Welcome back to the Wolf of Harcourt Street Newsletter.

Every month, I'll provide you with an update on my portfolio, including all of the transactions, the current allocation, and my buy list. In addition, I'll share a recap of the articles you may have missed from the previous month.

Top 10 AI-proof SaaS Stocks

Constellation: -47%. ServiceNow: -55%. Figma: -81%.

Everyone is now expecting vibe-coded solutions to replace legacy companies with tens of thousands of employees and millions of customers. This is what peak pessimism looks like.

The market is wrong. Under the hood, a few of these “AI victims” are accelerating revenue with AI. We now have a brief moment where sentiment is overshadowing fundamentals.

Rebound Capital has spent months identifying these software beneficiaries — what went wrong, how they hold up against AI, and their current valuation — all in a 33-page, 5,000-word PDF.

Wolf of Harcourt Street readers can now unlock this report for free!

Transactions

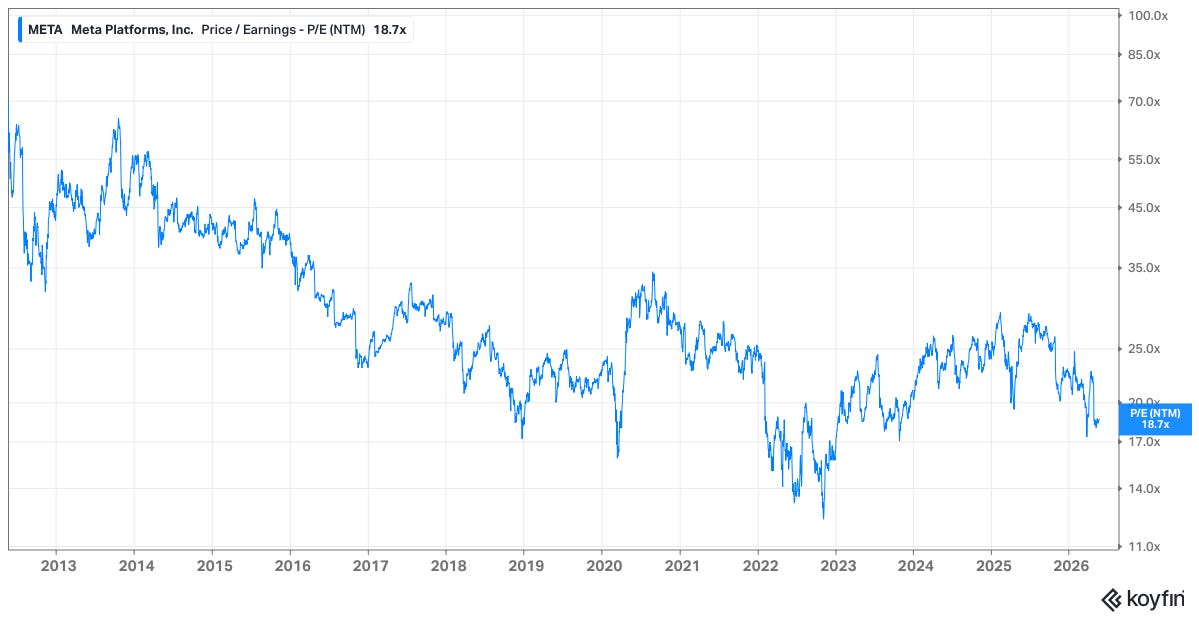

META (META)

I added to my META position for the second consecutive month. At current levels, I believe it is the best value opportunity within the Mag 7, trading at roughly 18x forward earnings despite a very attractive long-term growth outlook

As I have mentioned previously, AI is already driving tangible results across the core advertising business. Recommendation improvements are increasing time spent on platform, video engagement continues to rise, and better ad targeting is supporting stronger monetisation.

What remains underappreciated, in my view, is the flexibility embedded within META’s AI strategy. Mark Zuckerberg has repeatedly acknowledged that the company may ultimately be overbuilding AI infrastructure, but views this as a necessary risk worth taking. Even in that scenario, META can materially reduce future CapEx while still retaining years of excess data centre capacity. Given how constrained compute remains globally, that capacity could potentially be monetised through third-party demand.

The asymmetry here is compelling. The downside risk appears manageable relative to the scale of the potential AI monetisation opportunity.

