Welcome back to the Wolf of Harcourt Street Newsletter.

Every month, I'll provide you with an update on my portfolio, including all of the transactions, the current allocation, and my buy list. In addition, I'll share a recap of the articles you may have missed from the previous month.

Transactions

I added to my position in the following:

Airbnb (ABNB)

After reporting Q1 earnings, ABNB shares declined by 8% primarily due to perceived weak Q2 revenue guidance. Although Q1 revenue surpassed analysts' expectations by 4%, partially because some Q2 revenue was pulled forward into Q1 due to the timing of the Easter holiday, the guidance for Q2 appeared light. In reality, the projected H1 2024 revenue of $4.85 billion represents a 13% YoY increase and exceeds Wall Street's estimate of $4.80 billion. In the lead-up to Q1 earnings, my analysis suggested that ABNB was undervalued, and there was nothing in the Q1 report to contradict this. I took advantage of the market reaction to add to my position. The full earnings analysis is linked below for anyone who missed it

Nubank (NU)

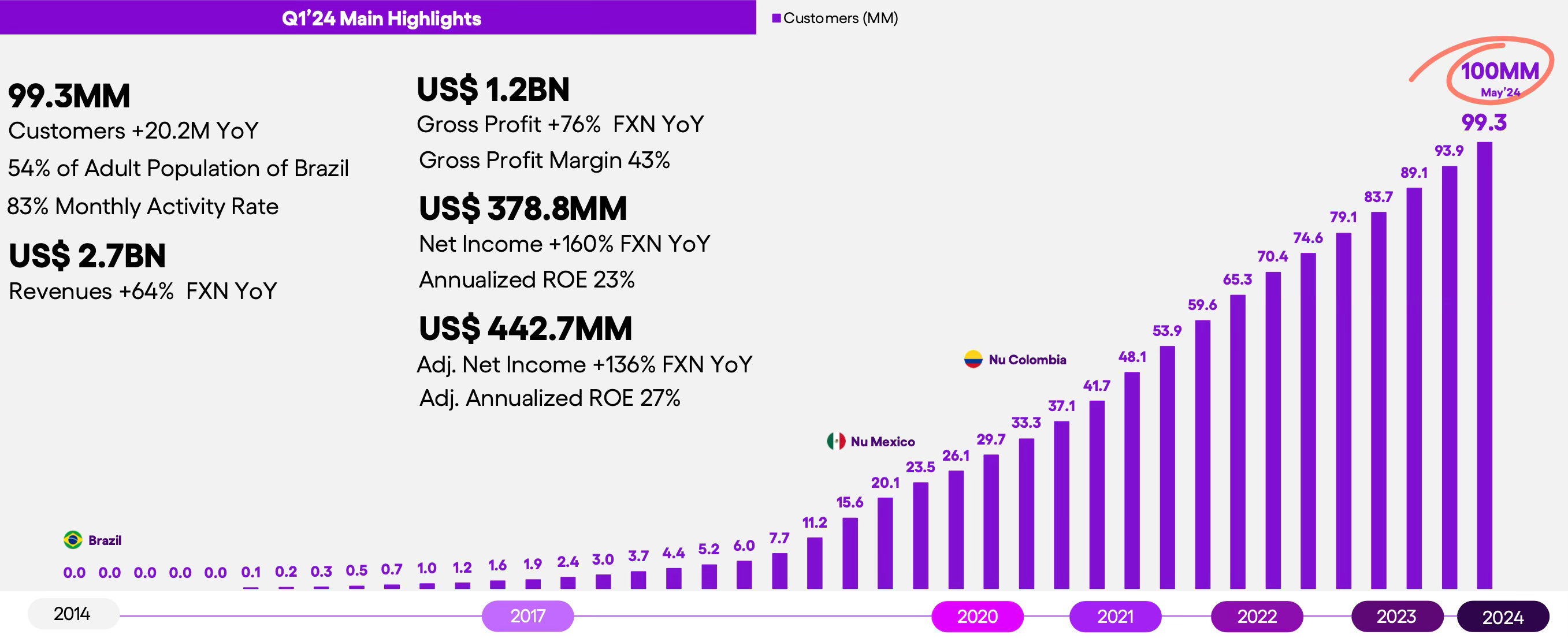

I added to my NU position in the lead up to Q1 earnings as it dropped below $11. The company once reported stellar earnings and the stock reacted accordingly. NU demonstrated the strength of its business model, anchored on three fundamental principles: fast customer expansion, increasing revenue per customer, and efficient operating costs. Key highlights from the report include:

Customer Growth: NU surpassed 99 million customers by the end of Q1 2024, a 67% increase from 59 million two years prior. In May, customers surpassed 100 million, becoming the first digital banking platform outside of Asia to reach this milestone, operating in just three Latin American countries. Brazil saw an impressive addition of 1.3 million customers per month, totaling 91.8 million customers. Mexico also experienced reaccelerated growth, adding nearly 1.5 million new customers to reach 6.6 million.

