Welcome back to the Wolf of Harcourt Street Newsletter.

Every month, I'll provide you with an update on my portfolio, including all of the transactions, the current allocation, and my buy list. In addition, I'll share a recap of the articles you may have missed from the previous month.

Transactions

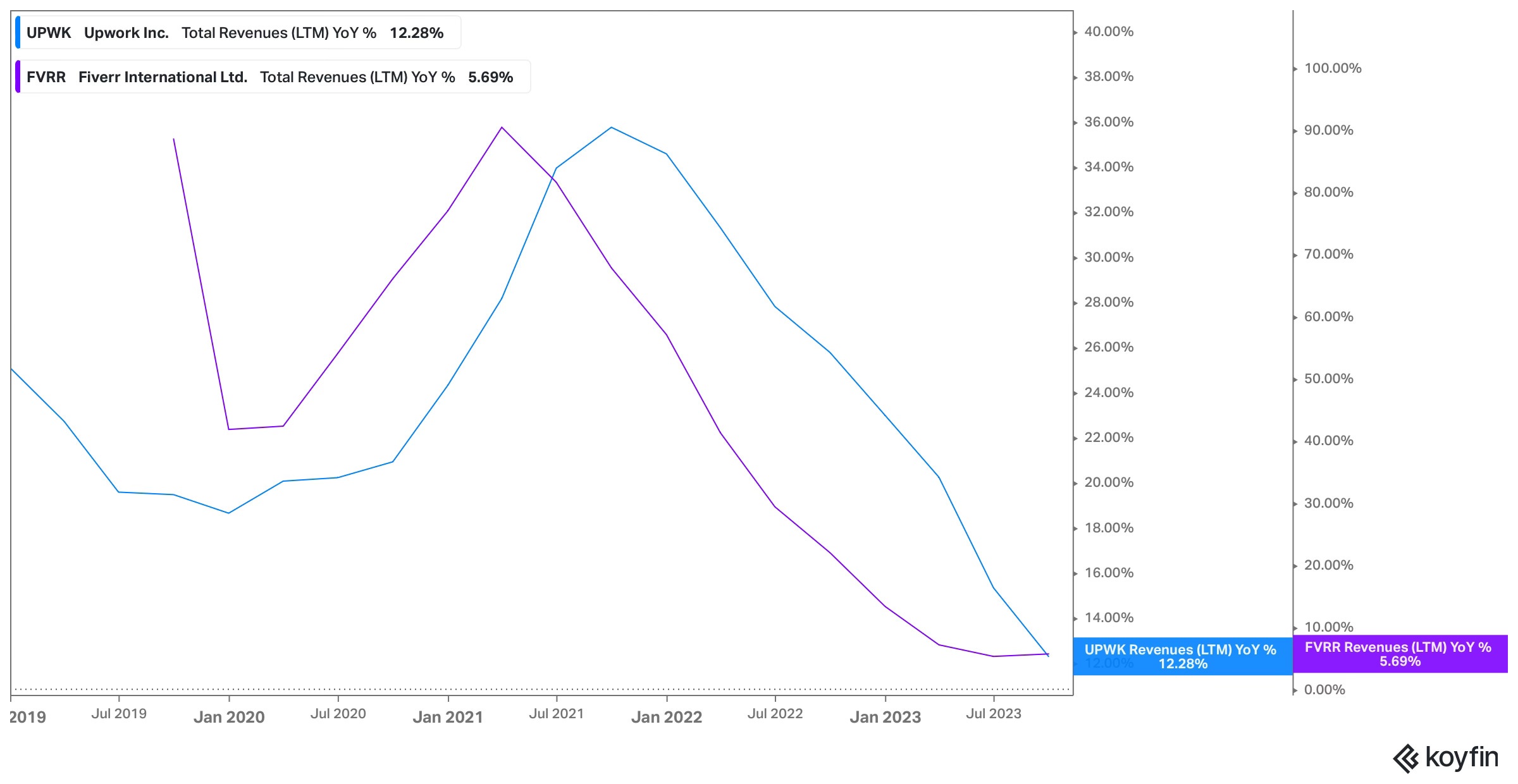

Last month, I made significant progress in consolidating my portfolio as planned. I entered this month with 6% in cash having not yet deployed the proceeds from Johnson & Johnson (JNJ). I continued the process this month and reduced my full exposure in Fiverr (FVRR), a 0.75% position in my portfolio.