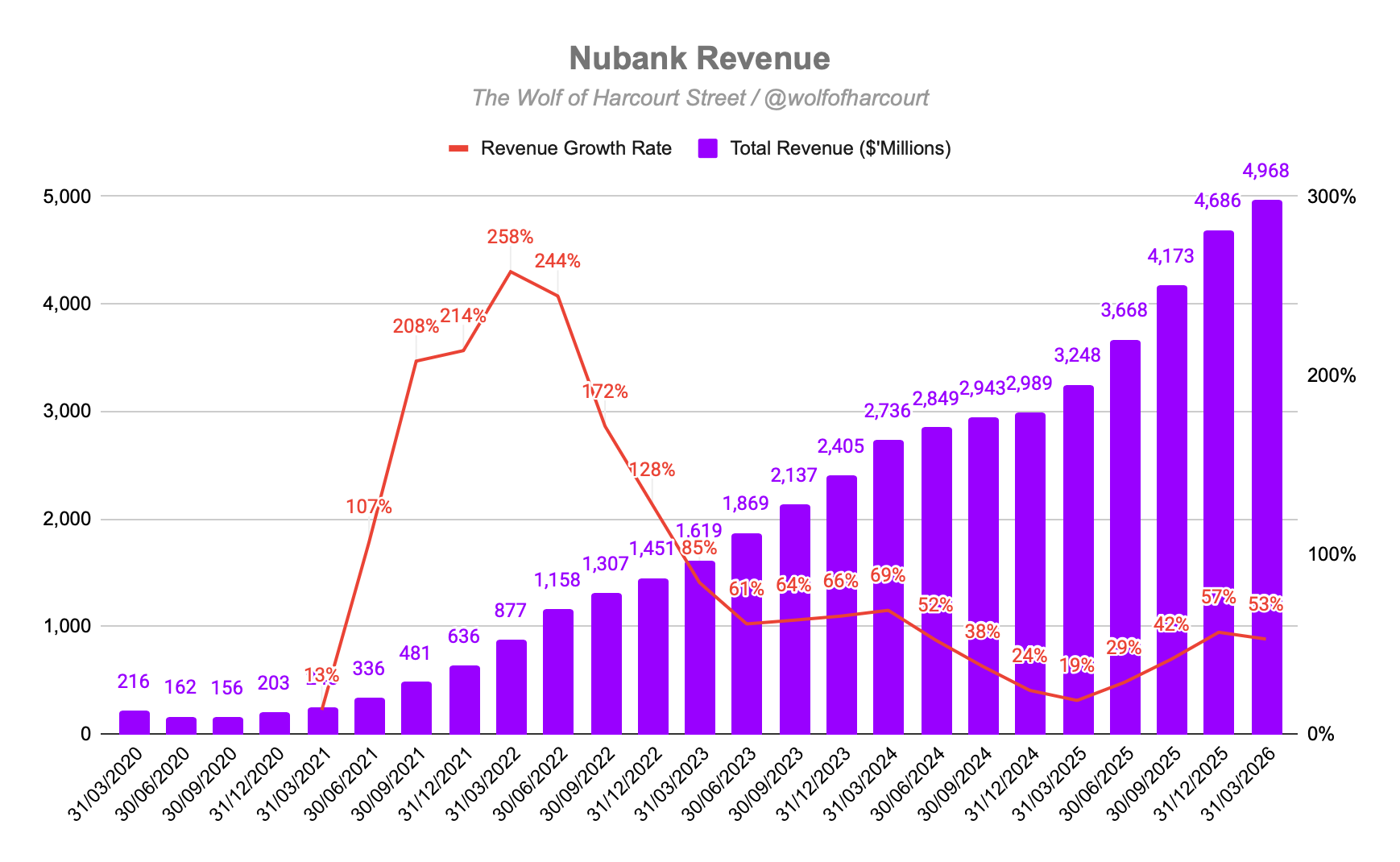

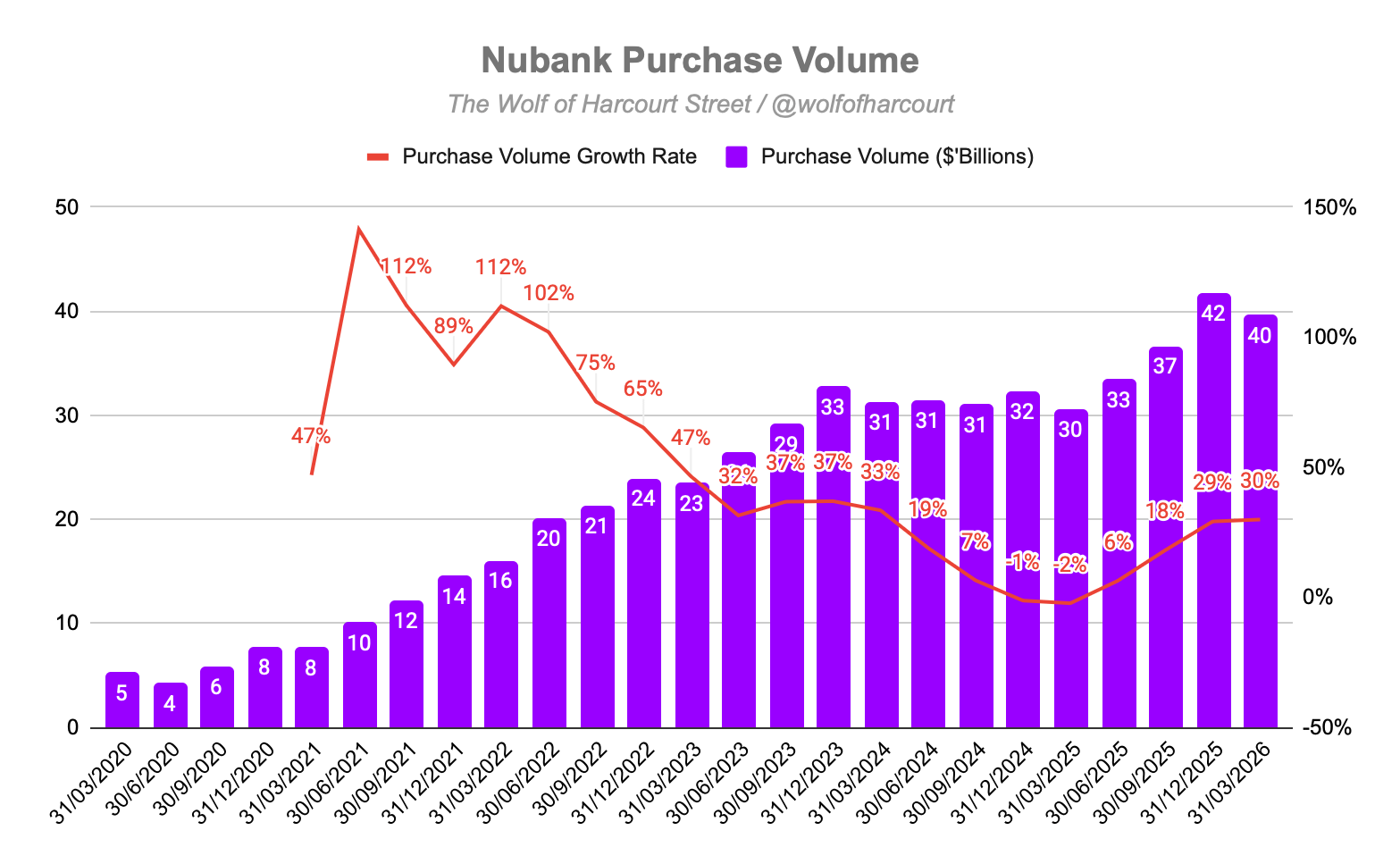

Nubank (NU)

I added to NU following the post-earnings selloff after Q1 2026 results. On the surface, this was not a perfectly clean quarter. Gross margin came in at 38%, down from the mid-40s earlier in 2025, while credit loss provisioning is clearly growing faster than revenue on that line. I am not dismissing those concerns, they represent the clearest bear case in the story and deserve close monitoring.

However, once I dug deeper into the numbers, the broader picture remained overwhelmingly positive. In my view, this business is compounding far faster than the market currently appreciates, and the earnings-day weakness created an opportunity.

The headline number tells the story. Revenue reached $5 billion, up 53% year-over-year. More importantly, growth has meaningfully re-accelerated. Earlier in 2025, revenue growth had slowed to 19%, leading many investors to declare the story broken. That narrative now looks increasingly premature. The rebound to 53% growth is a reminder that NU’s opportunity across Latin America remains enormous and largely untapped.

Purchase volume reinforced the same trend, reaching $40 billion in Q1, up 30% YoY, after recovering sharply from the -2% trough in late 2024 that had shaken investor confidence.