Financial Performance: Revenues surged to $2.7 billion, a 64% YoY increase, with gross profit growing 76% to $1.2 billion and a gross margin of 43.2%. Net income rose to $379 million, and adjusted net income was $443 million, reflecting YoY expansions of 160% and 136%, respectively.

Operational Efficiency: The robust growth was driven by cross-selling and upselling opportunities, leading to a threefold increase in quarterly revenues within two years, with a 75% annual compounded growth rate. The company’s strong pricing and underwriting capabilities resulted in a fourfold increase in quarterly gross profit during the same period.

Strategic Focus in Mexico: Mexico outpaced Brazil in key performance indicators since the launch of Cuenta Nu. Within a year, Mexico surpassed Brazil in customer numbers, checking account holders, and market share. Nu Mexico also achieved significant milestones in credit card customer numbers and market share, with $1.6 billion in credit card purchase volume and $2.3 billion in retail deposits.

I didn’t open any new positions during the month.

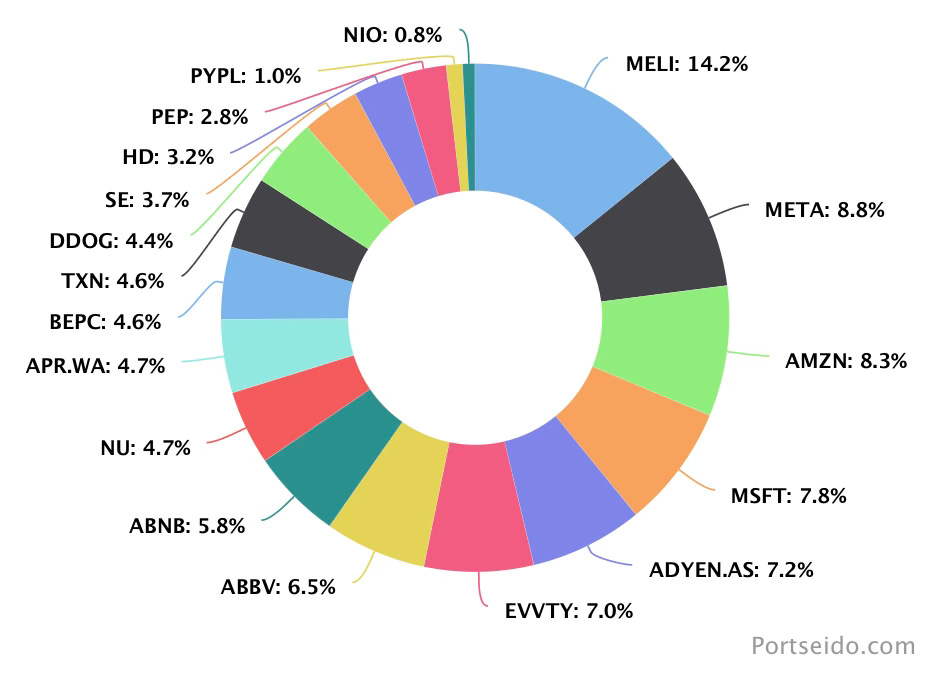

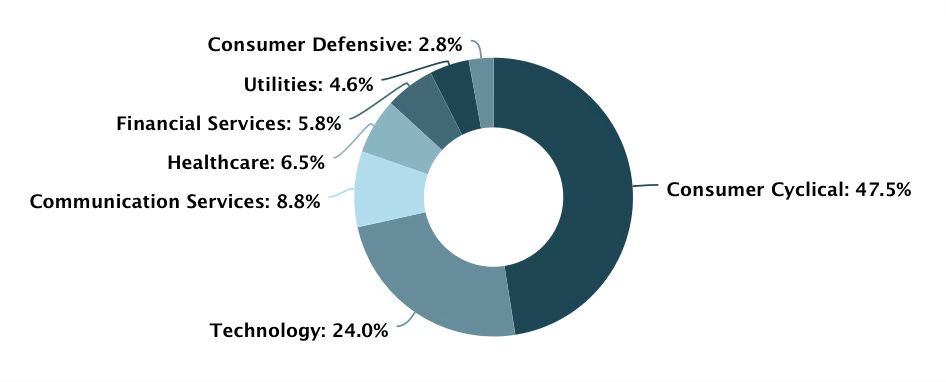

Allocation

Portseido is the tool that I have been using to track my portfolio for a number of years. I really like the charts that it produces and how it tracks performance. They also added a feature to automatically track dividends too. To top it off, it is effortless to update for new transactions. The team have kindly given me an affiliate link so if you would like to sign up you can click here.

Buy List

Stocks that are on my radar to add this month:

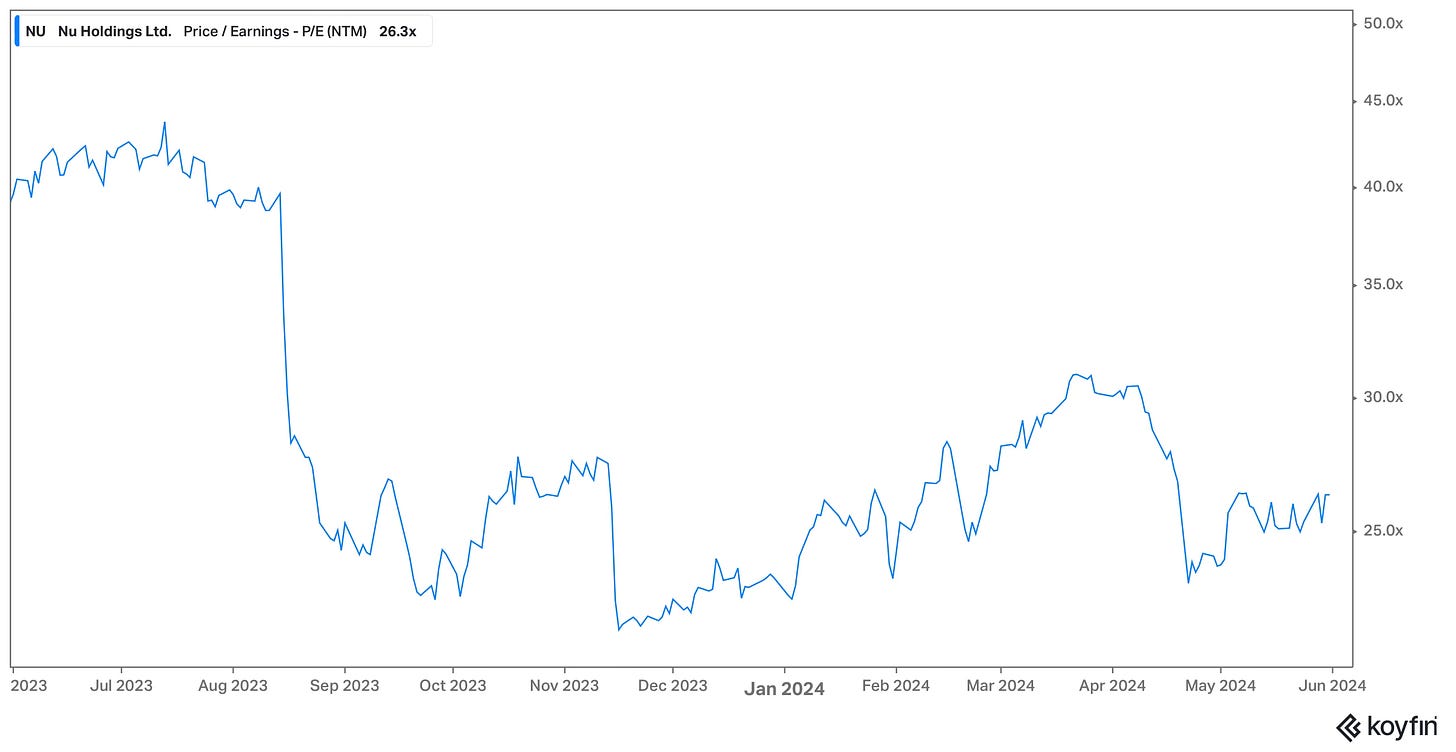

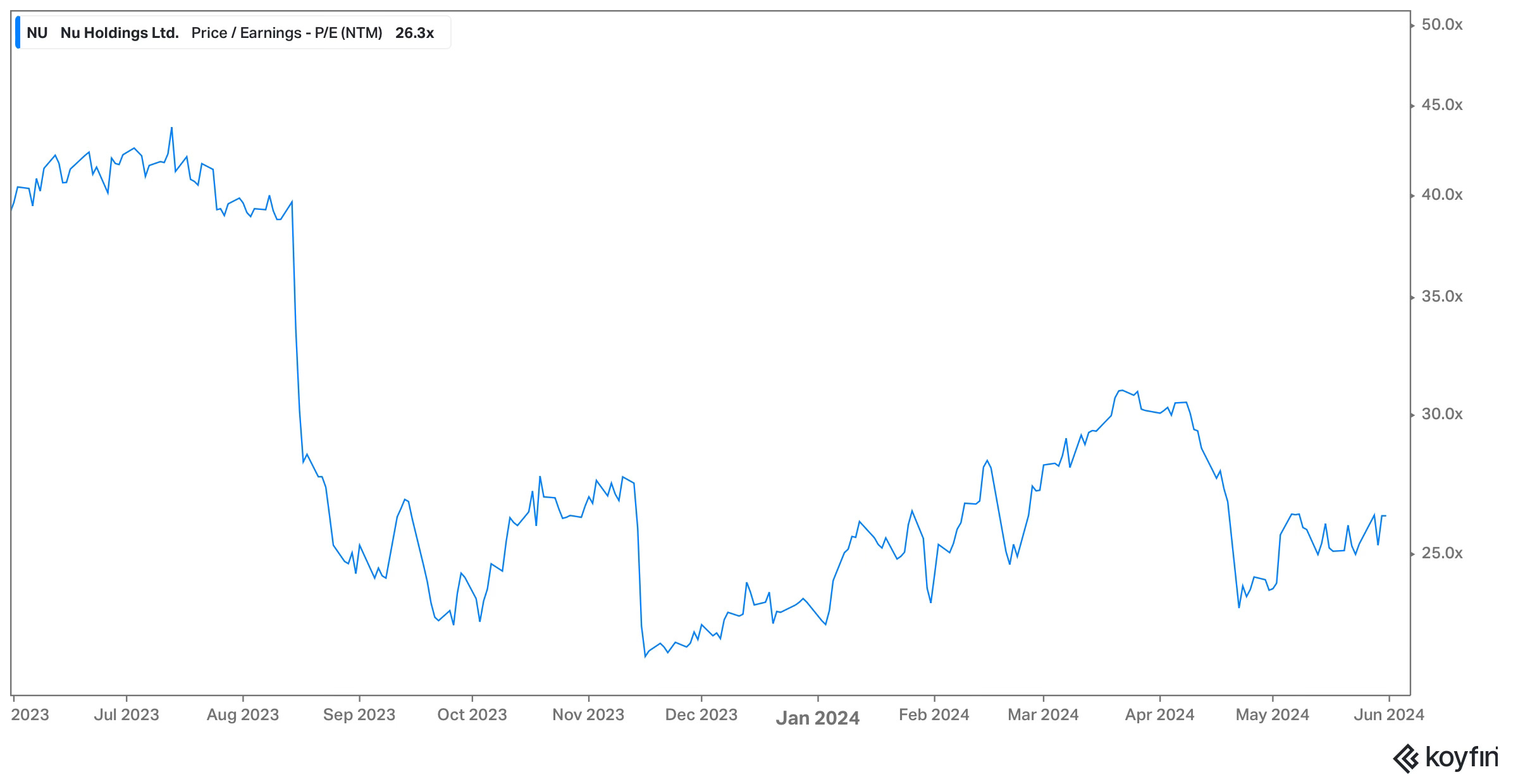

Nubank (NU) - Despite NU stock rising 9% over the past month, it now trades at a cheaper valuation. How is this possible, you might ask? As mentioned earlier, NU grew its net income by 160% in Q1, meaning that it trades at 26 times forward earnings compared to 30 times forward earnings at the beginning of April. NU holds a 4.7% weight in my portfolio, meaning that there is plenty of scope to increase the position.