The core of my initial Fiverr investment thesis was the emergence of the gig economy. The impact of Covid created favorable conditions for freelance workers and the remote work economy, and I believed this was a long-term trend. While remote work remains widespread, I did not anticipate the complete disruption that Artificial Intelligence (AI) would bring to the freelance industry. This observation is backed by data from the Online Labor Market (Hui et al, 2023), as cited in a recent Financial Times article.

In 2020, Fiverr caught my attention through personal experience—I used the service multiple times and found it to be excellent. However, since the introduction of ChatGPT in 2022, I haven't used Fiverr once.

During the same period, both Fiverr and its competitor Upwork (UPWK) have seen a significant decline in revenue since growth peaked in 2021.

The future of freelancing is currently very uncertain. It's possible that AI could turn out to be a passing trend and that both stocks will recover. Personally, I find the level of uncertainty too high, and since the position is so insignificant in my portfolio, it's easiest for me to cut my losses and consolidate elsewhere.

New Position

Auto Partner (APR.WA)

I invested more than a third of the JNJ proceeds into APR, which I have been tracking for a while. The company released Q3 earnings in November, and while the earnings call is not recorded, I was invited to participate.

In summary, Auto Partner recorded revenue growth of 30% for YTD 2023, driven by strong performance in both domestic and international markets, now accounting for 50% of total sales. I was really impressed by the management team, and their actions, including a new hub in Zgorzelec near Poland's western border, reflect a well-planned strategy to strengthen distribution capabilities, optimize logistics, and strategically position itself for increased competitiveness in both domestic and international markets.

The full Auto Partner Q3 2023 earnings analysis is linked below for anyone who missed it.

I added to my positions in the following:

Facebook (META)