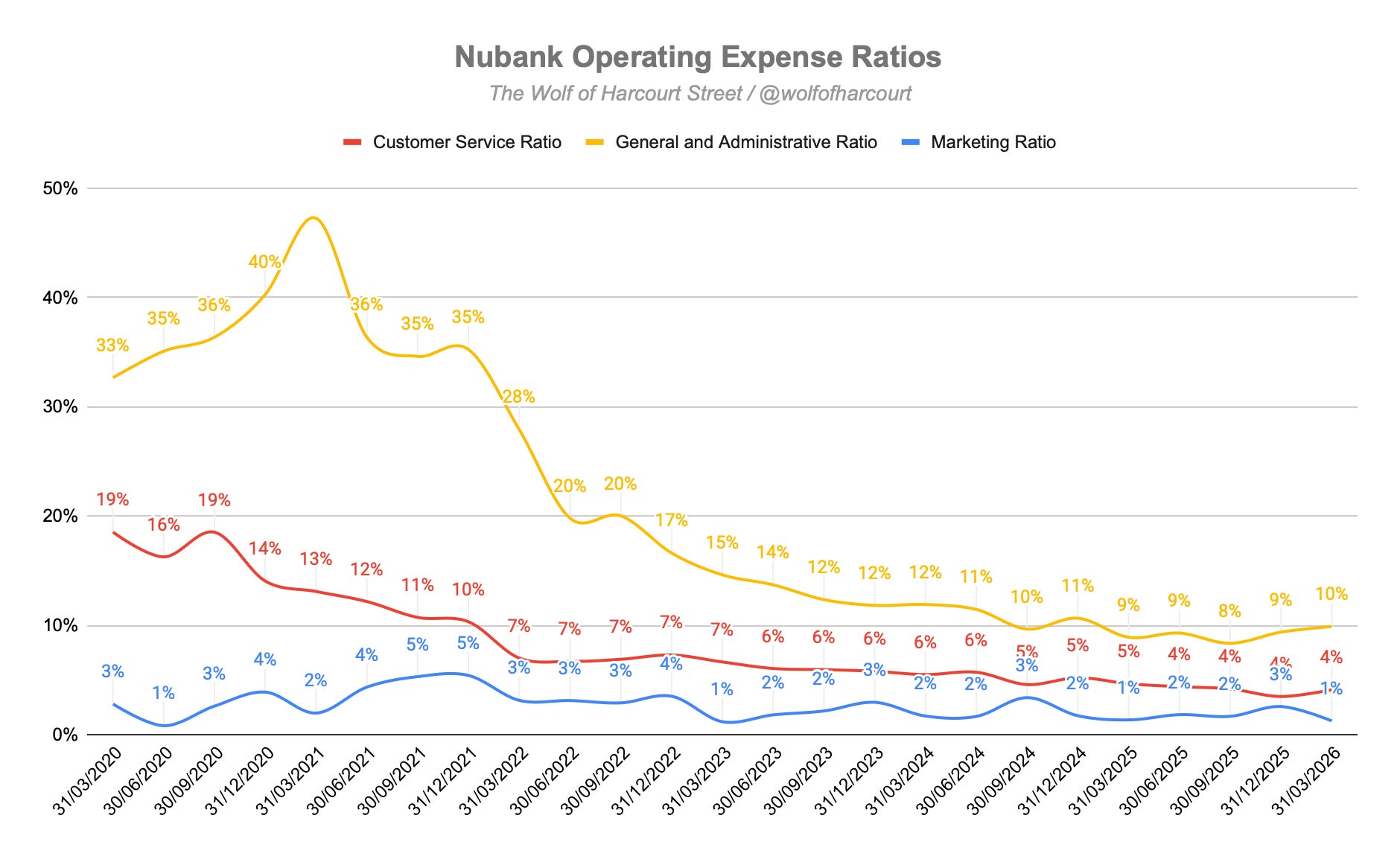

The metric that stood out most to me, however, was the operating expense ratio.

General and administrative expenses have now fallen to just 10% of revenue, down from 47% in 2021. Customer service costs sit at 4% of revenue versus 19% in 2020, while marketing expense is only 1% of revenue. These improvements are not cyclical, they reflect a technology-first business model that becomes structurally more efficient with scale.

When revenue is compounding at 53% while operating expenses remain relatively flat as a percentage of revenue, the operating leverage becomes extremely powerful.

I added after this quarter because I believe the market remains too focused on short-term gross margin pressure while underestimating the strength of the operating model underneath.