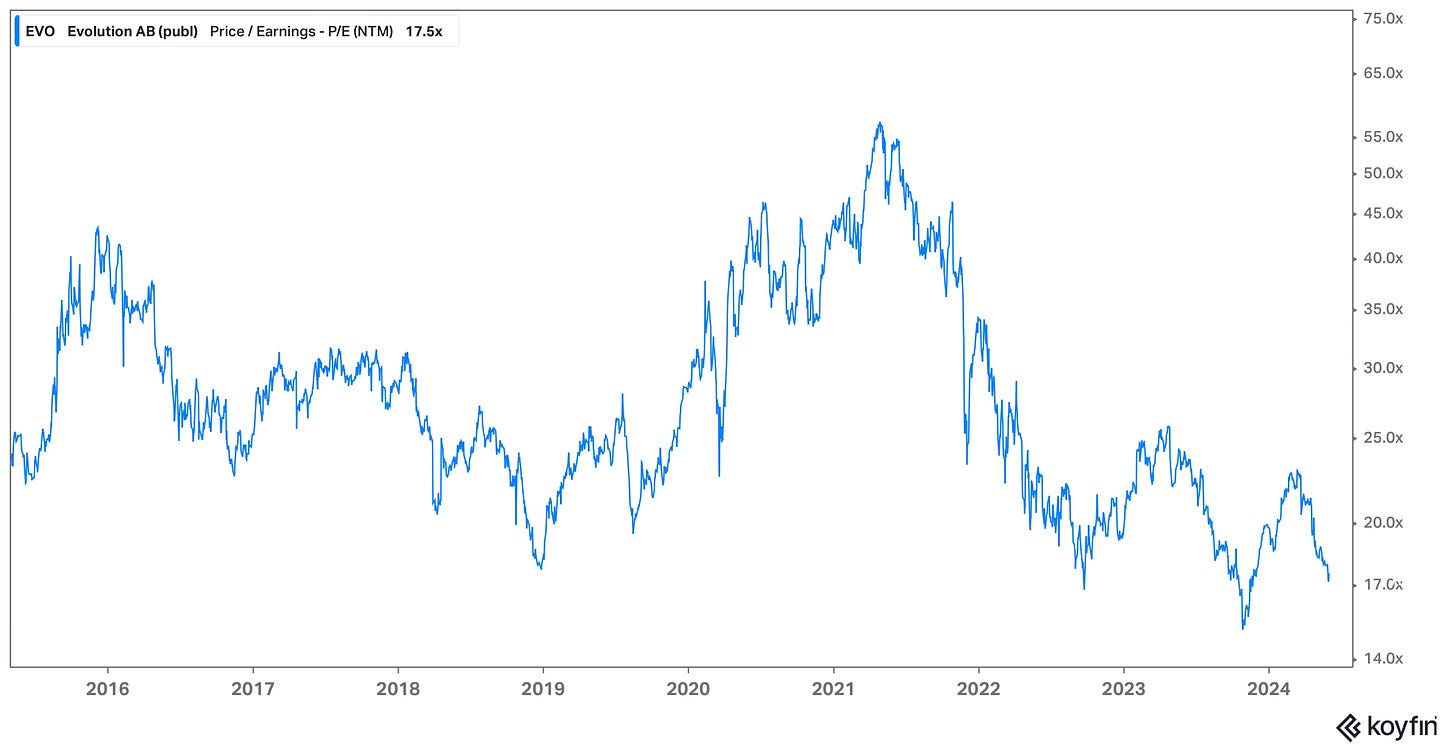

Evolution (EVO) - The share price has been under pressure for the past two months, so much so that the forward earnings multiple has dropped from 22 in March to just 17. Only twice in the company's history has it traded at a lower multiple: September 2022 and October 2023. Despite this being a large holding in the portfolio, the opportunity to grab more shares in a wide-moat company growing revenue by 20% on a constant currency basis at a historically low valuation is hard to ignore.

In Case You Missed It

Some of the articles you might have missed during the past month:

Final Words

There are a lot of opportunities in the market at the moment, particularly in the Consumer Cyclical area, but I have been focusing on high-conviction names already within the portfolio. It can be easy to get distracted by shiny new stocks that have experienced share price declines, such as Tesla and Lululemon, to name a few. I’ve already done the work on existing names in the portfolio, so I can add capital to these names with a higher degree of confidence.