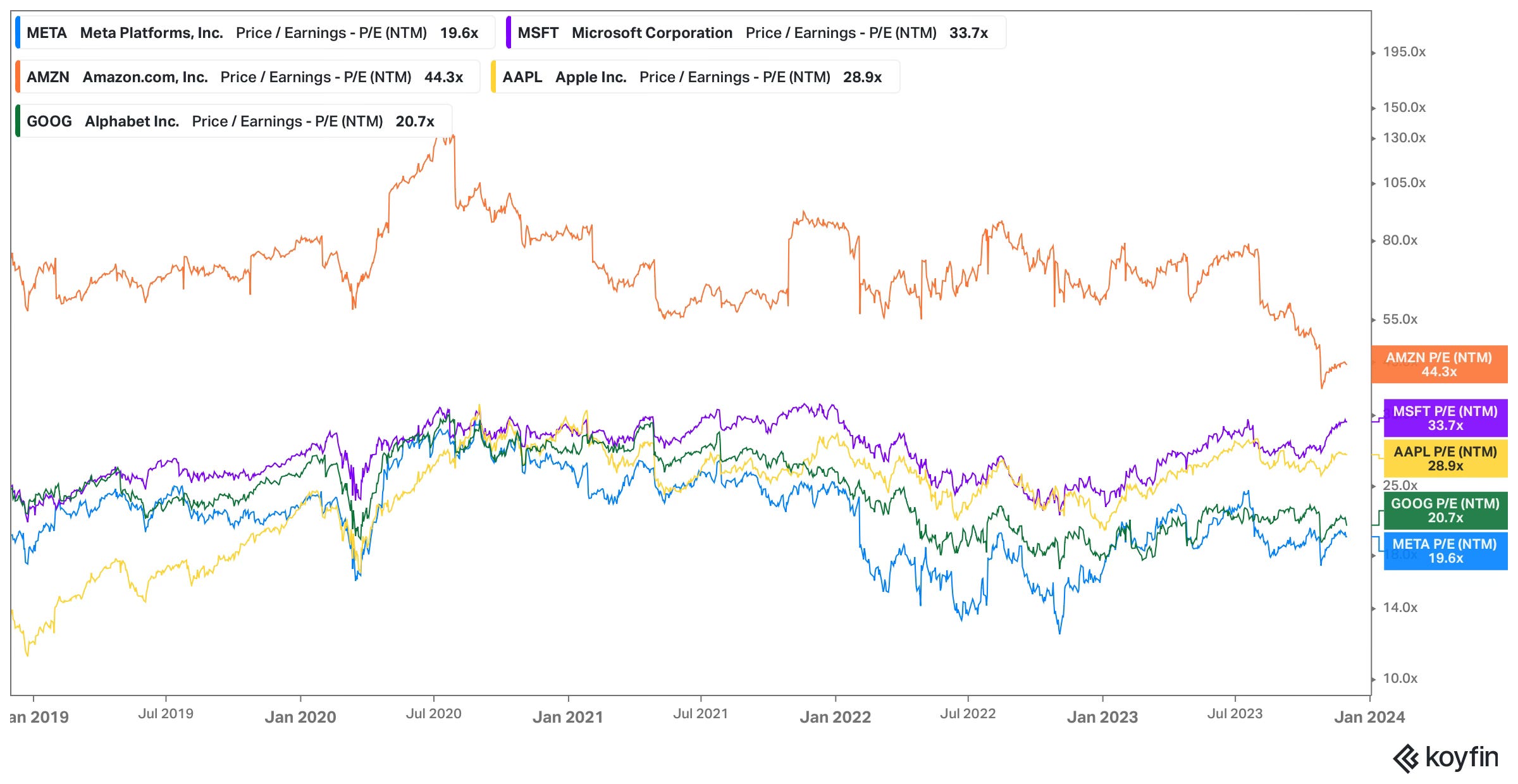

I put a third of the JNJ proceeds into META. META did exceptionally well in Q3, with reported revenue and EPS of $34.1 billion and $4.39, respectively. This surpassed Wall Street estimates of $33.5 billion and $1.64. Despite a year-to-date return of over +170%, META had a reasonable 18x forward earnings valuation at the beginning of November. Although the P/E ratio has its shortcomings, it's noteworthy that META trades at the lowest valuation among the Big Tech stocks.

PepsiCo (PEP)