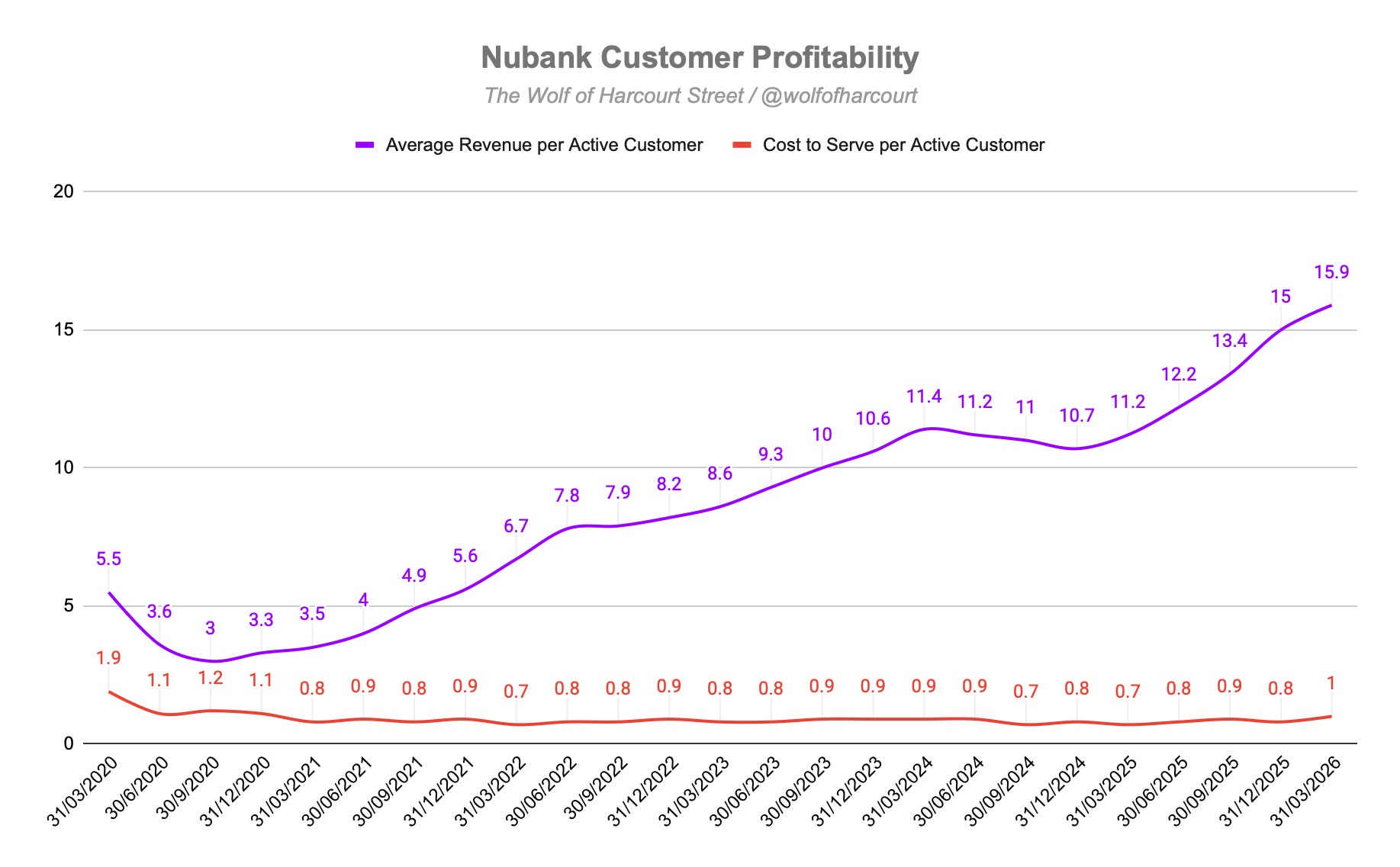

NU is now generating $15.9 in revenue per customer across a base of 135 million users that is still growing at double-digit rates across largely underbanked markets. This is not simply a digital bank. NU is building the financial operating system for Latin America, while operating with the cost structure of a software company.

That combination is exceptionally rare, and I am happy to remain a patient long-term holder.

InPost (INPST)

I sold my full position in INPST, which represented roughly 5.5% of the portfolio at the time of sale.

The stock was up 45% YTD following the €15.60 per share proposal to take the company private. Since news of the potential takeover emerged, I had largely been holding the position as a hedge given the stock continued trading close to the offer price, at roughly a 1.5% discount.

Now that I have deployed most of my available cash elsewhere, I wanted to raise some capital, and this was the easiest source of liquidity. At this stage, the remaining upside does not justify the opportunity cost of keeping capital tied up.

I also believe that if the takeover ultimately fails, the share price would likely retrace in the short term. The bid has unanimous board support and already has approximately 48% shareholder backing, although 80% tendering is required for completion.

If the bid fails, I would be more than happy to revisit the name in the future. If it does, I do not currently see a scenario where the stock meaningfully trades above the offer price in the near term.