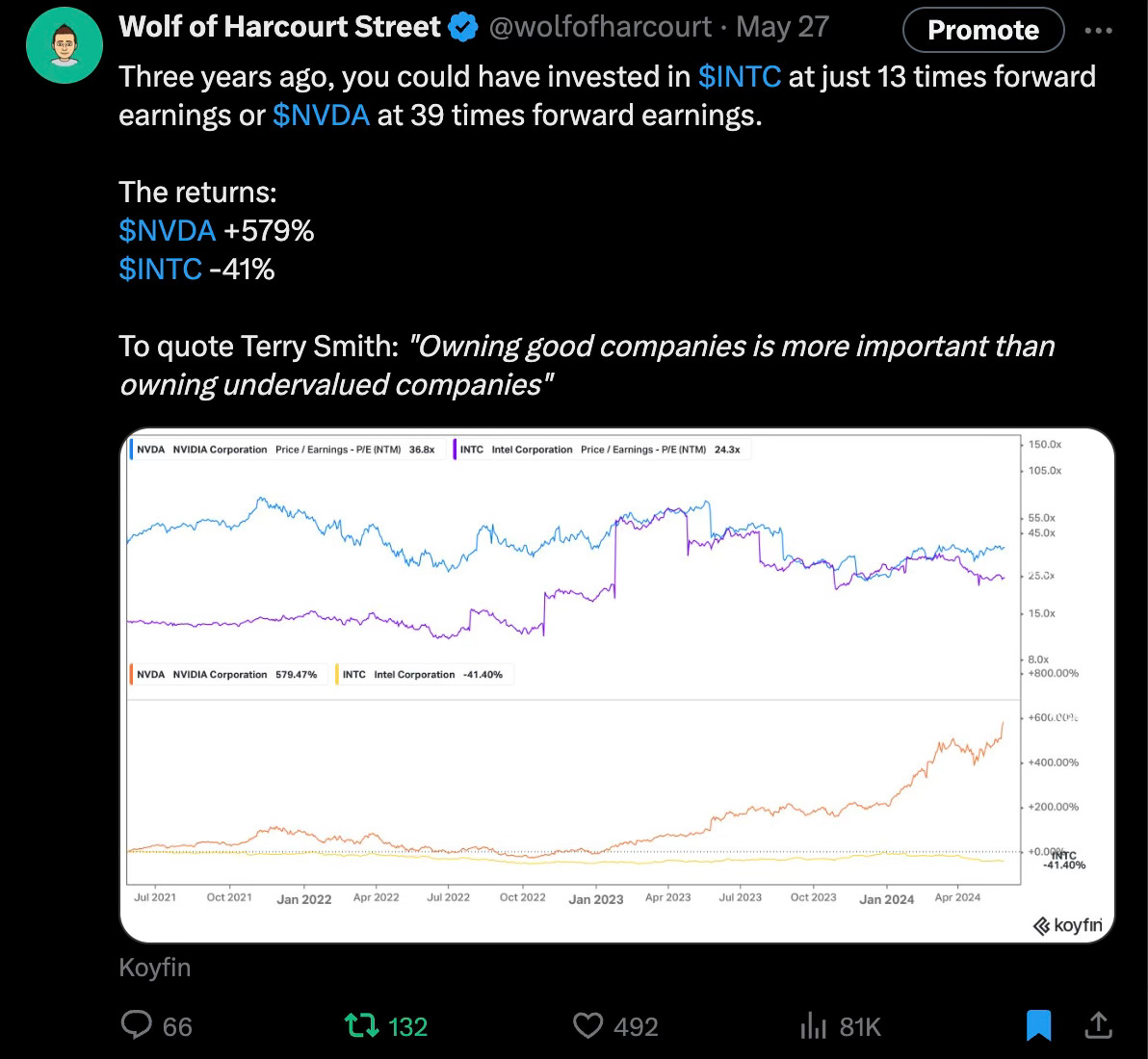

That being said, I am beginning to look at adding new positions to the portfolio, but it takes me time to build up conviction in new names. Impulsive decisions purely based on share price rarely lead to good outcomes. Owning good companies is more important than owning undervalued companies alone, as a recent tweet I shared demonstrated. It’s easy to look at a number on a screen and compare a relative valuation. A lot more than numbers is required to determine business quality and durability. There are no shortcuts to this process.

If you'd like to support the work of an independent analyst, you can buy me a coffee. The proceeds will contribute to covering the annual running costs of the newsletter.

Join the community of informed investors – subscribe now to receive the latest content straight to your inbox each week and never miss out on valuable investment insights.

If you found today's edition helpful, please consider sharing it with your friends and colleagues on social media or via email. Your support helps to continue to provide this newsletter for FREE!

Happy investing

Wolf of Harcourt Street

Contact me

Twitter: @wolfofharcourt

Email: wolfofharcourtstreet@gmail.com

Why ABNB and not BKNG?