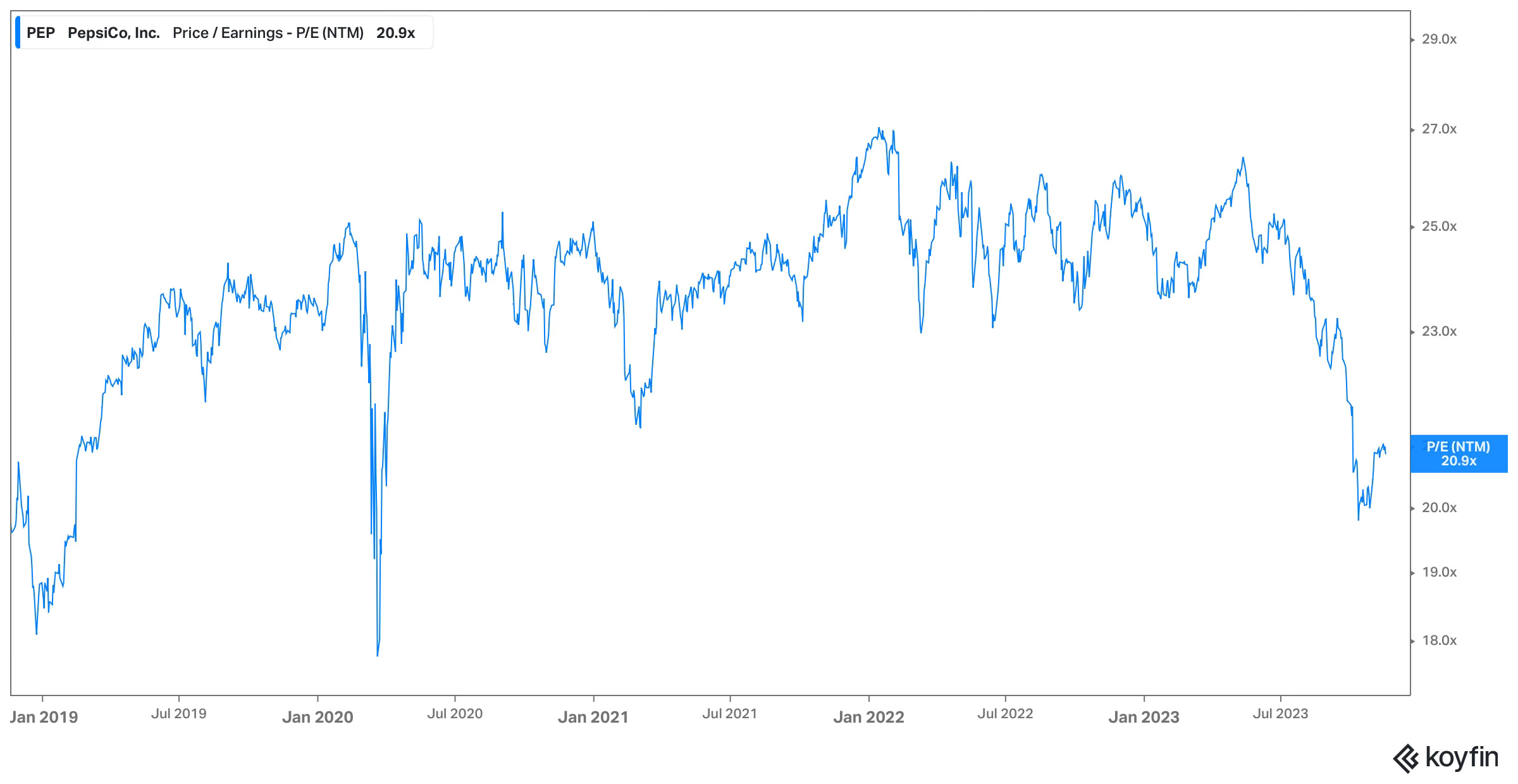

I allocated the remainder of the proceeds from JNJ into PEP. By the end of October, PEP stock had declined by 10% year-to-date and was trading at less than 20 times forward earnings, primarily due to concerns about the perceived impact of GLP-1 weight-loss drugs. However, I think this concern is being exaggerated.

On the Q3 earnings call, management noted minimal impact on their business from GLP-1 thus far:

So far, the impact is negligible in our business. Overall, if you take global consumption, there's obviously a lot of question marks with regards to this – obviously, the drugs when it comes to medical testing or scalability of the usage of this or what is the impact really on consumer choices. So a lot of question marks.

Although it's still too early to determine the true long-term effects of GLP-1, if weight-loss drugs involving GLP-1 indeed lead to volume reduction, PEP is in a good position to adapt to changing consumer preferences. This adaptation could include strategies like adjusting pricing and product mix to accommodate a shift toward smaller packs. Through pricing adjustments for these smaller packs, PEP has the potential to improve both overall revenue and profit margins by leveraging its pricing power.

Sea Limited (SE)

I invested all the proceeds from FVRR into SE after it fell by 20% following its Q3 earnings report. SE surpassed Wall Street revenue estimates but fell short on EPS, marking its first negative earnings since Q3 2022. Throughout the quarter, SE increased spending on Sales & Marketing (S&M) expenses, leading to the reported losses.

During the triple-digit revenue growth years of 2020 and 2021, SE allocated over 40% of its revenue to S&M expenses. The contrast between SE in 2023 and the Covid era SE lies in the fact that most S&M expenses were dedicated to vouchers and discounts, effectively subsidizing sales. However, in 2023, the majority of S&M expenses are directed towards Capital Expenditure (CapEx) to develop its live streaming ecosystem. This is evident as, despite reporting a net operating loss, SE showed positive cash flow from operations, considering CapEx is not factored into cash flow from operations. This implies that while the impact of S&M expenses on growth may not be immediately felt and could take several quarters or even years to materialise, it represents a more sustainable approach to growth and the establishment of a durable competitive advantage.