Take-Two Interactive (TTWO)

I deployed a portion of the INPST proceeds into initiating a new position in TTWO.

I already shared a dedicated article covering the full thesis, but in short, this is a catalyst-driven investment. I believe the launch of GTA VI represents the single largest catalyst in the company’s history, driving a multi-year earnings inflection that transforms the business from a low-profit or loss-making base into a high-margin, record-scale cash flow machine.

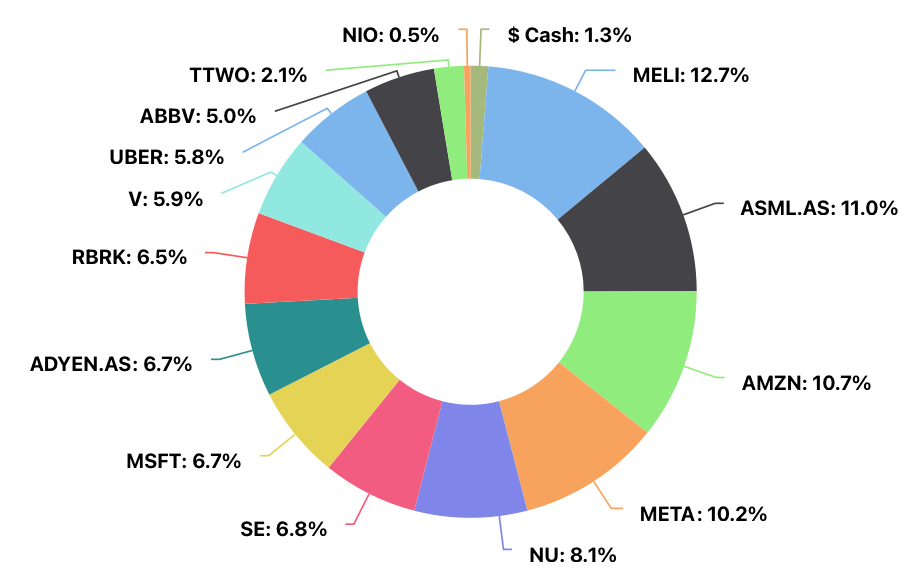

Allocation

I’ve been using Portseido to track my portfolio for years, and I highly recommend it. It consolidates all my transactions in one place, while its data visualisation and analytics capabilities guide my future decision-making and, ultimately, enhance my returns.

Sign up using my affiliate link here.

