time discussions, share knowledge and debate ideas with fellow investors. Join the conversation.

If you found today's edition helpful, please consider sharing it with your friends and colleagues on social media or via email. Your support helps to continue to provide this newsletter for FREE!

Happy investing

Wolf of Harcourt Street

Contact me

Twitter: @wolfofharcourt

Email: wolfofharcourtstreet@gmail.com

Good stuff

I have made $MELI my biggest position at the end of last year (it was around 35% back then). Even though the stock is slightly down now I am just so relaxed with this company, which is a really good sign in terms of conviction imo. I even consider to buy more, it’s just such an exceptional company.