The full Sea Q3 2023 earnings analysis is linked below for anyone that missed it.

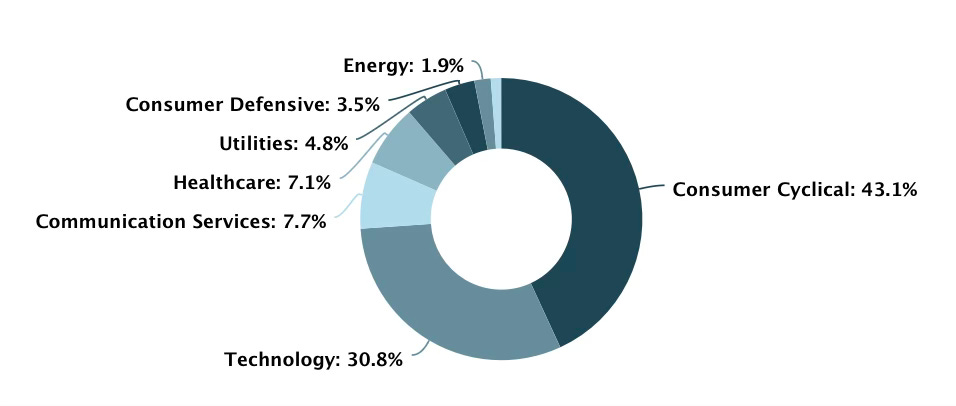

Allocation

Portseido is the tool that I have been using to track my portfolio for a number of years. I really like the charts that it produces and how it tracks performance. They also added a feature to automatically track dividends too. To top it off, it is effortless to update for new transactions. The team have kindly given me an affiliate link so if you would like to sign up you can click here.

Broker

Trade Republic is the investment broker that I use. The platforms combination of low fees, accessibility, fractional share options, and regulatory backing make it a reliable choice.

From 1 October, Trade Republic has doubled its interest on uninvested cash from 2% to 4% per annum, paid monthly. This is one of the most competitive rates on the market for European investors.

Click here to sign up for a free Trade Republic account

Buy List

Stocks that are on my radar to add this month:

Evolution (EVO.ST) - On 10 November, the CEO Martin Carlesund purchased €8.6 million (SEK 100 million) worth of shares. It was the first time the CEO has purchased stock since September 2022 and it came just days after the Board approved the 2023/2026 warrant incentive plan. As we know, insiders might sell their shares for any number of reasons, but they buy them for only one: they think the price will rise. Then on 23 November, the company announced a new €400 million buyback program which I had predicted at the start of November. My thesis is already starting to play out.

The full Evolution investment thesis is linked below for anyone that missed it.

Auto Partner (APR.WA) - APR is a new position in my portfolio and as such I am still building it out in terms of portfolio weight. I took the initial starter position when the stock pulled back to the 50-day moving average before it reported Q3 earnings. I am comfortable with the current valuation but from a technical perspective, I would like to see the stock consolidate or pull back to the 50 day moving average again to continue accumulating shares.

Trading View

In Case You Missed It

Some of the articles you might have missed during the past month:

Final Words

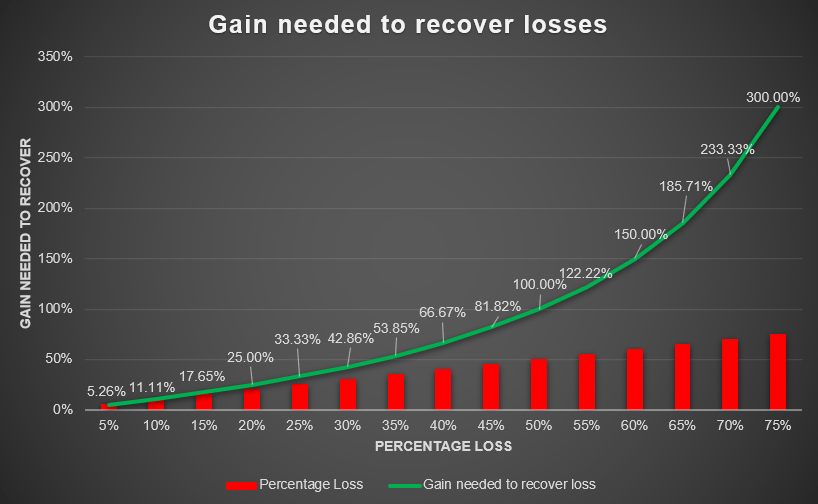

November was a great month for the portfolio as it hit a new all-time high value. The last ATH occurred in October 2021 and while the drawdown over the past 2 years felt painful at the time, it ultimately presented a fantastic buying opportunity. It's important to note that shortly after reaching the last ATH, the portfolio did undergo the drawdown. This might indeed mark another peak, time will tell. With one month of the year to go, the 2023 portfolio performance should make for interesting reading.

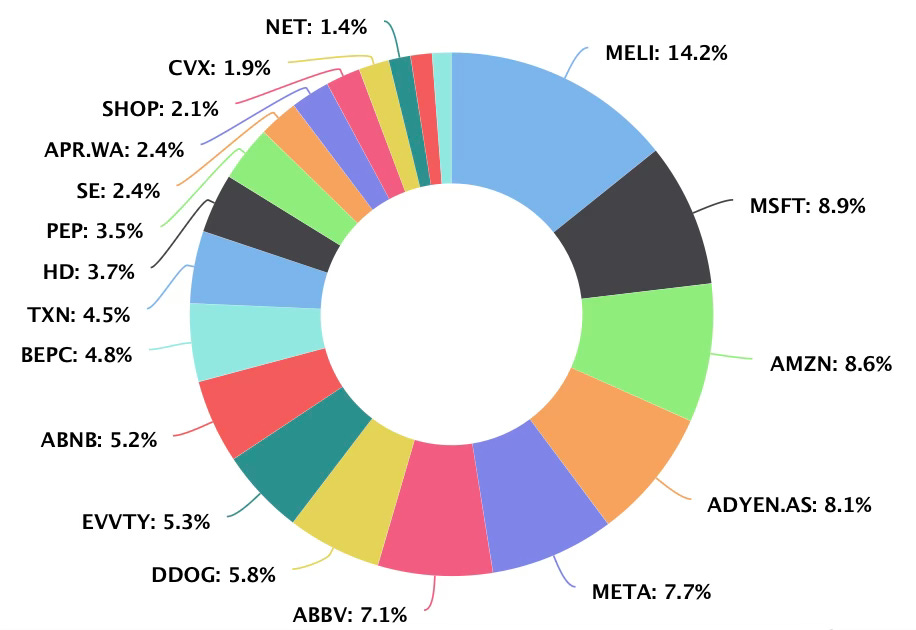

This recent move higher in November has been powered by moves from MercadoLibre (+32%), Adyen (+75%) and Datadog (+45%) in particular. MercadoLibre remains my largest position, with Adyen shooting from seventh to fourth, and Datadog jumping from tenth to seventh. What is personally satisfying about this is that these winners are the product of investment thesis’s that I have shared publicly with readers in 2023.

I am a long-term investor and don’t believe you can judge the ultimate success of a thesis in a couple of months as it takes many years to play out. However, I’d much rather have a stock I buy appreciate 50% in a couple of months rather than depreciate by the same amount!

If you'd like to support the work of an independent analyst, you can buy me a coffee. The proceeds will contribute to covering the annual running costs of the newsletter.

Join the community of informed investors – subscribe now to receive the latest content straight to your inbox each week and never miss out on valuable investment insights.

If you found today's edition helpful, please consider sharing it with your friends and colleagues on social media or via email. Your support helps to continue to provide this newsletter for FREE!

Happy investing

Wolf of Harcourt Street

Contact me

Twitter: @wolfofharcourt

Email: wolfofharcourtstreet@gmail.com

Great portfolio of quality businesses!