Buy List

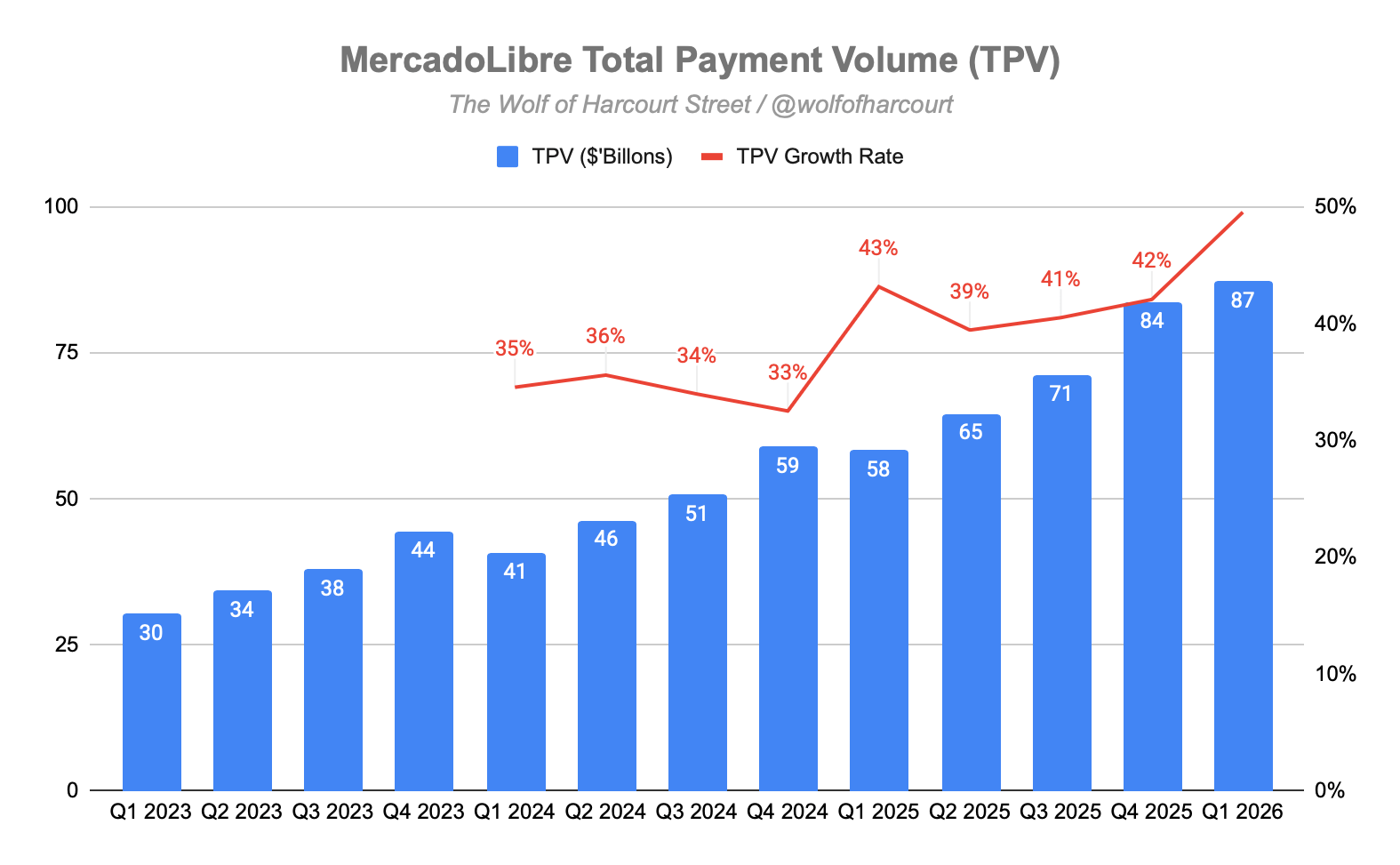

Mercado Libre (MELI)

MELI is already my largest position by a significant margin, but that has never stopped me from adding when I believe valuation and long-term opportunity remain attractive. In my view, the market has once again presented that opportunity.

The stock has struggled recently, down 15% YTD and 33% over the past year. Much of this weakness reflects temporary margin pressure caused by aggressive reinvestment into an enormous and still underpenetrated Latin American opportunity.

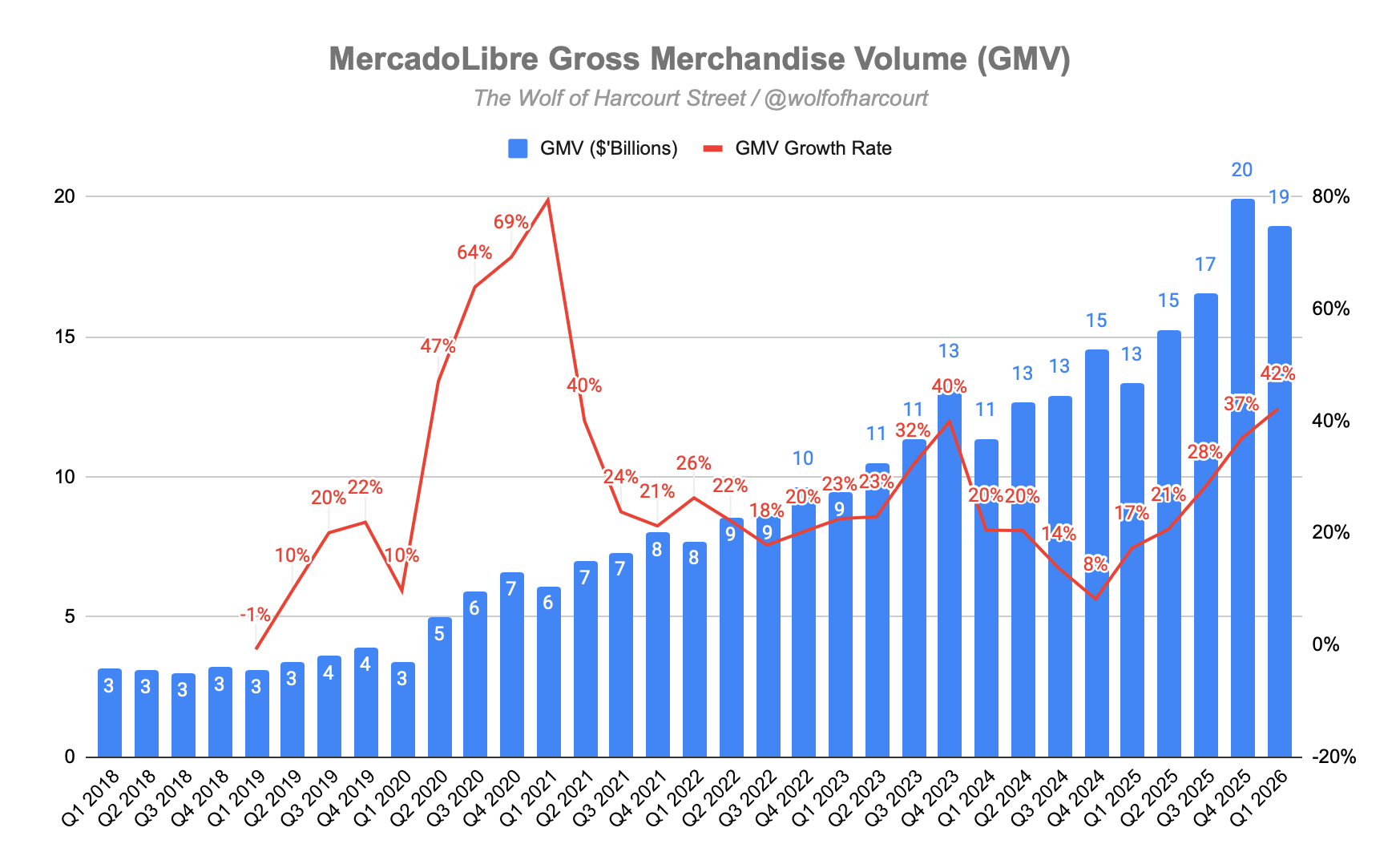

Q1 2026 results were exceptionally strong from a growth perspective. Net revenue increased 49% YoY to $8.85 billion, the fastest growth rate in nearly four years. E-commerce GMV grew 42%, marking the fifth consecutive quarter of acceleration and the fastest growth since Q1 2021.

Fintech revenue grew 51%, while TPV increased 50%, accelerating for the third consecutive quarter.

However, EPS came in at $8.23, below consensus expectations of roughly $8.8 to $9.7, as management deliberately prioritised growth over short-term profitability.

I put “miss” in quotation marks because MELI does not provide guidance. The company did not miss expectations, analysts simply underestimated the level of reinvestment management was willing to pursue.

This is a familiar playbook. We have seen similar periods throughout MELI’s history over the past two decades. Management consistently prioritises long-term market leadership and ecosystem expansion over near-term margins, and historically that strategy has compounded shareholder value exceptionally well.

Take-Two Interactive (TTWO)

I intend to build my TTWO position relatively quickly over the coming months as I believe the stock could begin moving materially once GTA VI marketing ramps up.

Last week, CEO Strauss Zelnick stated in an interview:

“The next few weeks don’t fall into summer yet, but when summer arrives, Rockstar anticipates beginning the promotion for GTA 6.”

To me, this strongly suggests the official marketing campaign will begin towards the end of June or early July.

In Case You Missed It

Some of the articles you might have missed during the past month:

Final Words

This was a very active month by my standards. I added to two existing positions, exited a full position, and initiated a new one. Cash now sits just above 1%, although I expect to deploy the remainder during June.

I continue to see significant opportunities across the market. Indices may be near all-time highs, but beneath the surface many sectors, particularly software, payments, and e-commerce, continue to lag materially. It remains an excellent environment for active stock picking.

Keep an eye on RBRK this month, with earnings scheduled for 5 June. At one point in April, the stock was down 42% YTD, although it has since staged an impressive recovery and now sits roughly flat for the year.

The stock had largely been punished through broader SaaS weakness, but I believe AI could become a significant long-term tailwind for the business. Perhaps the market is already beginning to anticipate that outcome. We will find out next week.

If you'd like to support the work of an independent analyst, you can buy me a coffee. The proceeds will contribute to covering the annual running costs of the newsletter.

Join the community of informed investors – subscribe now to receive the latest content straight to your inbox each week and never miss out on valuable investment insights.

The Chat is a space designed to facilitate, real-time discussions, share knowledge and debate ideas with fellow investors. Join the conversation.

If you found today's edition helpful, please consider sharing it with your friends and colleagues on social media or via email. Your support helps to continue to provide this newsletter for FREE!

Happy investing

Wolf of Harcourt Street

Contact me

Twitter: @wolfofharcourt

Email: wolfofharcourtstreet@gmail.com

entirely diffent approach...but maybe an interesting comparison...

https://reflectionsofreality.substack.com/p/beacon1-may-2026-what-ten-minutes